Contact us

Contact Nuveen

Thank you for your message. We will contact you shortly.

Municipal credit remains strong, with stable tax revenues and solid reserve positions continuing to support credit quality. While focus on budgetary pressures is important, high yield municipal bonds typically fund essential service projects separate from governmental operations. High yield municipal investors should pay closer attention to issues such as a project’s economics and necessity, as well as factors more typical of real estate or taxable bonds, such as management, marketing, location and competitive positioning.

High yield municipal bonds are primarily project bonds

Debt service payments for projects funded in the high yield municipal bond space do not come from general revenues collected by a municipality, for the most part. High yield municipal bonds are primarily project bonds that provide an element of essential service that is financially independent from the city, county or state they serve. These revenue bonds offer higher yields to compensate investors for the risk and uncertainty associated with a specific project, such as construction risk, location, management and governance risk, similar to corporate bonds or real estate projects.

That means the high yield municipal bond market is generally not concerned with issues typically associated with general obligation bonds (GOs) — managing public services, balancing budgets and funding pension costs. Rather, high yield investors pay close attention to a project’s economics and competitive position, as well as security features such as:

- A revenue pledge, which provides a security interest in the revenues generated by the project.

- A limited tax revenue pledge, where only those tax revenues pledged to debt service support the bonds.

- Any debt service or project-based covenants which, if violated, could accelerate rights of the bondholders.

- A first mortgage lien on property or other assets.

- Other forms of security interest in the real estate or project.

These features, along with higher yields, help compensate investors for the added risk.

These forms of security are not provided for high-quality GO bonds, as the revenue pledge backing GOs allows for unlimited taxing authority to cover debt service. Substantial credit monitoring is still required, but such credit strengths put high quality GOs and associated revenue bonds solidly in the investment grade rated category. Since high yield municipal bonds often have security features such as liens on land, tax liens on the project and/or security interest in the revenue stream, more potential remedies exist in the event of distress or default. These remedies potentially provide more protection than those found in similarly rated corporate high yield bonds, which are often subordinated in the capital structure of a high yield issuer.

High yield municipals cross many sectors

High yield municipal credit sectors can be characterized in numerous ways. Some credit factors cut across sectors, such as whether a bondholder is secured by a first mortgage lien on the land or an annual appropriation pledge (a taxing entity’s promise to appropriate funds). However, the major credit sectors can be broken down into several profiles:

Tax backed. A tax associated with land or infrastructure development generates revenues for repayment. Subtypes include special assessment districts, community development districts, redevelopment districts, infrastructure development and public improvement districts. Some projects in this sector are referred to as “mud” districts or “dirt” deals, indicating various stages of above-ground development.

Headline risk can affect liquidity and may be triggered by events that have nothing to do with actual credit factors.

Many of these projects also include a lien on the above-ground project. These credits can range from very risky projects with limited initial development to fully developed projects with diversified sources of tax payments from an array of landowners and residents who have subsequently moved into the district.

Health care. These projects range from hospitals or hospital systems to nursing homes and congregate care facilities. These credits are typically rated anywhere from AA+ to B- and below. Although size is not the determining factor, some larger, diversified health care projects fall into the mid-investment grade space, while smaller, less financially flexible stand-alone facilities tend to be higher yielding and lower-rated credits. Health care is being impacted by many factors, including an aging population, increasing expenditures from much higher wages, and the federal regulatory environment. As a result, these bonds require intense and ongoing credit analysis. Many health care credits can be evaluated like corporate credits, with balance sheets, income statements, endowments, real estate and other assets.

Education and charter schools. Similar to health care, credits in the education sector span the ratings spectrum from AAA-rated Harvard University to high yield credits such as small, private colleges or charter schools. Evaluating these credits requires knowledge of enrollment trends and intense focus on operating and balance sheet metrics (debt service coverage, operating leverage and liquidity cushion). Bondholder security is another key part of the analysis, with attention to legal protections, such as a mortgage or revenue pledge, and financial covenants.

Transportation and toll roads. These revenue bonds are repaid by tolls or facility rental fees from a public transportation system (e.g., toll roads, airport gates). Debt service repayment depends on facility usage and project management.

