Contact us

Contact Nuveen

Thank you for your message. We will contact you shortly.

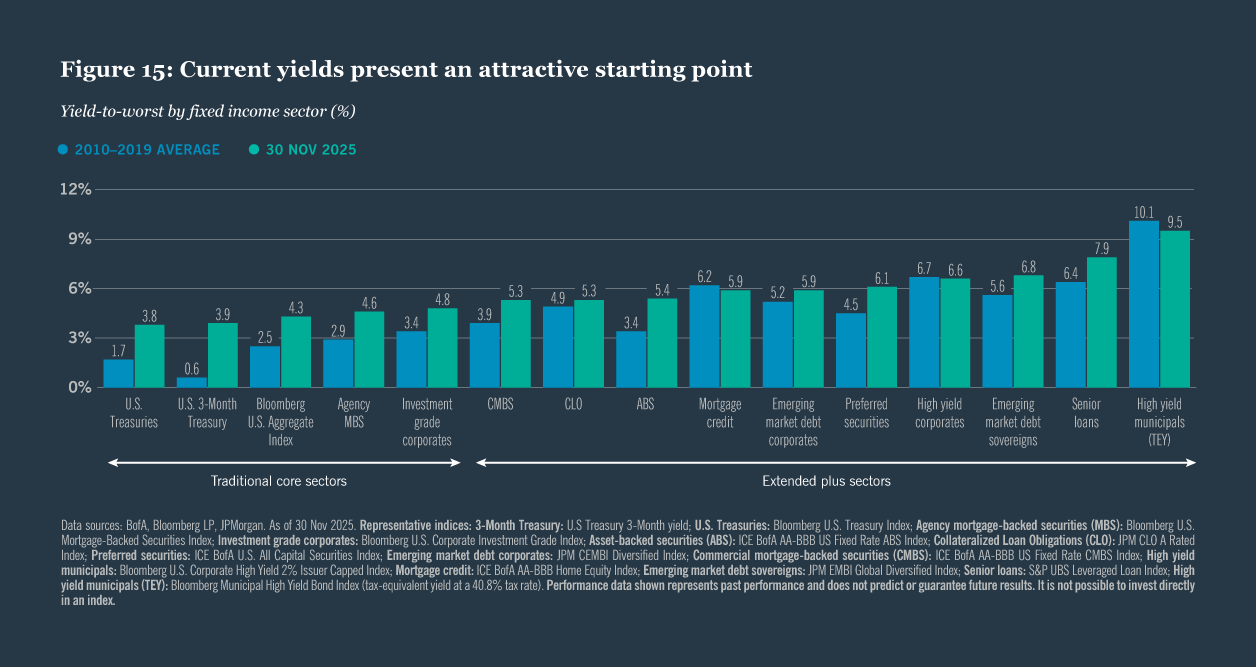

Explore by sector

- Leveraged finance

- Emerging markets debt

- Securitized credit

- Preferred securities

- Tax exempt municipal bonds

- Taxable municipal bonds

- Multi-sector credit

Leveraged finance

Collateralized loan obligations (CLOs)

In an environment where traditional credit valuations are rich but economic fundamentals remain sound, CLOs stand out as a way to capture attractive carry without taking incremental credit risk. CLOs typically offer spread premiums versus similarly rated corporate bonds. For example, in the single A credit rating bucket, corporate debt offers spreads of around 66 bps, while CLOs have spreads of around 186 bps — for a similar amount of credit risk.2 This spread premium largely reflects structural and liquidity complexity — investors are compensated for analyzing how CLO structures operate and for holding instruments that may be less liquid than corporate bonds — an A-rated CLO still has liquidity, but it is less liquid than an A-rated corporate bond.

Complexity does not translate into higher credit or default risk. In fact, CLOs have historically demonstrated superior default performance compared to similarly rated corporate credit, supported by the structural protection and the strength of the underlying collateral. Each CLO is a diversified portfolio of 200+ broadly syndicated senior loans from well-known companies, structured into tranches with varying risk/return profiles ranging from AAA-rated debt to unrated equity. By spreading risk across a large number of loans in different industries, CLOs mitigate the impact of poor performance by any single company or industry, making them a valuable addition to portfolios seeking greater stability.

