Contact us

Contact Nuveen

Thank you for your message. We will contact you shortly.

Key takeaways | Second quarter outlook

- Despite a turbulent first quarter, the steep municipal yield curve may reward investors who extend duration, with 20-year AAA yields above 4.00%.

- With reinvestment demand projected to surge 40% and net supply expected to remain negative, technical conditions favor municipal total returns through year end.

- Security selection in the health care and higher education sectors presents an opportunity for investors willing to look past current pressures.

Volatility and value define the muni outlook

Munis returned 2.20% through February before a sharp rate-driven selloff in March pushed the quarter to -0.18%.

In our view, investors have not missed the muni rally, and recent weakness in the asset class may offer an opportunity to increase exposure at attractive valuations.

Taxable-equivalent yields (TEY) for munis are in the top quartile of their 10-year history.¹ The broad municipal index offers a TEY of 6.37% versus 4.57% for the Bloomberg U.S. Aggregate Bond Index. Municipal credit spreads are also relatively attractive compared to corporates, with muni spreads in the 70th percentile versus the 15th percentile for investment grade corporates.¹

Municipals lagged the Bloomberg U.S. Aggregate Bond Index by more than 400 basis points (bps) at various points during 2025 and, while they have since recovered ground, still trail the broader taxable index by 319 bps as of quarter end. History shows that gaps of this magnitude have been followed by rapid recoveries and subsequent outperformance of a symmetrical approximately 400 bps.² If history is a guide, current market conditions may represent an attractive entry point for investors positioned to capture the recovery.

Record demand fuels a powerful market rally

Municipal fund flows surged 113% year-over-year in the first quarter. The market has gathered $25.3 billion in 2026 through February, the best start to any year on record. Since 1993, positive first quarter flows have signaled net positive annual flows for the calendar year 70% of the time.³ Investor flows are important because municipal total return is 79% correlated to positive inflows (Figure 1).⁴

We expect demand to continue, supported by ample cash on the sidelines, high starting yields and solid municipal credit conditions. But recent headwinds are worth monitoring, stemming from geopolitical uncertainty and a U.S. Federal Reserve that appears content holding interest rates steady for 2026.

Money market fund assets remain at historically high levels. On average, it has taken 18 to 22 months for sustained money market outflows to materialize following an easing cycle.⁵ The end of the first quarter marks the 19th month since the beginning of the current rate reduction cycle.

The Fed's most recent cut pushed after-tax money market yields below 2.75% for investors in the 24% tax bracket. With inflation hovering near 2.4%, cash is unlikely to cover the growth of living expenses for most investors. Municipal flows for the first quarter have strongly favored longer duration and high yield bonds, suggesting investors are keen to lock in historically attractive yields while credit conditions remain solid.

A healthy new issue market may reward patient investors

The new issue market is running slightly ahead of the historically high pace set in 2025. Total new issuance of $142 billion is up 11% year-to-date, though supply has underwhelmed against forecasts for an even more robust calendar.

We expect the pace of issuance to accelerate from the second quarter through year end and believe $600 billion in new issue supply is attainable (Figure 2). As issuers contend with higher project costs due to inflation, new issue deals are larger than in years past. The result is more attractive valuations on new deals and ample investment opportunities.

New issue deals have historically offered investors a meaningful spread over secondary purchases - a concession that we think should compound into real value and tax savings over time.

General obligation and local school districts were the top two absolute issuing sectors during the quarter. Within revenue sectors, hospitals, higher education and gas-prepay topped the charts. Hospitals and gas-prepay year-over-year issuance was up 66% and 32%, respectively. Higher education - while down 11% from extremely high levels in the first quarter of 2025 due to federal tax policy uncertainty - remained well ahead of its 10-year average issuance.

We expect to see healthy issuance growth in 2026 across the market, as waning fiscal stimulus and federal funding reductions push more projects toward public financing markets than at any point in recent years.

The gas-prepay sector is a nascent and growing segment now comprising more than 5% of the municipal index with roughly $100 billion outstanding. These bonds involve financial services counterparties and complex structures that command higher yields to compensate for additional risk. They are not traditional muni bonds financing essential service monopolies. As such, we are highly selective in this sector and believe these bonds are best suited to well-diversified portfolios.

