Contact us

Contact Nuveen

Thank you for your message. We will contact you shortly.

Section 4: Five themes for 2025

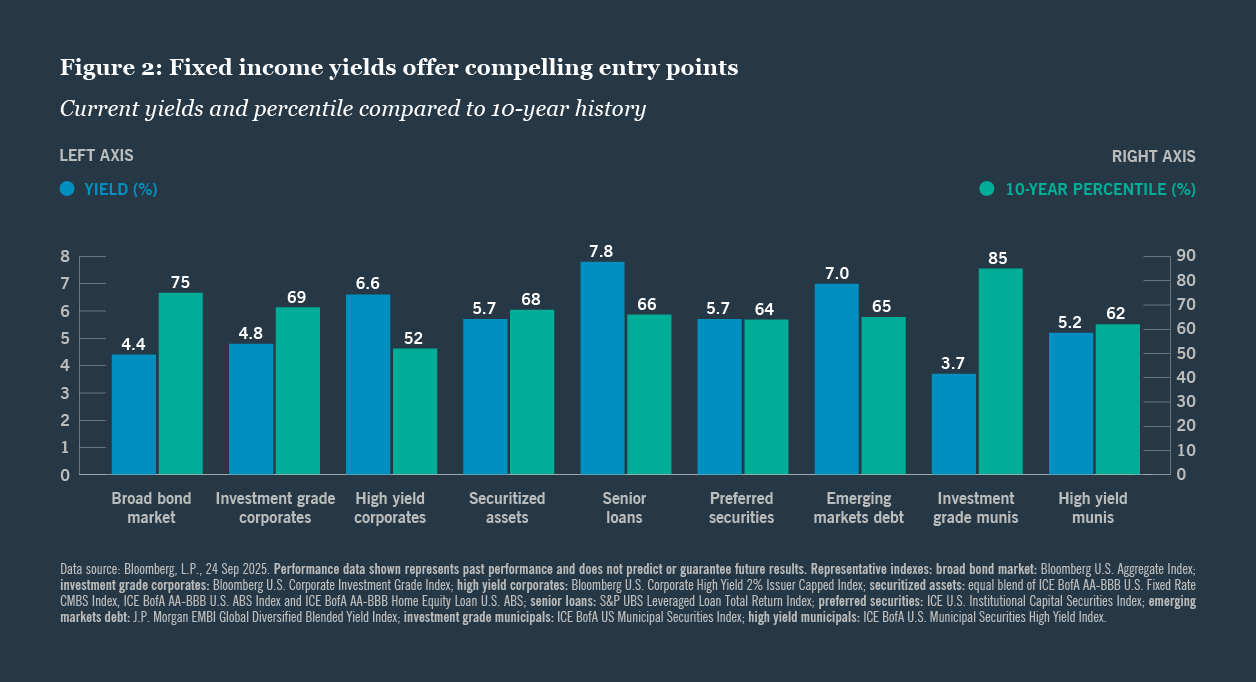

- Relative yields and credit selection, more than risk-free rates, should drive returns in public and private debt markets.

As we explained in the previous section, we expect the Fed and other central banks to continue cutting rates modestly. But that won’t necessarily translate into broad market bond yields moving lower given upward pressure from other sources. This dynamic should produce a steeper U.S. yield curve over the coming quarters, yet we don’t think investors should extend duration to seek returns.

Rather, we think it makes sense to emphasize credit selection and broad fixed income diversification, with a particular emphasis on market segments that continue to offer yields at extremely attractive entry points, on both an absolute basis and relative to their history (Figure 2).

We offer more details on specific areas of the fixed income market we favor in the following section, but several areas merit highlighting. Emerging markets debt has grown increasingly attractive, and we continue to favor securitized assets and senior loans. While some investors have expressed concern about how weakening growth could negatively impact private credit, we believe deal activity remains robust and continue to favor conservative structures with lower leverage and stronger covenants — especially in the middle market segment.

- Municipals are still

the borrower of

choice for investors

in it for the duration.

There is much to like about municipal bonds right now. Fundamentals remain solid for state and local governments: Tax revenues have been climbing, cash balances are high and defaults remain quite low. Municipal bond yields are also elevated, thanks in part to growing new supply. That surge in supply has caused municipal bond returns to lag the broader fixed income market this year, creating what we view as excellent value opportunities.

With the municipal bond curve steeper than the Treasury curve, this looks to be an area of the market where investors may be well compensated for accepting some duration risk. From a credit perspective, we see compelling opportunities across both high grade and high yield municipals.

- Real estate reality:

the trends are

positive.