Additionally, CLOs are actively managed, enabling managers to sell underperforming loans and purchase higher-quality assets or those offering more attractive relative value. This flexibility can be especially valuable during periods of market volatility, when loans from fundamentally strong companies become undervalued, creating opportunities to buy higher-quality assets at discounted prices and capitalizing on the underlying economic resilience of borrowers. Looking into 2026, we expect bouts of volatility to continue, and we have constructed our portfolios to be defensive and positioned to take advantage of price movements to enhance returns for our clients.

Senior loans

Under the forecast of minimal recession risk, the broadly syndicated loan (BSL) market is well positioned from a fundamental credit standpoint and could potentially provide economic resilience for investors. Throughout 2025, BSL default rates have moved lower from the peak reached in late 2024, reflecting positive fundamental momentum, and we expect this trend to continue into 2026. The average BSL borrower is growing revenue and EBITDA by approximately 3% and 4%, respectively, on a year-over-year basis, while the average interest coverage ratio stands at 3.0x, up year-over-year.3

Credit selection remains critical, as dispersion among fundamentals remains within the lower quality segment of the BSL market. We believe significant incremental yield and return potential is available, and we actively manage the risks and opportunities within this cohort.

The BSL market continues to drive high levels of income while delivering low volatility and diversification for investors (Figure 8). With rate volatility expected to remain, especially when considering the shape of the yield curve, the floating rate nature of senior loans affords investors the opportunity to insulate from rate risk, while benefiting from high levels of income associated with credit risk poised to perform in a slow, albeit positive, economic environment.

The BSL market remains highly transparent, and with the market growing to $1.5 trillion in size, daily trading volume is approaching $4 billion. In addition, we expect increased mergers and acquisitions (M&A) and leveraged buyout (LBO) activity to drive new issue in the BSL market, highlighting the strategic importance of the asset class. Finally, we expect continued demand from investors across the globe, especially those under-allocated to the asset class, or over-allocated to riskier segments of the credit landscape.

The BSL market is yielding close to 8% on a yield to 3-year basis,4 even when incorporating the market’s expectations for the path of short-term rates, delivering to investors one of the highest yielding asset classes within the fixed income markets. While credit spreads have tightened throughout 2025, we believe investors are being compensated for the inherent risk in the market — default risk. Active management will continue to be critical in avoiding downside volatility while also taking advantage of the liquidity in the market to find opportunities within the discounted loan cohort, incrementally adding significant yield and total return potential on top of the high levels of income the broad BSL market offers investors.

U.S. high yield corporates

The U.S. high yield bond market offers attractive absolute yields, currently around 7%.5 Issuer fundamentals have remained healthy, with net leverage ratio at 3.9x and the interest coverage ratio at 4.1x as of third quarter 2025.5 The market composition has evolved structurally, with an increasing presence of larger, publicly traded BB-rated companies, which fundamentally reduces default risk for the overall high yield market. Default rates are projected at 1.75% in 2026, below long-term averages and in line with 2025, despite ongoing market volatility across the credit landscape (Figure 9). Importantly, much of the loss associated with projected default activity is already priced into the market. Corporate balance sheets remain resilient, with revenue and EBITDA growth trends continuing; however, credit selection remains critical within lower quality segments of the high yield market.

Fiscal policy dynamics and monetary easing are expected to influence the high yield market in 2026. Trade policies, immigration changes and regulatory reforms could affect economic activity and the Fed’s easing cycle, contributing to performance differences across sectors and issuers. Gross issuance for 2026 is forecasted to rise 15% to $375 billion, driven by refinancing needs and increased M&A activity, increasing the opportunity set for active managers. With Fed rate cuts anticipated to bring the Fed funds rate to approximately 3.25% by mid-year 2026, we believe credit spreads can continue to tighten amid reduced volatility. In addition, the high yield market remains anchored around three years of duration, providing potential positive convexity to falling short term rates, while being insulated from longer-term rates where we anticipate continued volatility.

While credit spreads remain tight to long-term averages, economic resilience alongside the fundamental and technical picture for high yield reflects the rationale for tighter spreads. We expect high yield spreads to remain range bound around current levels throughout 2026, and coupled with high coupons, could result in a full year total return estimate of 6%–8%. Absent a severe economic downturn, high yield bonds should continue to deliver attractive risk-adjusted returns. We believe dispersion among issuers will continue, allowing active managers with robust credit underwriting to capitalize on relative value opportunities and dig deeper for diversification across the credit landscape.

Emerging markets debt (EM)

The boundaries separating developed markets (DM) and EM are becoming increasingly blurred, presenting compelling investment opportunities as DM grapples with issues that traditionally have been confined to EM. Rising fiscal deficits, above target inflation, concerns over central bank independence, and weakening currencies have been tagged as EM risks historically, resulting in a yield premium demanded by investors. Yet, in recent years, many DMs have seen a rise in the same concerns, without the same degree of risk premium demanded.

