Contact us

Contact Nuveen

Thank you for your message. We will contact you shortly.

Duration: a measure of bond price volatility

How do maturity and coupon rate affect volatility? Both determine how quickly you, the bondholder, get your money back. The longer you must wait to get your principal back, the more the price of your bond will fluctuate with a given change in interest rates. This effect is lessened by the receipt of coupon payments over the life of the bond. A higher coupon rate means you get a higher portion of your total return prior to maturity in the form of interest payments.

Bond volatility refers to the degree of price fluctuation over time, determined by changes in interest rates, credit risk, liquidity and market sentiment. However, changes in interest rates have the most significant impact on volatility. One of the first things one learns about bonds is that their prices increase when interest rates decline and decrease when interest rates rise.

A bond’s volatility depends on two factors: its coupon rate and when it will be retired (at maturity or call date). Other things being equal, the general rule is that:

- The longer the time until retirement, the greater the price volatility.

- The lower the coupon rate, the greater the price volatility.

So, if two bonds have the same maturity (assuming no call options), the one with the lower coupon will be more volatile. On the other hand, if two bonds have the same coupon rate, the one with the longer maturity will be more volatile.

But how do we compare the volatility of two bonds with different coupon rates and maturities? We use duration.

In the calculation of duration, each payment to the bondholder is multiplied by the amount of time that will elapse until that payment is received. But there is a twist — duration is based not on the time-weighted cash amount of each payment, but the time-weighted present value of each payment.1

Once you have added up all the time-weighted present values of the payments, you divide that number by the price of the bond (which is the sum of the unweighted present values) and the result is duration, a measure of time. This measurement aims to calculate the average amount of time it takes to receive the present value of your investment, otherwise referred to as Macaulay duration.

sum of

(present value of each payment x

time until that payment is received)

Duration = ____________________________

price of bond

For example, a par bond due in 10 years with a 3.00% coupon would have a duration of 8.71 years, calculated as follows:

871 dollar-years

______________ = 8.71 years

100 dollars

The 871 dollar-years in the numerator is the time-weighted present value of the various coupon payments and the final principal payment. Alternatively, if that bond had a 4.00% coupon and a dollar price of 108.58, the duration would be lower:

914 dollar-years

______________ = 8.42 years

108.58 dollars

Duration as a predictor of price changes

Duration has a very useful quality. With a slight modification (dividing by one plus the semiannual yield of the bond) the duration number can estimate how much a bond’s price will change in response to changing interest rates. If you multiply the new “modified duration” by the assumed change in interest rates, you can approximate the percentage change that will occur in the bond’s price.

For example, consider again the 3.00% par bond due in 10 years (with no call options). That bond would have a modified duration of 8.58 years (8.71 divided by 1.015). On the basis of duration, a bond with a modified duration of 8.58 years would be expected to increase in value by approximately 0.858% to $100.858 if yields decline by 10 basis points (0.10%). In fact, a more accurate estimate of the positive price movement would be $100.863 as a result of a characteristic of bonds known as convexity, which grows more impactful as the estimated change in interest rates increases.

The effects of coupon and maturity

In our previous example, the 3% par bond with a 10-year maturity had a modified duration of 8.58 years. If a bond with the same coupon rate and price had a maturity of 11 years, its modified duration would be 9.31 years. The longer the time until retirement, the greater the price volatility. If the coupon were 4.00% instead, but with the same 3.00% yield and 11-year maturity, the modified duration would be reduced back to 8.97 years. The larger the coupon rate, the shorter the duration.

Reducing the coupon rate to zero makes the duration equal to maturity. This is logical since the full amount of one’s investment return will be received in one lump sum when the bond matures, which maximizes sensitivity to rates as there are no payments to reduce the average time it takes to recover the present value of the investment. As a general rule, bonds that pay interest prior to maturity will have a duration that is shorter than their years to maturity as their cash flows prior to maturity from the coupon payments pull its duration below the maturity line.

For municipal bond investors, one dollar of tax-exempt interest is worth more after tax than one dollar of capital gain. Under IRC Section 103, municipal bond interest is excluded from federal gross income while capital gains remain taxable based on holding period and tax bracket. Additionally, municipal bond interest is excluded from state and local taxable income depending on residency and the bond’s state of issuance. At the highest federal marginal rate of 37%, this exemption delivers a meaningful advantage over long-term capital gains, which are taxed at rates up to 20%.

