Contact us

Contact Nuveen

Thank you for your message. We will contact you shortly.

Key takeaways:

- Private market investments like private credit, real estate and real assets may enhance diversification and potential returns in defined contribution (DC) plans.

- While some private market assets come with challenges like lower liquidity and transparency, these drawbacks may be manageable — and even beneficial — within longterm retirement portfolios.

- One way to include private market investments in DC plans is through professionally managed solutions like target date funds or managed accounts, rather than offering them directly to participants.

Defining private market assets investments

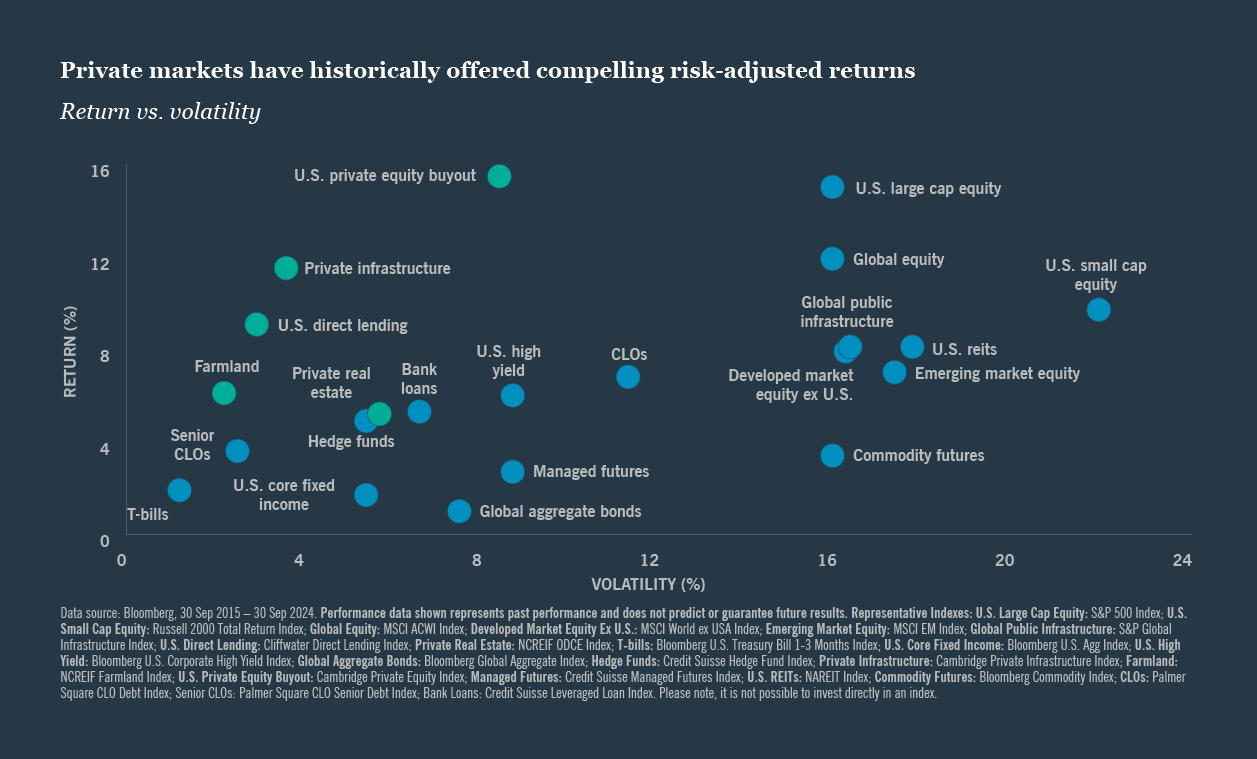

Private market investments, sometimes called alternative assets, represent a significant and relatively underutilized opportunity, often larger in scope than commonly perceived. While traditional investor portfolios typically comprise publicly traded stocks and bonds, private market investments are distinguished by their absence from public exchanges. These can include direct investments in private company equity and credit, real estate and real assets such as infrastructure or farmland. Private market investments can complement public holdings, offering diverse opportunities to potentially enhance portfolio performance.

Various private asset classes possess distinct characteristics in terms of asset type, comparable public asset class and risk/return profile.

- Private equity: Involves equity ownership in companies not listed on public stock exchanges

- Private credit: Entails lending capital to private companies through non-traditional banking channels

- Real estate: Direct investment in professionally managed real estate properties, sites and buildings that benefit from global trends

- Real assets: Investments in natural resources (e.g., farmland) and public resources such as infrastructure

Benefits

Private market investments can offer several potential benefits for DC plan portfolios. Incorporating these investments can enhance diversification, providing exposure to a broader range of the global economy and reducing reliance on traditional public equities and bonds. Many private asset classes also offer an “illiquidity premium” in the form of higher yields, which can potentially boost returns during periods when participants are not expected to access their accounts.

