Contact us

Contact Nuveen

Thank you for your message. We will contact you shortly.

Municipal bonds have long played an essential role in addressing America's housing affordability crisis. As housing costs strain household budgets nationwide, municipal housing bonds offer investors attractive tax-exempt yields while providing communities the low-cost capital needed to expand affordable housing across all income levels.

By the numbers

- 33%: U.S. households' spending on housing (affordability benchmark is 30%)¹

- 198%: Housing bond issuance growth from 2016 to 2025²

- 5.53%: Housing index return in 2025 versus the muni index at 4.41%³

- 7%: Housing bonds' share of the $4.4T municipal market⁴

Municipal bonds connect investors to affordable housing

Affordability has become a defining issue across the United States, shaping political discourse and driving election outcomes. Recently, Mayor Mamdani won the New York City mayoral election on a platform of rent freezes, free childcare and fare-free buses.

At the federal level, President Trump recently signed an executive order banning large institutional investors from buying single-family homes. These proposals reflect growing recognition that living costs have become unsustainable for many households.

Municipal bonds directly support affordable housing development while offering investors an opportunity for tax-exempt income. The S&P Municipal Bond Housing Index outperformed the broader market in 2025, returning 5.53% versus 4.41%.

Tax-exempt status allows governmental entities and private developers to access capital at lower costs than conventional financing, creating savings that may be passed to renters and homebuyers. Housing projects generate returns over decades, matching well with municipal bonds' long maturities and creating predictability for developers while ensuring lasting affordability.

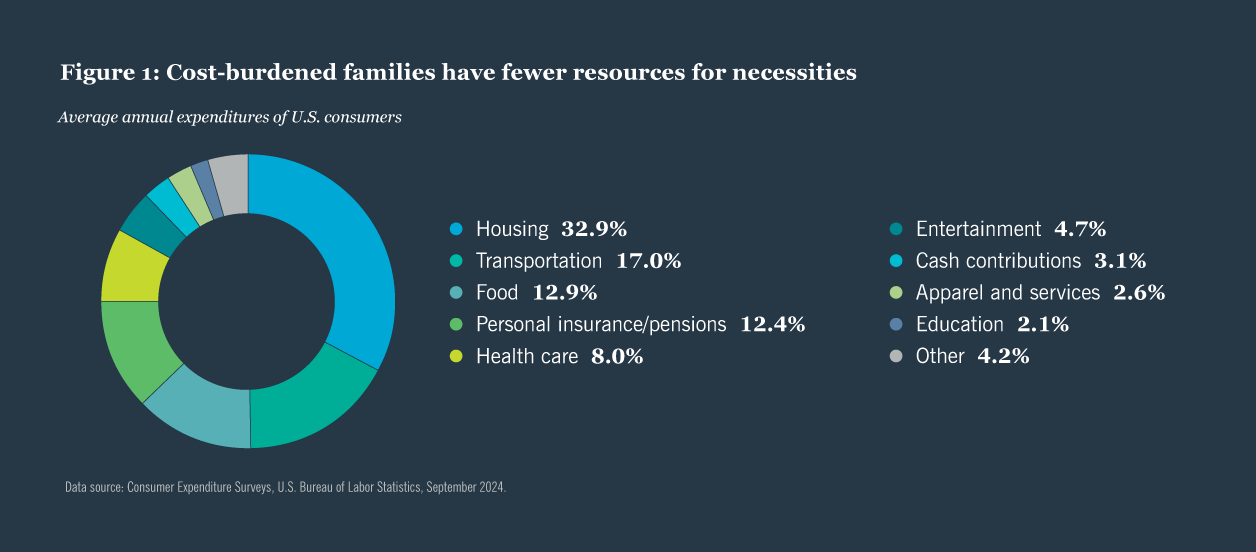

Housing consumes one-third of household budgets

Expensive housing can crowd out resources for other household necessities. The average American household spends nearly 33% of total expenditures on housing - above the traditional 30% affordability threshold - according to the Bureau of Labor Statistics (Figure 1). Beyond this benchmark, families face difficult trade-offs with essentials like food, childcare and education.