Despite new supply, reinvestment demand from maturing bonds, callable bonds and coupons is projected to surge 40% compared to last year. Maturity and coupon dates are projected to increase significantly through the third quarter. As reinvestment demand continues to outpace new issuance, we expect the market to remain in a net negative supply environment that should support total returns.

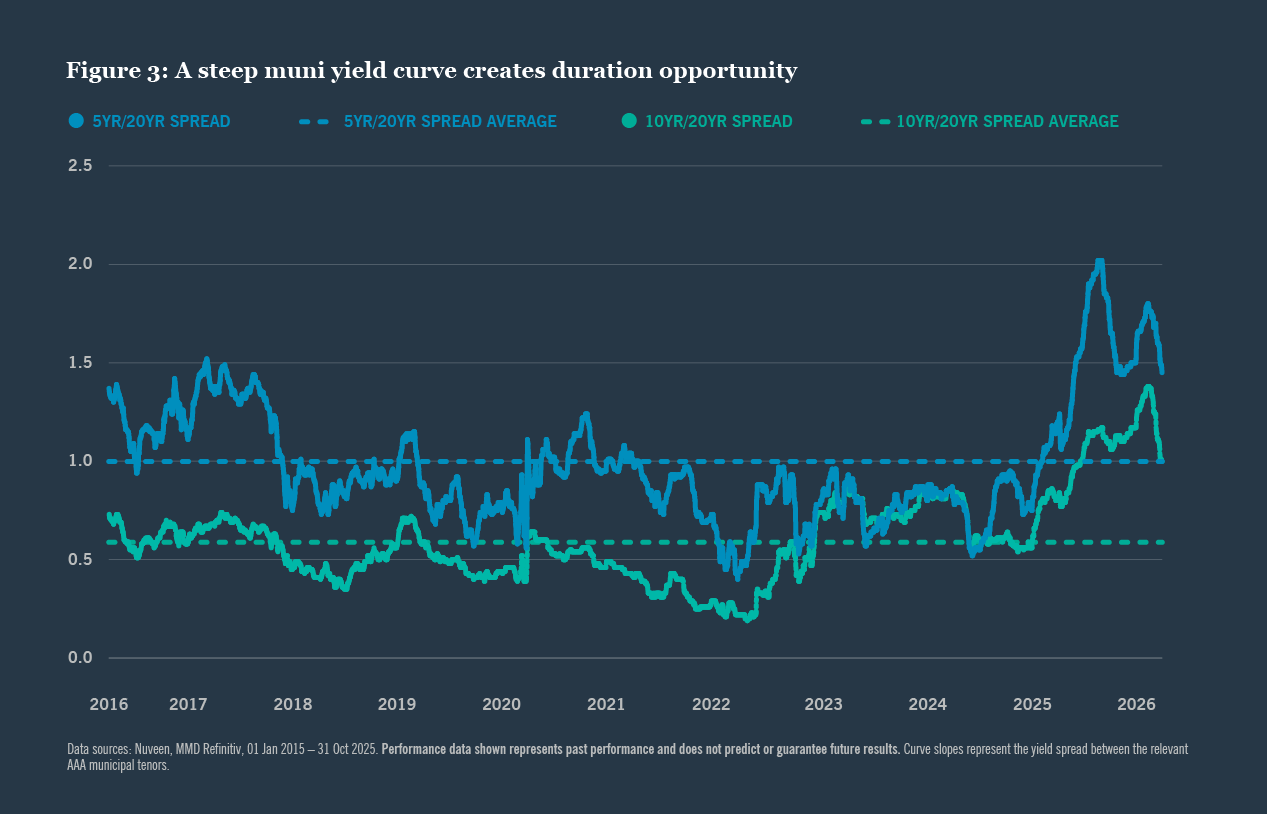

A steep yield curve rewards duration extension

The 20-year AAA municipal bond yield now tops 4.00%, offering a yield pickup of 1.45% over 5-year AAA bonds (Figure 3). The combination of 20-year municipal yields above 4.00% and a spread between 5- and 20-year municipals of more than 1.25% has occurred less than 5% of the time over the last 15 years.⁶

This asymmetric risk-return profile further supports the case for extension: the Bloomberg Municipal 20-Year Index reflects 13.61% upside potential if rates fall 100 bps, versus -4.72% downside if rates rise 100 bps. Starting yields are 1.30% higher than the 15-year average - meaningful given that income has historically comprised nearly 84% of municipal total returns.⁷

By comparison, 20-year Treasuries offer a yield pickup of only 0.96% over 5-year bonds, well below the 1.45% available in municipals. We favor extending marginal duration in municipals over Treasuries.