Private investments may also help mitigate portfolio risk through exposure to assets with different return drivers. Additionally, these investments can provide access to unique opportunities not available in public markets, offering the potential for longterm value creation. Certain private assets like real estate, farmland and infrastructure, may even serve as an inflation hedge.

Considerations and potential drawbacks

While the benefits of incorporating private market assets into DC plans can be compelling, there are also valid criticisms and concerns that plan sponsors must carefully evaluate.

First and foremost is the relative lack of transparency and disclosure requirements compared with publicly traded securities. The SEC mandates a rigorous disclosure regime for public asset classes, but disclosure from underlying private companies is often voluntary or lacking in detail. Alternative investments are typically designed for professional asset managers who have the expertise to analyze these less transparent opportunities, rather than for general retail investors.

Another common criticism is the reduced liquidity of private investments. However, this lack of immediate access can be viewed as a potential benefit specifically within the context of a DC plan. Since the assets in a DC portfolio are generally intended to be held for the duration of a participant’s working career, the reduced liquidity of alternatives may not be a significant impediment. Additionally, the higher yields often associated with illiquid private market investments can help compensate for this lack of liquidity. And in the event of an emergency need for funds, the more liquid publicly traded portion of the portfolio would typically still be available.

Implementing private assets within a DC plan

As the DC market continues to mature, plan sponsors and consultants are evaluating the benefits of traditional active asset management versus passive indexing models, often with an eye on cost savings. The nuanced discussion centers on how to optimally combine these different investment approaches. With this backdrop, well-designed blended strategies have the potential to become the new standard for default investment options, offering a balanced approach that serves the interests of both plan sponsors and participants.

Certain market segments, such as large-cap U.S. equities, are highly efficient, making it challenging for active managers to consistently outperform. In contrast, areas like emerging markets or small-cap stocks often present greater opportunities for skilled managers to add value. Private assets, in particular, represent an area where we believe active management is essential. Private real estate, private credit and other non-public assets may offer compelling diversification and enhanced income opportunities when supported by expertise and active oversight. While some sponsors attempt to use proxy, index-based strategies, such as publicly traded REITs, to gain exposure to these markets, these approaches often fall short in effectively replicating the performance and characteristics of the underlying private assets.

The cost of active management, and specifically the fee structure of private investments requiring specialized managers, is a common criticism. However, recent litigation trends have not deemed the use of actively managed funds as inherently imprudent. The key is to demonstrate a thoughtful, transparent process for selecting and monitoring investments, with a clear rationale for how each component contributes to the overall investment objective. By offering a blended approach, plan sponsors can demonstrate a commitment to both cost efficiency and investment excellence, a balance that aligns with their fiduciary responsibilities.

Embedding private assets with care

At Nuveen, we have long recognized the potential benefits that alternatives can provide within a professionally managed retirement portfolio. We have been a leader in incorporating our private market assets into our funds.6 Nuveen is a top five real estate manager, with nearly $300 billion in alternative assets under management.7

As the various government departments consider the use of private investments within DC plans, we believe that their inclusion must be done thoughtfully to avoid unnecessary fiduciary risk. We believe that these investments are typically best applied within professionally managed portfolios, such as, target date funds, insurance general accounts or carefully monitored in-plan managed account offerings.

By embedding private solutions inside professionally managed portfolios like target date funds, the end investor and plan sponsor can mitigate many of the challenges, such as the complexities and illiquidity concerns, that would accompany making these assets directly available within a plan’s investment menu.

As plan sponsors look to improve retirement outcomes for their workers, they should rely on their investment consultants to assist them with their plan’s investment menu design. This includes ensuring that their participants have access to the right mix of asset classes, both public and private, but that these are managed within professional portfolio, most easily achieved through target date funds with an embedded annuity — some of which may already include allocations to alternatives.

Nuveen has been an industry leader in private markets for decades. The question is not whether alternatives belong in DC plans, but rather how to incorporate them thoughtfully to enhance retirement security. We are well positioned to offer participants access to private assets through our target date funds and alternative-focused CITs that can be used as components within custom solutions and managed accounts.

Continue reading

Contact us

Endnotes

¹ Any guarantees are backed by the claims-paying ability of the issuing company. Past performance is no guarantee of future results. Guarantees of fixed monthly payments are only associated with fixed annuities.

² Sources: Employee Benefits Security Administration (EBSA), 2024, Private pension plan bulletin: Abstract of 2022 Form 5500 annual reports, U.S. Department of Labor.

³ Read more about Benefits 2.0 here: https://www.nuveen.com/global/campaigns/benefits-2- 0?type=us#view-benefits

⁴ Pension-like income refers to the income received from guaranteed-interest annuity contracts, not income provided by a defined benefit pension plan.