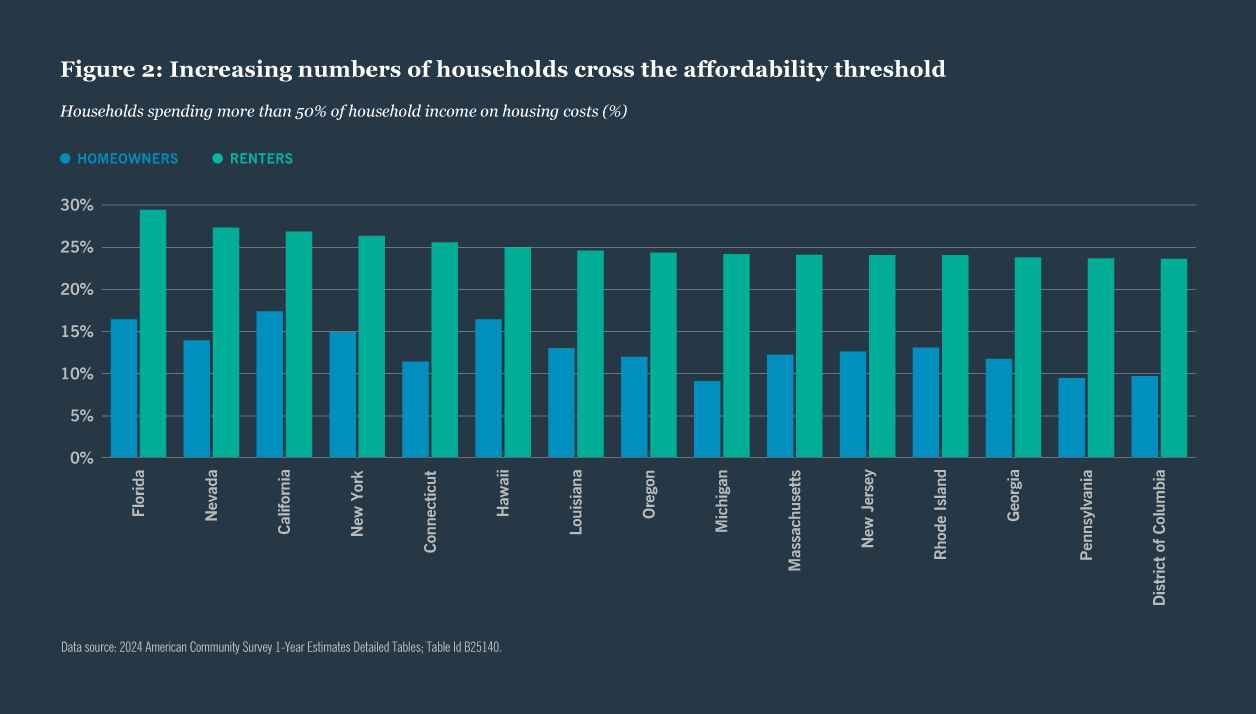

As housing costs have escalated, increasing numbers of American households have crossed this threshold. For example, more than a quarter of renters in states such as California, New York, Florida and Nevada spend over half their income on housing costs (Figure 2).

Governments address housing affordability

- Zoning reform increases housing supply by allowing higher-density development, mixed-use projects and greater building flexibility, unlocking land for new construction.

- Streamlining building approvals reduces the lengthy permitting process, helping developers move faster while lowering costs.

- Mandatory inclusionary requirements mandate that market-rate developments include affordable units, a long-used strategy to increase supply.

- Rent control protects existing tenants but may reduce new construction incentives, potentially constraining supply and reducing housing quality.

- State grant programs provide direct financial support through federal programs administered by states, including community development block grants and low-income housing tax credits.

- Housing trust funds support affordable housing development at all government levels, funded by property taxes, development fees or bonds.