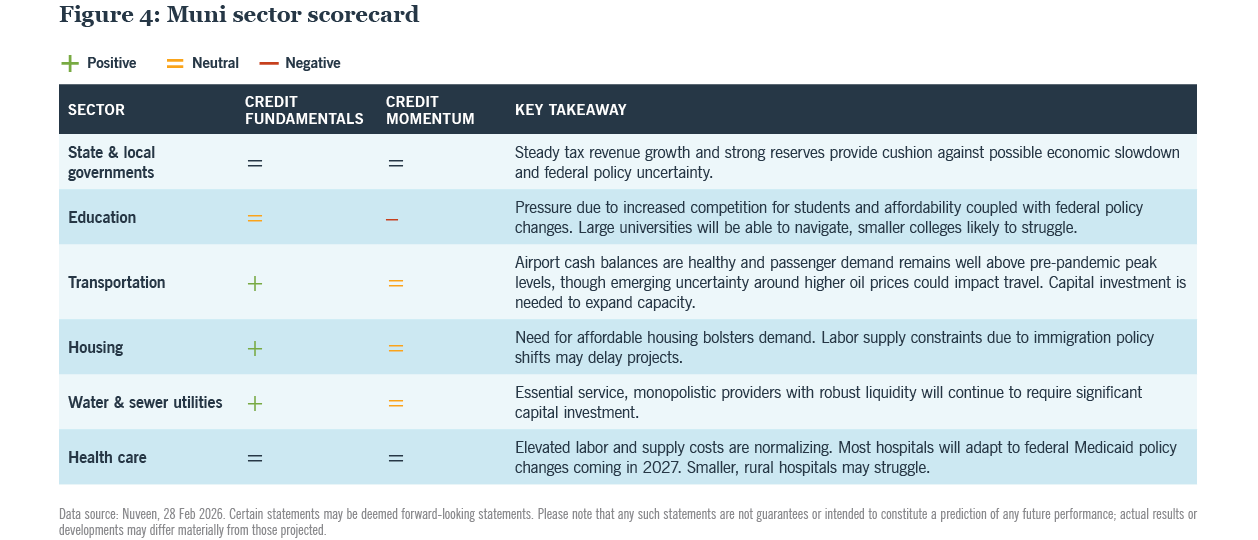

Credit divergence creates opportunity across muni sectors

Federal policy shifts are creating uneven pressures across the municipal market. For selective investors, that divergence may create opportunity. We see compelling cases for active sector selection in higher education and health care, while strong liquidity and essential service sectors continue to anchor broader credit resilience.

Colleges and universities remain vulnerable to federal policy risk on multiple fronts, and current credit spreads across the higher education sector reflect these pressures. The One Big Beautiful Bill Act (OBBBA) limits federal student loan borrowing, which may weigh on enrollment and affordability. Meanwhile, the cancellation of federal research grants constrains university finances and their ability to attract students and faculty.

Even if policy concerns fade, we expect bond issuance to remain elevated, driven by deferred maintenance, heightened competition for students and rising project costs. Elevated issuance and well-publicized headwinds have pushed spreads wider, and rigorous credit analysis could help investors capture additional yield.

Health care faces mounting pressure from rising costs and shifting federal policy. The expiration of ACA premium subsidies in 2025 contributed to a 5% decline in 2026 enrollment. Beginning in 2027, OBBBA will reshape Medicaid eligibility and is expected to reduce beneficiaries by 11 million, lowering federal matching dollars for states and leaving hospitals to absorb a larger share of uninsured patients.

Our credit team tends to favor health care credits with leading market positions, multi-state operations and strong physician alignment - issuers we believe may offer adequate compensation for the increasingly challenging operating environment.

State and local governments maintain robust liquidity, with median rainy day fund balances projected to reach 14% by FYE26, up from a pre-pandemic average of 8%. Total state and local tax revenue increased 5.4% in 2025, broadly outpacing individual state projections, as most states took a conservative budget approach in anticipation of federal policy and funding uncertainties.