Concerns over fiscal trajectory and broader policies are plaguing countries throughout DM from the U.K. to Japan, but EM economies have been demonstrating improving fundamentals and increased prudence in central bank policymaking. EM countries, as well as companies, are often compelled to exercise greater caution than their DM counterparts. We can see the relative strength as EM sovereigns exhibit much lower debt-to-GDP ratios and EM corporates maintain significantly lower net leverage compared to DM, though select sectors could be pressured by China’s competitive export orientation. We have started to see some repricing of the EM premium amid strong recent returns, but EM external debt, both sovereign and corporate, offers an average of nearly 100 bps of additional yield versus DM on a ratings-adjusted basis (Figure 10).

EM investing requires a country-level view as the starting point for determining bottom-up expression in terms of issuer or issue. Using our proprietary country cohort lens, we identify countries where extension into EM corporates is most appropriate. The best opportunities for corporate extension are generally within the Steady cohort. We are more cautious within Frontier where our sovereign team spends significant time, and there is often sufficient performance divergence potential, and an embedded spread premium, offering little motivation to extend to corporates.

EM local has returned +17.5% with foreign exchange (FX) contributing nearly half of that figure.6 As DM concerns intensify, EM local currency debt appears positioned to continue to outperform. For investors seeking yield and spread opportunities, while expanding their diversification, EM’s fundamental strength looks increasingly attractive. With risks of a higher dollar subsiding for now, this will benefit hard currency investors too with an improvement in debt servicing ability and inflation dynamics.

Securitized credit

Securitized credit can offer compelling investment opportunities in 2026 for investors seeking diversification beyond traditional corporate credit (Figure 11).

Securitized credit should provide lower correlation to corporate earnings, resilience to tariffs and some exposure to floating rate or shorter-duration investments, reducing the potential impact of steeper curves. Securitized credit’s contractual cash flows and tangible collateral also provide relative stability as questions intensify about the fiscal sustainability of developed markets.

Mortgage-backed securities (MBS) present continued opportunity, with robust household balance sheets and sustained rigor in credit underwriting representing key support for the sector. Agency MBS represents a compelling blend of tariff remoteness, liquidity and high-quality income relative to U.S. Treasuries. Non-agency MBS continues to benefit from structural housing shortages and disciplined underwriting standards. U.S.-focused collateral provides insulation from global trade disruptions and geopolitical risks.

Asset-backed securities (ABS) have seen record supply for several years in a row as investors seek yields backed by fundamentally sound consumers, robust employment and ongoing commercial financing requirements. While signs of weakness are emerging in lower-quality credit, opportunities continue for investors willing to participate in esoteric collateral types. The highest-quality opportunities should benefit from increased investor focus.

Commercial mortgage-backed securities (CMBS) should benefit from ongoing real estate tailwinds; valuations have found floors, demand has stabilized and oversupply has generally abated. Anticipated interest rate cuts should also provide further support for the sector and lower the cost of debt for many borrowers.

Preferred securities

An economically resilient sector, preferred securities provide investors with attractive tax-advantaged income and exposure to primarily high-quality issuers. The sector offers strong fundamentals with an average security-level rating of BBB and average issuer ratings typically three to five notches higher. We invest primarily in highly regulated sectors (e.g., banks, insurance companies and utilities) that offer investors the added assurance of external oversight. Preferreds are a less traditional, higher-yielding credit sector. Allocating to preferred securities can also enhance overall portfolio diversification because of the sector’s low correlation to other fixed income and equity categories.

Banks, the largest sector of the universe, are in a position of notable strength. U.S. banks had favorable 2025 stress test results, solid earnings and conservative risk positioning. Insurance, the second largest sector, also has a positive outlook. Insurers have historically high risk-based capital levels, the added assurance of regulatory oversight, an inherent benefit from higher interest rates and near record setting sales of annuity products for the past three years. Both industries are only indirectly impacted by tariffs. While new supply has increased, it should not meaningfully affect valuations. Much of the new issuance comes from non-bank financials or corporate hybrid structures that are eligible for traditional investment grade or high yield corporate indexes, attracting a broader investor base beyond dedicated preferred investors. This new supply has been easily absorbed.