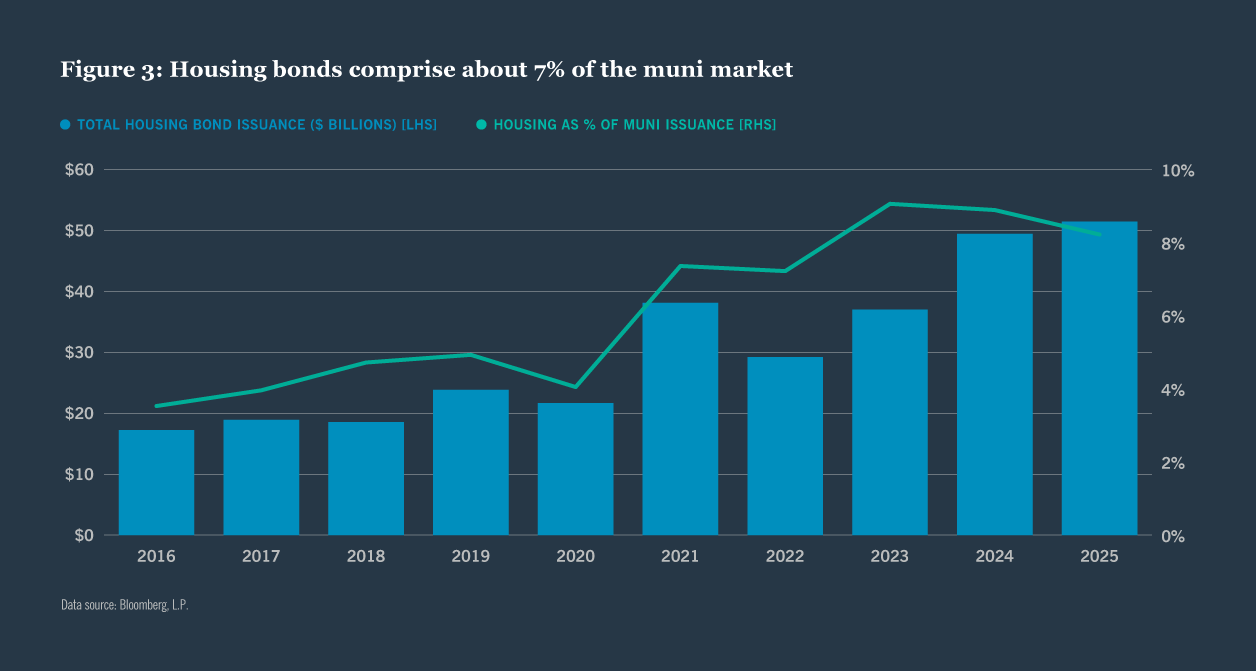

Housing bond issuance has risen over past decade

Housing bonds comprise about 7% of the $4.4 trillion municipal bond market and currently yield an average of 3.58% for bonds with 10-year maturities, versus the broader market at 3.06% (Figure 3). Nearly a quarter of all outstanding municipal housing bonds finance projects in California or New York - two states with high housing costs. Annual housing bond issuance has increased steadily over the past decade, up 198% between 2016 and 2025.

According to National Council of State Housing Agencies (NCSHA), state housing finance agencies alone have helped finance construction of millions of affordable rental homes and supported hundreds of thousands of first-time homebuyers through bond-financed programs.

Housing in the municipal market is financed primarily through single-family, multi-family and workforce housing bonds, though some municipalities also issue general obligation (GO) bonds.

Municipal housing bonds serve diverse income levels and needs

Single-family housing bonds, often structured as mortgage revenue bonds issued by state housing finance agencies (HFAs), help lower-income, first-time buyers purchase homes through below-market interest rate mortgages and down payment assistance. By reducing monthly payments, these bonds make homeownership accessible while helping families build wealth through home equity.

When evaluating single-family housing bonds, we seek issuances backed by federal guarantees and strong collateral structures supporting high credit ratings and stable cash flows. Yields tend to run higher than credit quality alone suggests, reflecting inherent prepayment risk from various factors such as mortgage refinancings and home sales. Term bonds recently priced around 70 basis points above the AAA municipal yield curve.

In early 2026, the Illinois Housing Development Authority issued $200 million in revenue bonds backed by mortgage-backed securities guaranteed by Ginnie Mae, Fannie Mae and Freddie Mac - entities with explicit or implicit federal guarantees.

This structure supports very high credit ratings (Aaa by Moody's). Similarly, New Mexico Mortgage Finance Authority issued $120 million in revenue bonds rated Aa1, with its portfolio of 100% mortgage-backed securities supporting strong credit quality.

Multi-family housing revenue bonds support affordable rental housing by financing construction and rehabilitation of apartment complexes reserved for low-to-moderate-income households, secured by projected revenue streams from the developments.

Bonds issued by state or local housing finance agencies are typically secured by large pools of mortgage loans and generally carry strong credit ratings. These projects may have supplemental security such as FHA mortgage insurance, GNMA-guaranteed mortgage-backed securities, or credit enhancement from Fannie Mae or Freddie Mac.

Multi-family housing projects can also be financed on a single-asset basis. These deals tend to have lower credit quality due to concentrated credit risk and often price 200 basis points or wider than the AAA municipal yield curve.

We seek to invest in multi-family housing bonds from issuers with solid finances, effective governance and reliable loan performance. Key indicators include healthy asset-to-debt ratios, profitable margins, very low delinquency rates (typically under 1%) and experienced management with robust oversight.

Multi-family housing bonds in action

Two recent issuances demonstrate the scale and structure of quality multi-family housing bonds.

- New York City Housing Development Corporation recently priced a $350 million refinancing for the 50th Avenue Apartments in Queens. Of 619 units, 20% serve households at 50% area median income (AMI) or less, 30% serve moderate-to-middle-income households, and half are market rate. The bonds are rated Aa2/AA+. In 2025, NYCHDC issued $1.8 billion, financing 8,647 affordable units.

- Massachusetts Housing Finance Agency (MassHousing) provides mortgage financing for low-to-moderate-income families statewide. As of June 30, 2025, its $2.97 billion multifamily portfolio supported over 240 developments.

MassHousing recently issued $308 million to finance 8 affordable developments totaling 789 units across 30 buildings, leveraging mixed funding sources including low-income housing tax (LIHTC) credits, subordinate debt and local government funds.