Fiscal year 2027 budget season is well underway. While many proposed state and local budgets reflect deficits, we view these as opening positions rather than final outcomes. Many state and local governments are constitutionally required to pass balanced budgets and have several levers available, including raising tax rates, instituting new taxes, reducing expenditures and drawing down reserves.

New York City's preliminary FY27 budget illustrates this process well. The mayor identified an initial $5.4 billion gap and proposed two closing scenarios; the city council will offer an alternative, followed by months of hearings and budget negotiations. A compromise is expected by the early July deadline. Strong liquidity, revenue-raising capacity and expenditure flexibility support credit resilience in tax-backed sectors despite headline volatility.

Revenue sectors can be more vulnerable to economic shifts, and we favor those that function as essential service monopolies. Water and sewer, electric utilities, and transportation are prime examples. Water and sewer issuers generally demonstrate strong liquidity and debt service coverage and have rate-setting powers that allow them to adjust user charges over time. We believe sectors that combine operational stability with pricing flexibility are well-positioned to navigate both economic and geopolitical uncertainty.

Affordability has become a defining issue across the United States, shaping political discourse and driving election outcomes. Congressional momentum is building around affordable housing, with bills such as the 21st Century ROAD to Housing Act and the Affordable Homes Act pending approval. President Trump recently signed an executive order restricting large institutional investors from buying single-family homes.

Municipal bonds directly support affordable housing development while offering investors an opportunity for tax-exempt income. However, structural features such as prepayment risk, credit enhancements, collateral and project-level finances can create meaningful differences in risk and return. Rising supply in the sector may create opportunity, and evaluating these structural complexities through thorough due diligence will be essential.

We would consider any short-term market dislocations as an opportunity to add exposure at current valuations.

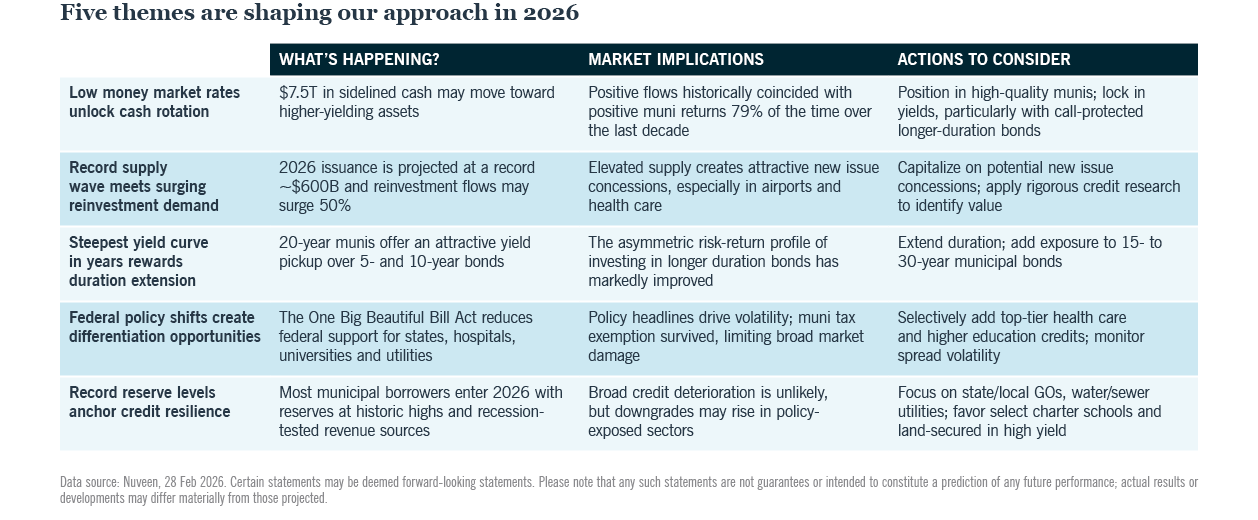

Outlook: Use near-term volatility as a tactical opportunity in 2Q

We suggest investors consider staying invested and use any short-term market dislocations as a tactical opportunity to add exposure at current valuations. The steep yield curve makes extending maturity profiles - particularly into 20-year-plus bonds - an effective way to capture additional yield and long-term value. Selective allocation to higher education and health care bonds may also reward patient investors, as sector-level policy concerns have driven spread widening that we believe overstates the fundamental credit risk in many of these issuers.