Spreads remain below longer-term averages but above historical lows. We believe underlying fundamentals and supportive technicals can support current spread levels. Despite recent outperformance, we continue to favor $1000 par preferreds for their higher option-adjusted spreads, attractive income levels and lower duration (Figure 12). In contrast, $25 par preferreds tend to be more volatile, less liquid, longer duration and currently trade at much tighter spread levels.

Tax-exempt municipal bonds

We have a favorable view of tax-exempt municipals, especially in longer maturities, and we expect the municipal rally to continue. High starting yields, paired with resilient credit fundamentals and a solid technical foundation, should drive positive returns for municipals in 2026 (Figure 13).

As the fiscal over monetary takeover theme materializes, federal deficit spending headlines will drive U.S. Treasury yield volatility, but municipal bonds are more insulated as the municipal yield curve is significantly steeper than the Treasury curve. Municipal 20-year bonds outyield 10-year bonds by 112 bps, while Treasury counterparts only offer 60 bps of yield pickup at the same tenors (as of 25 Nov 2025). This relationship is likely to normalize in 2026, and we favor taking duration in municipals.

Municipal credit fundamentals are solid. Most municipal borrowers are essential service providers that continue to earn revenues when federal support wanes. Further, borrowers possess significant flexibility to balance budgets via taxes, service cuts and other tools. Credit quality is high after several strong years of upgrades, yet municipal spreads are wider than where they began 2025.

Lower-rated municipal issuers offer more room for compression. The yield spread on the Bloomberg Municipal 10-year High Yield Index stands at 301 bps, which is 71 bps wider than the five-year average (as of 28 Nov 2025). With economic resilience supporting markets, we see no major catalyst for spread correction.

Municipal market technicals are a critical source of price performance. 2025 set record levels of supply, and the market demonstrated tenacity as it navigated heavy deal flow. We expect 2026 supply to remain elevated while demand will continue to grow as investors move out of money market funds into higher-yielding municipals. The recovery staged in late 2025 is likely to continue and should reward early movers.

Taxable municipal bonds

Taxable municipals are poised to deliver compelling performance in 2026 as strong technical tailwinds and attractive valuations converge (Figure 14). Anemic taxable municipal supply trends are expected to continue in 2026, driving scarcity in the market. We do not foresee supply growth until longer-term rates fall sustainably and taxable refunding becomes economically attractive again. Flows to the asset class remain robust and Build America Bonds’ continued use of extraordinary redemption provisions (ERPs) should underpin demand.

As investors dig deeper for diversification in 2026, high absolute yields for taxable municipals offer attractive relative value versus corporates with typically lower default risk. With fiscal sustainability and policy questions rising to the forefront, headline-driven episodic volatility will be short lived and should present buying opportunities in municipals.

Economic resilience and solid credit fundamentals should continue to support municipals, justifying current valuations. Yet, we see relatively more value in BBB and lower-rated taxable municipals where spreads are wider than where they began the year. We see no immediate impetus for widespread credit deterioration but expect dispersion among issuers, particularly in higher education, health care and large urban centers. Disciplined credit selection should be rewarded.

Taxable municipals enter 2026 with strong momentum, which we expect to continue as market conditions remain favorable.

Multi-sector credit

As we enter 2026, multi-sector fixed income investors face an easing monetary policy cycle paired with full valuations across traditional credit sectors.

In developed markets, high levels of deficit spending remain unaddressed and we expect continued supply pressure to push long-end rates higher. As such, we are maintaining a duration posture significantly lower relative to standard benchmarks.

Emerging markets stand to benefit as developed market vulnerabilities come into focus. Questions about fiscal sustainability and institutional credibility — traditionally emerging market concerns — are increasingly being applied to advanced economies. These blurred lines create opportunities across emerging market sovereign, corporate, and local currency debt as investors recognize improving relative fundamentals.

Going lower in quality in corporate credit is unlikely to benefit investors because spreads are tight relative to historical standards. We’re looking beyond traditional credit to sectors like securitized, emerging markets and preferred securities, where complexity premiums and wider spreads reward credit specialists who can accurately identify value.

We do not believe a recession will occur in 2026, and there is still some room to take credit risk within portfolios. While we are taking more credit exposure in less traditional sectors, recession resistant sectors like MBS, higher quality EM sovereigns and IG corporate utilities can offer downside protection against spread widening events.

Continue reading

Contact us

You are on the site for: Financial Professionals and Individual Investors. You can switch to the site for: Institutional Investors or Global Investors

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen DMAT Cart

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)