Two critical rules govern how gains are taxed in the municipal market. First, under the market discount rule of IRC Sections 1276–1278, bonds purchased at a discount exceeding the de minimis threshold — generally 0.25% of face value per full year remaining to maturity — have their accreted discount reclassified from capital gain to ordinary income upon sale or redemption. This distinction grows increasingly relevant as rising interest rates push secondary market prices through that boundary.

Second, to manage these dynamics, municipalities and their underwriting teams frequently structure offerings with above-market coupons, which generate higher tax-exempt cash flow, reduce duration sensitivity, and maintain a buffer above par that reduces the risk of triggering adverse market discount treatment in the secondary market.

Consequently, the municipal bond investor experiences a structurally shorter duration profile under a 5.5% coupon bond structure while the spot curve, where coupon matches the benchmark yield at each maturity, serves as a theoretical baseline depicting how duration evolves only as a function of time.

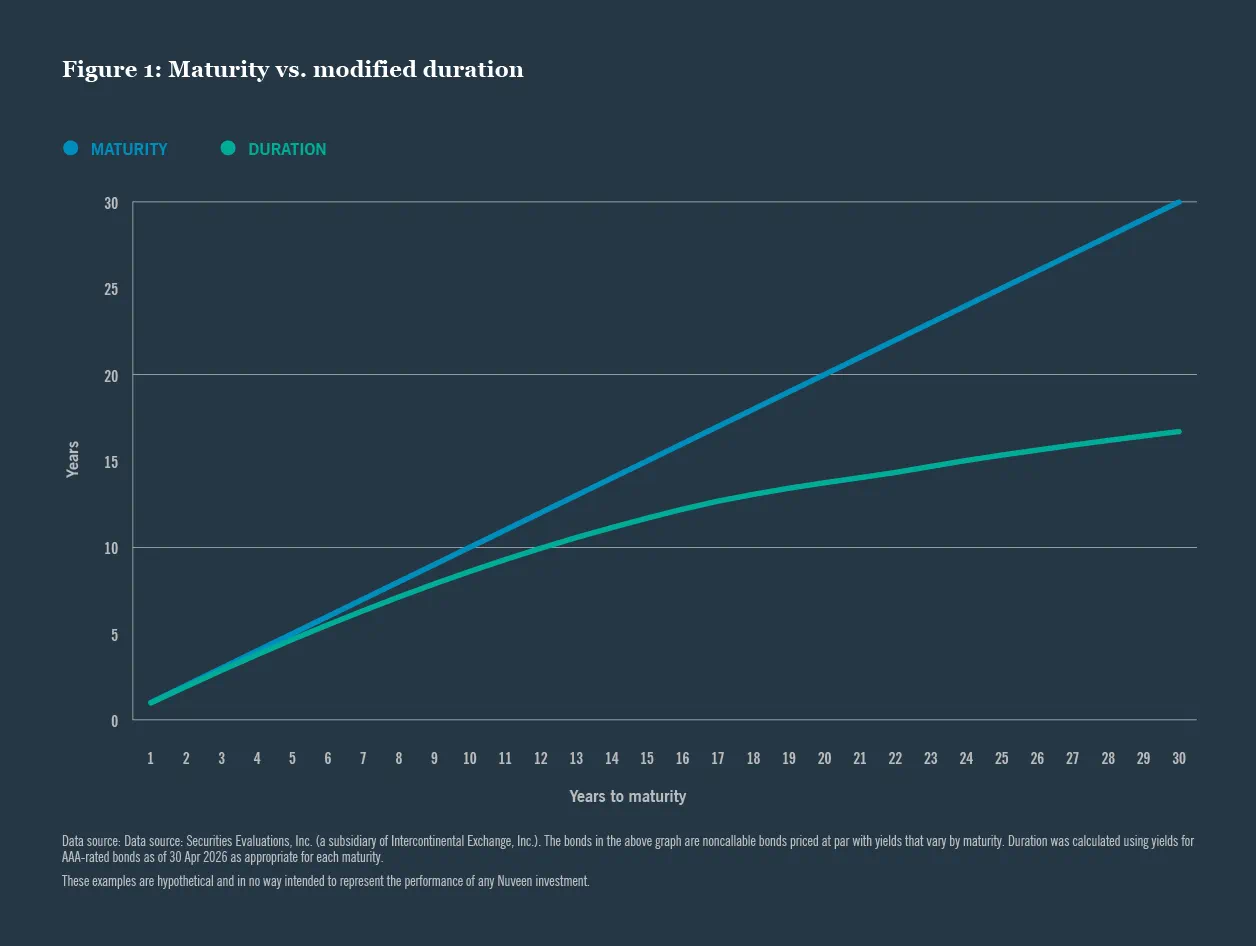

Figure 1 shows the relationship between a bond’s effective maturity (when the bond is expected to be retired) and its modified duration.

