Contact us

Contact Nuveen

Thank you for your message. We will contact you shortly.

Key takeaways:

- Effective participant communication and education during market volatility can help prevent impulsive decisions and reinforce long-term investing discipline.

- Plan sponsors should view periods of volatility as opportunities to reassess plan design, enhance investment menus and consider features like auto-enrollment and guaranteed income solutions.1

- Incorporating guaranteed income strategies can offer participants confidence and greater financial security in retirement.

Participant engagement strategies

During periods of market volatility, participants often feel overwhelmed and worried about their financial futures. It is not uncommon for participants to change contributions or consider more active trading in their accounts.8 In these situations, it is important to encourage participants to stay the course, as remaining invested in the markets is typically the most effective way to achieve long-term goals.

Participant education must be a top priority during volatile market conditions, especially for those in the earlier stages of their careers who may have had limited exposure to significant market volatility or economic downturns. Also vulnerable are participants in the latter stages of their careers who may not have as much time to see asset values rebound from a potential downturn before they intend to retire. For these investors, communication from a plan sponsor may make the difference between panicked selling and a longer-term perspective that could see values recover before withdrawals are due to start.

Fundamentally, target date funds are designed to mitigate such suboptimal decision-making. Their inherent asset allocation model helps smooth out market volatility and systematically reduces risk as participants approach retirement age. While there’s no one-size-fits-all approach to “staying invested” due to varying individual preferences, long-term financial goals and risk appetites, investors seeking potential market upside while cushioning downside risk may consider a range of specific portfolio allocations.

Why stay invested?

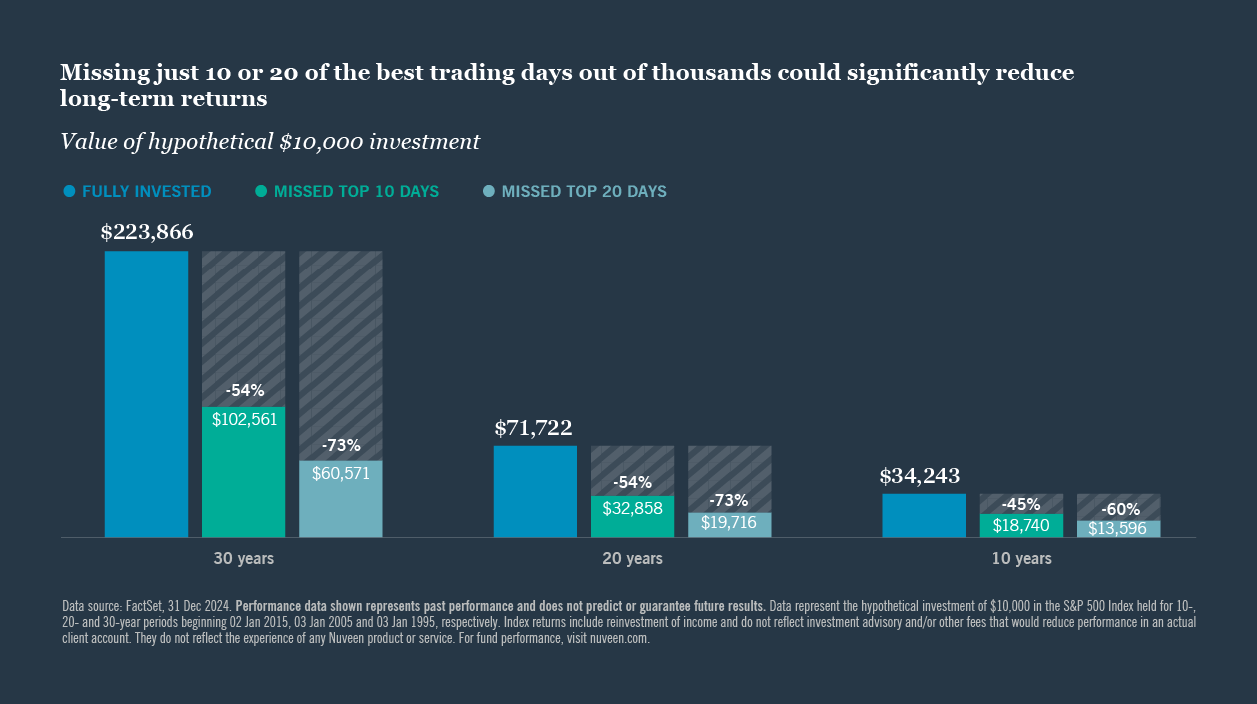

The timeless mantra “stay invested” can be especially challenging during periods of volatility, but historical data overwhelmingly favors remaining in the market, particularly for investors with long-term objectives. Between 1937 and 2024, for example, U.S. stocks delivered positive calendar-year returns 76% of the time, averaging nearly 20% per annum in those years. In the 24% of years with negative returns, losses averaged -12.5%.9 The pattern of market performance is difficult to predict and missing even the first few days of a market rebound can lead to long-term underperformance.