Real estate markets appear to be in the early stages of a positive turnaround. Returns have been positive for the last few quarters following a two-year downturn driven by falling values, oversupply and weak demand. We believe the first two headwinds have been largely mitigated, and we are seeing meaningful progress on the third.

Real estate values appear to have found a floor and bottomed out. The oversupply issue that emerged at the end of the pandemic is finally fading as construction starts decline. While demand uncertainty for real estate broadly does remain a concern, we are witnessing robust demand in specific sectors such as medical office, grocery-anchored retail and affordable housing.

- The world may

be decoupling;

markets are not..

While some of the tariff turmoil from earlier in the year has subsided, ongoing trade policy uncertainty and geopolitical tensions suggest that globalization may be a distant memory. But from an economic perspective, growth and monetary policy trends are generally still moving in the same direction globally.

We continue to hear discussion around a “sell the U.S.” trade, sparked by a sense that U.S. global economic leadership may be waning. However, we think this trend may be misguided. We maintain our positive stance on U.S. large cap equities, as we believe fundamentals remain strong and that the U.S. will remain the primary beneficiary of the AI boom.

Regarding other areas of the global equity market, we remain broadly neutral toward non-U.S. developed markets, though we view European equities as potentially representing a long-term value opportunity. In contrast, emerging markets equities appear less attractive given heightened global trade policy risks.

- Energy demand

charges ahead of

capacity, creating

opportunities

amid political

changes.

The demand for energy continues to surge. Many of the world’s largest technology companies are investing billions in new data centers, AI infrastructure and power generation. While tech companies themselves should benefit from this trend, we also see significant opportunities in power-related infrastructure investments across public and private markets.

U.S. political and regulatory shifts do affect the relative attractiveness of energy-generating investments. On balance, we expect the global green energy transition to continue, particularly in Europe, but investments in natural gas, pipelines and traditional energy should benefit from Trump administration policies. With power demand outstripping existing supply capacity from conventional sources, we could also see increased investment in nuclear and geothermal energy generation. In contrast, we expect areas such as U.S. wind power and electric vehicle charging infrastructure to face greater headwinds.

Continue reading

If neither purely traditional fixed income and cash at one extreme nor overly equity-centric approaches at the other are optimal portfolio strategies, where do we see the most compelling opportunities? Our latest outlook covers this and more.

Global Investment Committee

Contact us

You are on the site for: Financial Professionals and Individual Investors. You can switch to the site for: Institutional Investors or Global Investors

Endnotes

Sources

All market and economic data from Bloomberg, FactSet and Morningstar.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her financial professionals.The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Performance data shown represents past performance and does not predict or guarantee future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. For term definitions and index descriptions, please access the glossary on nuveen.com. Please note, it is not possible to invest directly in an index.Important information on risk

All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investing involves risk. Investments are also subject to political, currency and regulatory risks. These risks may be magnified in emerging markets. Diversification is a technique to help reduce risk. There is no guarantee that diversification will protect against a loss of income. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Investing in municipal bonds involves risks such as interest rate risk, credit risk and market risk, including the possible loss of principal. The value of the portfolio will fluctuate based on the value of the underlying securities. There are special risks associated with investments in high yield bonds, hedging activities and the potential use of leverage. Portfolios that include lower rated municipal bonds, commonly referred to as “high yield” or “junk” bonds, which are considered to be speculative, the credit and investment risk is heightened for the portfolio. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC/CC/C and D are below-investment grade ratings. As an asset class, real assets are less developed, more illiquid, and less transparent compared to traditional asset classes. Investments will be subject to risks generally associated with the ownership of real estate-related assets and foreign investing, including changes in economic conditions, currency values, environmental risks, the cost of and ability to obtain insurance, and risks related to leasing of properties. Investors should be aware that alternative investments including private equity and private debt are speculative, subject to substantial risks including the risks associated with limited liquidity, the use of leverage, short sales and concentrated investments and may involve complex tax structures and investment strategies. Alternative investments may be illiquid, there may be no liquid secondary market or ready purchasers for such securities, they may not be required to provide periodic pricing or valuation information to investors, there may be delays in distributing tax information to investors, they are not subject to the same regulatory requirements as other types of pooled investment vehicles, and they may be subject to high fees and expenses, which will reduce profits. Alternative investments are not appropriate for all investors and should not constitute an entire investment program. Investors may lose all or substantially all of the capital invested. The historical returns achieved by alternative asset vehicles is not a prediction of future performance or a guarantee of future results, and there can be no assurance that comparable returns will be achieved by any strategy

Nuveen, LLC provides investment advisory services through its investment specialists.

This information does not constitute investment research as defined under MiFID.

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen DMAT Cart

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)