Sector fundamentals diverge amid shifting federal policy

The muni sector scorecard shows our views on credit fundamentals, momentum and valuations for major municipal sectors (Figure 4).

Download the full PDF

Related articles

Contact us

You are on the site for: Financial Professionals and Individual Investors. You can switch to the site for: Institutional Investors or Global Investors

Endnotes

1 Bloomberg L.P., 26 Mar 2026.

2 Morningstar Direct, 01 Jan 2015 - 31 Dec 2025. Fund flows and performance are cumulative YTD figures for each calendar year.

3 Morningstar Direct, 01 Jan 2015 - 31 Dec 2025.

4 Bloomberg, L.P., ICI, Nuveen, 31 Mar 2026. Weekly correlation using ICI municipal bond estimated weekly net new cash flow and the Bloomberg Municipal Bond Index Total Return Index.

5 Bloomberg L.P. and ICI, based on trailing 6- and 12-month net money market flows since 2000.

6 Nuveen, MMD Refinitiv, 31 Mar 2011 - 31 Mar 2026.

7 Nuveen, Bloomberg L.P., 31 Dec 2010 - 31 Dec 2025.

Sources

Gross Domestic Product: U.S. Department of Commerce. Treasury Yields and Ratios: Bloomberg (subscription required). Municipal Bond Yields: Municipal Market Data. Open-end fund flows: Investment Company Institute. Municipal Issuance: Siebert Research. Defaults: Municipals Weekly, Bank of America/Merrill Lynch Research. State Revenues: The Nelson A. Rockefeller Institute of Government, State Revenue Report. State Budget Reserves: Pew Charitable Trust. Global Growth: International Monetary Fund (IMF) and the Organisation for Economic Co-operation and Development (OECD). Standard & Poor’s and Investortools: http://www.invtools.com/. Flow of Funds, The Federal Reserve Board: https://www.federalreserve.gov/releases/z1/default.htm. Payroll Data: Bureau of Labor Statistics. Bond Ratings: Standard & Poor’s, Moody’s, Fitch. New Money Project Financing: The Bond Buyer. State revenues: U.S. Census Bureau.

NASBO Fall 2025 Fiscal Survey; CMS.gov; New York City February 2026 Financial Plan.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her financial professionals.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Performance data shown represents past performance and does not predict or guarantee future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. For term definitions and index descriptions, please access the glossary on nuveen.com. Please note, it is not possible to invest directly in an index.

Important information on risk

Investing involves risk; principal loss is possible. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Investing in municipal bonds involves risks such as interest rate risk, credit risk and market risk. The value of the portfolio will fluctuate based on the value of the underlying securities. There are special risks associated with investments in high yield bonds, hedging activities and the potential use of leverage. Portfolios that include lower rated municipal bonds, commonly referred to as “high yield” or “junk” bonds, which are considered to be speculative, the credit and investment risk is heightened for the portfolio. Bond insurance guarantees only the payment of principal and interest on the bond when due, and not the value of the bonds themselves, which will fluctuate with the bond market and the financial success of the issuer and the insurer. No representation is made as to an insurer’s ability to meet their commitments. This information should not replace an investor’s consultation with a financial professional regarding their tax situation.

Nuveen is not a tax advisor. Investors should contact a tax professional regarding the appropriateness of tax-exempt investments in their portfolio. If sold prior to maturity, municipal securities are subject to gain/losses based on the level of interest rates, market conditions and the credit quality of the issuer. Income may be subject to the alternative minimum tax (AMT) and/or state and local taxes, based on the state of residence. Income from municipal bonds held by a portfolio could be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service or state tax authorities, or noncompliant conduct of a bond issuer. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

Taxable-equivalent yields are based on the highest individual marginal federal tax rate of 37%, plus the 3.8% Medicare tax on investment income. Individual tax rates may vary. Inflation rate used is the PCE Deflator, which is removed from the after tax income of the 3 month T-bill yield, resulting in an after tax and after inflation rate for cash.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Nuveen, LLC provides investment solutions through its investment specialists.

This information does not constitute investment research as defined under MiFID.

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen DMAT Cart

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)