Participants who stick to a systematic investing plan may take advantage of stock market downturns to enhance investment returns. Such approaches can reduce the emotion created by market volatility, avoid the traps of market timing and help achieve financial goals. During periods of market instability, it’s best to encourage participants to remain calm, take a breath and consider their options before taking any action.

Consideration should be given to implementing automatic messaging triggers during moments of significant market volatility. These systems are often at the recordkeeper level, so it is worth having a conversation with your relevant provider to see what is possible. When set up correctly and judiciously activated, these mechanisms can send reassuring messaging to participants during times of elevated market stress.

Plan design

Examine the investment fundamentals of the plan

Although periods of heightened market volatility may not seem like the optimal time to dive into the weeds of plan design, they can, in fact, present an opportune moment to focus on fundamental design principles and reassess underlying assumptions. This can help ensure the plan’s optimal performance during market stress. Volatile times also present a valuable opportunity to work with an advisor or consultant to examine ways to enhance the plan’s investment menu and consider the inclusion of guaranteed elements. Market stress can reveal weaknesses in existing options, prompt deeper conversations about participants’ evolving needs, and potentially create momentum for adopting solutions.

Additionally, it is also prudent to reevaluate current plan features, such as auto-enrollment and auto-escalation benefits. Ensuring automatic participant enrollment and appropriate auto-escalation levels to achieve adequate retirement savings rates is crucial. During volatile periods, increasing plan participation and contribution rates can enhance the participants’ asset base, allowing them to potentially benefit from a market recovery to historical return profiles.

It is also worth noting that volatile times could present a favorable environment to initiate a plan if one is not currently in place. When participants observe volatility in the market, the benefits of tax-advantaged savings accounts and consistent contributions into long-term investments can provide reassurance.10 Given the range of tax benefits and incentives available for companies establishing plans, engaging a specialist advisor to examine any potential options and assess the timing for facilitating employee retirement planning may also be beneficial.

One potential strategy worth consideration is the re-enrollment of participants who may have withdrawn from the plan or ceased contributions. Market volatility may present an appropriate juncture to transition participants from potentially suboptimal allocations to a well-designed Qualified Default Investment Alternative (QDIA).

The role of guaranteed strategies

It is imperative for plan sponsors to conduct a thorough review of investment options within the plan, including the asset allocation strategy of the target date solution and the QDIA, if these are distinct. Specifically, plan sponsors can seek to enhance participant outcomes by engaging in discussions with advisors regarding the potential incorporation of guaranteed accumulation strategies within their target date offerings. By integrating guaranteed income elements, plan sponsors can offer participants a more robust and potentially reassuring investment option, especially during periods of market uncertainty.

401(k) plans, originally designed as supplemental savings plans, have evolved to become primary retirement savings instruments. However, there is a growing recognition that these plans may be disproportionately focused on asset accumulation, with limited provision for lifetime income options.

While target date products remain an important and popular retirement savings tool with both plan sponsors and their employees, there is an emerging trend toward incorporating more lifetime income options to better balance retirees’ asset allocation. A recent survey by Nuveen and the TIAA Institute shows that 92% of participants think that it would be valuable for 401(k) plans in general to include a fixed annuity.11 Furthermore, 90% of employers who offer in-plan guaranteed lifetime income options consider them to be extremely or very valuable for their employees.8

In light of these findings, plan sponsors should consider undertaking a comprehensive review of their plan menu in collaboration with their advisors. This review should focus on identifying available guaranteed income strategies that could potentially enhance the plan’s offerings for participants. Such enhancements may provide participants with increased confidence to continue building assets while also offering visibility into potential guaranteed income streams upon reaching retirement.

Continue reading

Contact us

Endnotes

¹ Any guarantees are backed by the claims-paying ability of the issuing company. Past performance is no guarantee of future results. Guarantees of fixed monthly payments are only associated with fixed annuities.

² Sources: Employee Benefits Security Administration (EBSA), 2024, Private pension plan bulletin: Abstract of 2022 Form 5500 annual reports, U.S. Department of Labor.

³ Read more about Benefits 2.0 here: https://www.nuveen.com/global/campaigns/benefits-2- 0?type=us#view-benefits

⁴ Pension-like income refers to the income received from guaranteed-interest annuity contracts, not income provided by a defined benefit pension plan.