Tobacco. Tobacco settlement bonds are repaid by sales tax generated from the Master Settlement Agreement between various states and participating tobacco manufacturers. The payments by the tobacco companies to the states are determined by a multi-variable formula heavily based on cigarette consumption. Therefore, one risk is that domestic sales of cigarettes may decline further than declines assumed in the various bond documents. Some of these bonds carry investment grade ratings, but the market generally trades these as high yield bonds.

Industrial development and pollution control. Many of these projects depend on repayment from large industrial firms, with the bond proceeds meeting the public purpose to create jobs and/or reduce pollution. This sector is very similar in credit profile to the taxable high yield space, and sometimes a company will have bonds issued in both marketplaces.

Other sectors. High yield municipal bonds can also include financings for convention centers, Native American Tribal gaming facilities, utilities (including water and sewer facilities), multifamily housing and other smaller credit sectors.

Liquidity remains a risk

Liquidity is a risk in the high yield municipal marketplace. Headline risk can affect liquidity and may be triggered by events that have nothing to do with actual credit factors. For example, high yield municipal prices fell dramatically in 2008 even though the vast majority of high yield municipal bonds continued to pay interest and principal when due. During the coronavirus pandemic in 2020, limited defaults in the high yield market mainly affected nursing homes and congregate care centers. However, even these defaults were spread out over time and space and contained mostly to this single sector. In spring 2025, President Trump’s tariff announcement caused most markets to sell off, including high yield munis, which have little to do with tariff issues.

Because these credit issues can be misunderstood and the bonds are often thinly traded, headlines and other factors can impact liquidity – an inherent risk in the high yield municipal bond market.

Portfolios were eventually compensated for patience

In times of elevated market volatility or negative press, investors may decide to sell and wait for conditions or valuations to improve before reallocating funds. But most cannot time the market perfectly, which can mean lost opportunity.

There have been six periods where municipal yields increased by at least 100 basis points in less than one year. We examined the total return of a hypothetical investment of $100,000 held for 6- and 12-month periods following each spike, assuming the investor had the misfortune of investing right before prices declined. In holding periods of 12 months or longer, staying the course benefited investors.

Misunderstanding may create value

Municipal credit has continued to prove resilient during periods of market disruptions, with the most recent example being the coronavirus pandemic. Municipalities have not only recovered from this crisis, but metrics are even stronger.

Media attention on high profile credit situations leaves many investors concerned about the overall state of municipal GO credit quality. However, in this cycle, high quality municipal bonds are well prepared for a fiscal slowdown. Reserves stand at all-time highs, and tax receipts remain robust despite some declines. Therefore, the media is less focused on high quality municipal credit than in the past.

High yield municipals may benefit from these positive perceptions, even though GO bonds are not typically owned in high yield bond funds. Investors may read about financial problems in cities and hesitate to invest in high yield munis, even though high yield credit exposure is not related to municipal budgets.

This misunderstanding may create investment opportunities. The current ratio of high yield municipal yields to high yield corporate yields is 85%, slightly more than the historical average. In addition, inflation has declined faster than bond yields, creating a higher real yield (adjusted for inflation) than in previous time periods.