⁵ A target-date fund is a “fund of funds,” primarily invested in shares of other mutual funds. The fund’s investments are adjusted from more aggressive to more conservative over time as the target retirement date approaches. The principal value of a target-date fund isn’t guaranteed at any time, including at the target-date, and will fluctuate with market changes. The target date represents an approximate date when investors may plan to begin withdrawing from the fund. However, you are not required to withdraw the funds at that target date. After the target date has been reached, some of your money may be merged into a fund with more stable asset allocation. Also, please note that the target-date fund is selected for you based on your projected retirement date (assuming a retirement age of 65). Target-date funds share the risks associated with the types of securities held by each of the underlying funds in which they invest. In addition to the fees and expenses associated with the target-date funds, there is exposure to the fees and expenses associated with the underlying mutual funds as well.

⁶ The Nuveen Lifecycle Target Date Series (formerly the TIAA-CREF Lifecycle Fund Series) first included direct real estate investments in 2017. See the press release titled: “Nuveen enhances target-date fund offering with direct real estate allocation,” April 20, 2017.

⁷ Top 5 real estate manager globally based on Pensions & Investments Real Estate Managers Special Report, October 2024. Ranking included 72 real estate managers and ranked them by total worldwide real estate assets as of 30 Jun 2024. Real estate assets are reported net of leverage, including contributions committed or received but not yet invested; REOCs are included with equity; REIT securities are excluded.

⁸ PlanSponsor. 04 Apr 2025. Center for Retirement Research at Boston College. Nov 2012.

⁹ FactSet, 31 Dec 2024.

¹⁰ Dollar cost averaging does not assure a profit and does not protect against loss in declining markets.

¹¹ Nuveen and TIAA Institute Participant Sentiment Survey on Lifetime Income, 2024

¹² Opinions expressed are those of the speakers as of the date and are subject to change without notice and do not necessarily reflect Mercer’s opinions.

Before investing, carefully consider fund investment objectives, risks, charges and expenses. For this and other information that should be read carefully, please request a prospectus or summary prospectus from your financial professional or Nuveen at 800.257.8787 or visit nuveen.com.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or investment strategy and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial advisors. Financial professionals should independently evaluate the risks associated with products or services and exercise independent judgment with respect to their clients. This material, along with any views and opinions expressed within, are presented for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as changing market, economic, political, or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. There is no promise, representation, or warranty (express or implied) as to the past, future, or current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such. This material should not be regarded by the recipients as a substitute for the exercise of their own judgment. For index definitions, please visit the glossary on Nuveen.com. Please note it's not possible to invest in an index directly.

Important information on risk

Past performance is no guarantee of future results. All investments carry a certain degree of risk, including the possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Certain products and services may not be available to all entities or persons. There is no guarantee that investment objectives will be achieved. See the applicable product literature for details. Investors should be aware that alternative investments are speculative, subject to substantial risks including the risks associated with limited liquidity, the potential use of leverage, potential short sales, currency exchange rates, and concentrated investments and may involve complex tax structures and investment strategies. Alternative investments may be illiquid, there may be no liquid secondary market or ready purchasers for such securities, they may not be required to provide periodic pricing or valuation information to investors, there may be delays in distributing tax information to investors, they are not subject to the same regulatory requirements as other types of pooled investment vehicles, and they may be subject to high fees and expenses, which will reduce profits.

Nuveen, LLC provides investment solutions through its investment specialists.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA institute.

About Nuveen Lifecycle Income CIT Series

SEI Trust Company serves as the Trustee of the Nuveen/SEI Trust Company Investment Trust III and maintains ultimate fiduciary authority over the management of, and the investments made, in the Nuveen Lifecycle Income CIT Series (Lifecycle Income CIT Series).

Each fund is part of a trust operated by the trustee. The trustee is a trust company organized under the laws of the Commonwealth of Pennsylvania and wholly owned subsidiary of SEI Investments Company (SEI). The Lifecycle Income CIT Series is managed by the trustee, based on the investment advice of Nuveen Fund Advisors, LLC, the investment adviser to the trust, and Nuveen Asset Management, LLC as investment sub-adviser to the Lifecycle Income CIT Series.

The Lifecycle Income CIT Series are trusts for the collective investment of assets of participating tax qualified pension and profit-sharing plans and related trusts, governmental plans and other eligible plans, as more fully described in the Declaration of Trust. As a bank collective investment trust, the trust is exempt from registration as an investment company. A plan fiduciary should consider the funds’ objectives, risks, and expenses before investing. This and other information can be found in the Declaration of Trust and the Funds’ Disclosure Memorandum.

Annuity contracts may contain terms for keeping them in force.

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen DMAT Cart

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)