⁵ A target-date fund is a “fund of funds,” primarily invested in shares of other mutual funds. The fund’s investments are adjusted from more aggressive to more conservative over time as the target retirement date approaches. The principal value of a target-date fund isn’t guaranteed at any time, including at the target-date, and will fluctuate with market changes. The target date represents an approximate date when investors may plan to begin withdrawing from the fund. However, you are not required to withdraw the funds at that target date. After the target date has been reached, some of your money may be merged into a fund with more stable asset allocation. Also, please note that the target-date fund is selected for you based on your projected retirement date (assuming a retirement age of 65). Target-date funds share the risks associated with the types of securities held by each of the underlying funds in which they invest. In addition to the fees and expenses associated with the target-date funds, there is exposure to the fees and expenses associated with the underlying mutual funds as well.

⁶ The Nuveen Lifecycle Target Date Series (formerly the TIAA-CREF Lifecycle Fund Series) first included direct real estate investments in 2017. See the press release titled: “Nuveen enhances target-date fund offering with direct real estate allocation,” April 20, 2017.

⁷ Top 5 real estate manager globally based on Pensions & Investments Real Estate Managers Special Report, October 2024. Ranking included 72 real estate managers and ranked them by total worldwide real estate assets as of 30 Jun 2024. Real estate assets are reported net of leverage, including contributions committed or received but not yet invested; REOCs are included with equity; REIT securities are excluded.

⁸ PlanSponsor. 04 Apr 2025. Center for Retirement Research at Boston College. Nov 2012.

⁹ FactSet, 31 Dec 2024.

¹⁰ Dollar cost averaging does not assure a profit and does not protect against loss in declining markets.

¹¹ Nuveen and TIAA Institute Participant Sentiment Survey on Lifetime Income, 2024

¹² Opinions expressed are those of the speakers as of the date and are subject to change without notice and do not necessarily reflect Mercer’s opinions.

Before investing, carefully consider fund investment objectives, risks, charges and expenses. For this and other information that should be read carefully, please request a prospectus or summary prospectus from your financial professional or Nuveen at 800.257.8787 or visit nuveen.com.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or investment strategy and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial advisors. Financial professionals should independently evaluate the risks associated with products or services and exercise independent judgment with respect to their clients. This material, along with any views and opinions expressed within, are presented for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as changing market, economic, political, or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. There is no promise, representation, or warranty (express or implied) as to the past, future, or current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such. This material should not be regarded by the recipients as a substitute for the exercise of their own judgment. For index definitions, please visit the glossary on Nuveen.com. Please note it's not possible to invest in an index directly.

Important information on risk

Past performance is no guarantee of future results. All investments carry a certain degree of risk, including the possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Certain products and services may not be available to all entities or persons. There is no guarantee that investment objectives will be achieved. See the applicable product literature for details. Investors should be aware that alternative investments are speculative, subject to substantial risks including the risks associated with limited liquidity, the potential use of leverage, potential short sales, currency exchange rates, and concentrated investments and may involve complex tax structures and investment strategies. Alternative investments may be illiquid, there may be no liquid secondary market or ready purchasers for such securities, they may not be required to provide periodic pricing or valuation information to investors, there may be delays in distributing tax information to investors, they are not subject to the same regulatory requirements as other types of pooled investment vehicles, and they may be subject to high fees and expenses, which will reduce profits.

Nuveen, LLC provides investment solutions through its investment specialists.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA institute.

About Nuveen Lifecycle Income CIT Series

SEI Trust Company serves as the Trustee of the Nuveen/SEI Trust Company Investment Trust III and maintains ultimate fiduciary authority over the management of, and the investments made, in the Nuveen Lifecycle Income CIT Series (Lifecycle Income CIT Series).

Each fund is part of a trust operated by the trustee. The trustee is a trust company organized under the laws of the Commonwealth of Pennsylvania and wholly owned subsidiary of SEI Investments Company (SEI). The Lifecycle Income CIT Series is managed by the trustee, based on the investment advice of Nuveen Fund Advisors, LLC, the investment adviser to the trust, and Nuveen Asset Management, LLC as investment sub-adviser to the Lifecycle Income CIT Series.

The Lifecycle Income CIT Series are trusts for the collective investment of assets of participating tax qualified pension and profit-sharing plans and related trusts, governmental plans and other eligible plans, as more fully described in the Declaration of Trust. As a bank collective investment trust, the trust is exempt from registration as an investment company. A plan fiduciary should consider the funds’ objectives, risks, and expenses before investing. This and other information can be found in the Declaration of Trust and the Funds’ Disclosure Memorandum.

Annuity contracts may contain terms for keeping them in force.

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen DMAT Cart

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)