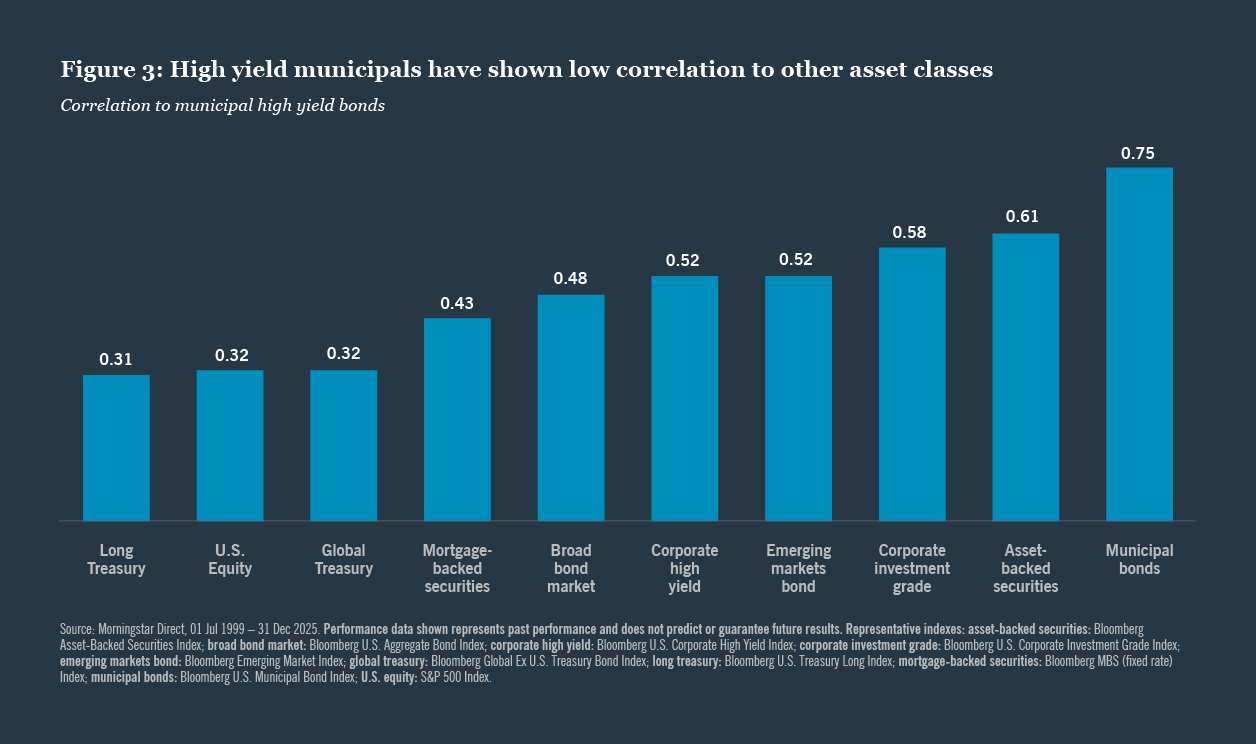

Furthermore, high yield municipals have a low historical correlation to other asset classes, making them an appropriate complement to an overall portfolio. The correlation to equities, Treasuries and corporate high yield is generally near or below 50%.

Fundamental research identifies opportunities

Evaluating high yield municipal bonds typically requires understanding issues relating to land or infrastructure development, potential impact on balance sheets and income statements and issues specific to healthcare policy and education. We believe that in-depth fundamental research can help an investor understand risks, identify opportunities and capitalize on the inefficiencies in this misunderstood asset class.

Related articles

Contact us

You are on the site for: Financial Professionals and Individual Investors. You can switch to the site for: Institutional Investors or Global Investors

Endnotes

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Performance data shown represents past performance and does not predict or guarantee future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. For term definitions and index descriptions, please access the glossary on nuveen.com. Please note, it is not possible to invest directly in an index.

Important information on risk

Investing involves risk; principal loss is possible. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Investing in municipal bonds involves risks such as interest rate risk, credit risk and market risk. The value of the portfolio will fluctuate based on the value of the underlying securities. There are special risks associated with investments in high yield bonds, hedging activities and the potential use of leverage. Portfolios that include lower rated municipal bonds, commonly referred to as “high yield” or “junk” bonds, which are considered to be speculative, the credit and investment risk is heightened for the portfolio. Bond insurance guarantees only the payment of principal and interest on the bond when due, and not the value of the bonds themselves, which will fluctuate with the bond market and the financial success of the issuer and the insurer. No representation is made as to an insurer’s ability to meet their commitments.

This information should not replace an investor’s consultation with a financial professional regarding their tax situation. Nuveen Asset Management is not a tax advisor. Investors should contact a tax advisor regarding the appropriateness of tax-exempt investments in their portfolio. If sold prior to maturity, municipal securities are subject to gain/losses based on the level of interest rates, market conditions and the credit quality of the issuer. Income may be subject to the alternative minimum tax (AMT) and/or state and local taxes, based on the state of residence. Income from municipal bonds held by a portfolio could be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service or state tax authorities, or noncompliant conduct of a bond issuer. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Nuveen, LLC provides investment solutions through its investment specialists.

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen DMAT Cart

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)