Redemption provisions

Call provisions can also cause a bond’s duration to be less than its maturity. Typically duration is calculated based on the date to which the bond is priced. A premium bond, which is redeemable at par sometime before maturity, will be priced to a call date. So the modified duration will correspond to the call date, not the maturity date. Thus, in a market where prices are rising, the volatility of a portfolio will tend to decline as more and more bonds are priced to their call dates rather than to maturity. On the other hand, when prices fall, volatility and average duration tend to increase because of the increase in the number of bonds that are priced to maturity.

This also means that modified durations of callable bonds priced near par may shift rapidly as prices move above and below par – and duration shifts from the call date to the more distant maturity date.

An alternative measure of duration – known as “option-adjusted duration” or “effective duration” – takes into account the effect of the call option on the expected life of a bond. It weighs the probability that the bond will be called based on the spread between its coupon rate and its yield, as well as the volatility of interest rates. Generally speaking, option-adjusted duration (OAD) will be longer than modified duration when a bond is priced to a call date, and shorter than modified duration when a bond is priced to maturity.

Call options limit the potential price appreciation of a bond, but do not limit the downside, when the bond is priced to maturity. As a result, callable bonds typically have negative convexity since the change in price in a rising market is not as great as the change in price in a falling market.

Duration and portfolio management

In any case, since duration reflects bond price volatility, a portfolio’s average duration is more meaningful than its average maturity. By comparing a bond’s duration with an existing portfolio’s average duration, a portfolio manager tries to anticipate the effect that buying or selling that bond would have on the portfolio’s volatility. Further, by exploring how the duration of a bond might change in different market environments, a portfolio manager can better evaluate the relative value of call protection.

Using duration analysis, the portfolio manager may elect, for example, to buy high-coupon, premium bonds to reduce downside risk, or buy deep discount bonds to try to maximize potential price appreciation. Or the manager may decide that intermediate-term, current coupon bonds offer the best value. Whatever the approach, duration analysis helps the portfolio manager evaluate the effects of various trading strategies in an effort to better achieve the goal of minimizing price volatility while maximizing total return.

Related articles

Contact us

You are on the site for: Financial Professionals and Individual Investors. You can switch to the site for: Institutional Investors or Global Investors

1 The present value of a sum yet to be received is the amount of money required today to have the desired amount at a specified future date after compounding interest earnings at an assumed rate.

EndnotesThis material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her financial professionals.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Performance data shown represents past performance and does not predict or guarantee future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. For term definitions and index descriptions, please access the glossary on nuveen.com. Please note, it is not possible to invest directly in an index.

Important information on riskInvesting involves risk; principal loss is possible. Investing in municipal bonds involves risks such as interest rate risk, credit risk and market risk. The value of the portfolio will fluctuate based on the value of the underlying securities. There are special risks associated with investments in high yield bonds, hedging activities and the potential use of leverage. Portfolios that include lower rated municipal bonds, commonly referred to as “high yield” or “junk” bonds, which are considered to be speculative, the credit and investment risk is heightened for the portfolio. Bond insurance guarantees only the payment of principal and interest on the bond when due, and not the value of the bonds themselves, which will fluctuate with the bond market and the financial success of the issuer and the insurer. No representation is made as to an insurer’s ability to meet their commitments.

This information should not replace an investor’s consultation with a professional advisor regarding their tax situation. Nuveen Asset Management is not a tax advisor. Investors should contact a tax professional regarding the suitability of tax-exempt investments in their portfolio. If sold prior to maturity, municipal securities are subject to gain/losses based on the level of interest rates, market conditions and the credit quality of the issuer. Income may be subject to the alternative minimum tax (AMT) and/or state and local taxes, based on the state of residence. Income from municipal bonds held by a portfolio could be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service or state tax authorities, or noncompliant conduct of a bond issuer. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

Nuveen, LLC provides investment solutions through its investment specialists.

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen DMAT Cart

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)