Workforce or essential housing bonds represent a relatively new financing type targeting essential workers - teachers, nurses, firefighters, and others whose incomes may exceed traditional affordable housing thresholds but who still struggle to afford market-rate housing in expensive metropolitan areas. These bonds recognize that affordability challenges extend beyond the lowest-income households to encompass much of the working middle class.

Municipal bonds fund multifamily apartment complexes providing discounted housing to qualified tenants earning 80% to 120% of Area Median Income. These high-yield bonds are generally non-rated, backed by a first lien mortgage on the housing complex, and provide higher yields than single- or multi-family housing bonds given their riskier credit profile.

Two examples are Altana-Glendale and Platinum Triangle Anaheim, both issued by California Statewide Communities Development Authority. Solid demand for affordable multi-family housing in California cities including Anaheim and Glendale supports bond repayment.

General obligation bonds are increasingly being used for affordable housing-related projects and programs. These bonds can fund land acquisition, infrastructure improvements, direct construction subsidies and gap financing for projects requiring public support.

While the total amount of GO bond proceeds dedicated to housing nationwide is difficult to quantify, significant examples demonstrate the scale of commitment. Chicago recently authorized $1.25 billion in new GO borrowing specifically for affordable housing initiatives, backed by the city's full faith and credit.

In California, multiple jurisdictions including San Francisco, Oakland and Berkeley have approved GO bonds for affordable housing through voter referendum, reflecting residents' willingness to tax themselves to address the housing crisis. GO bonds issued for housing purposes currently average a yield of 3.02% for bonds with 10-year maturities.

Municipal bonds and community outcomes

For households across America contending with affordability pressures, municipal bonds demonstrate how strategic infrastructure investment can meaningfully address community challenges. America's housing affordability crisis didn't develop overnight and will not be resolved through any single intervention.

However, municipal bonds represent a proven, scalable tool that leverages the tax code's support for state and local governments to help deliver tangible benefits to households struggling with rising costs. As policymakers debate various approaches to affordability - from zoning reform to rent control - the quiet work of municipal bond financing continues to add housing units, support first-time homebuyers and preserve existing affordable housing stock.

Muni bonds connect with Americans' lived experience

The Nuveen munis in your community series explores the connection between effective muni bond investing and Americans' lived experience. Nuveen's muni credit analyst team - one of the industry's largest and longest tenured - constantly assesses the impact of the trends that influence muni credit quality across all market sectors.

Municipal bonds are a foundational element in Nuveen's proud heritage of investing to support public purpose - and an asset class that touches the everyday lives of all Americans. Munis fund essential infrastructure for state and local government: K-12 schools, colleges and universities; roads and airports; hospitals; water and sewer utilities; housing and more.

Our research identifies what we believe are attractive investment opportunities. It also yields practical insights into what individuals can expect when it comes to the availability, operation and cost of services used daily - things like the price of an airline ticket or a hospital visit, the health of regional transportation options, the quality of local school systems or the dependability of critical utilities.

Related articles

Contact us

You are on the site for: Financial Professionals and Individual Investors. You can switch to the site for: Institutional Investors or Global Investors

For more information, please visit nuveen.com.

Endnotes

1 Consumer Expenditure Surveys, U.S. Bureau of Labor Statistics, September 2024.

2 Bloomberg, L.P.

3 Bloomberg, L.P., S&P Muni Bond Housing Index, S&P Muni Bond Index.

4 Bloomberg, L.P.

Sources

EIA Data Barclays Power Grab - How Rising Bills Are Affecting Muni Utilities

https://www.census.gov/content/dam/Census/library/visualizations/2025/demo/Housing-Costs2024.png

How Building Affordable Housing Became Hottest Game in L.A. WSJ

https://laist.com/news/housing-homelesness/califonia-housing-policy-changes-la

https://cbcny.org/research/rent-and-ride

U.S. Energy Information Administration

https://ww.ia.gov/electricity/sales_revenue_price/pdf/table_5A.pdf

Consumer expenditures in 2023 BLS Reports: U.S. Bureau of Labor Statistics

Housing Affordability Index

Housing Bonds - NCSHA

The Middle Class Is Buckling Under Almost Five Years of Persistent Inflation WSJ

Housing affordability will continue to challenge state and local governments Sector Comment Moody's

Rural America's economic and demographic woes will deepen as US economy softens Sector In-Depth Moody's

Rising power prices, affordability concerns fuel regulatory and credit pressures | Sector In-Depth Moody's

https://www.wsj.com/economy/everyone-is-talking-about-the-affordabiliy-crisis-it-cant-be-solved-c3d37a39mod=author_content_page__pos_

Moody's Webinar: Affordability: Policy Choices and Credit Implications PowerPoint template March 2024

Turning Data Center Revenues into Affordable Homes Urban Institute

https://www.cnn.com/2025/12/16/economy/affordability-wage-growth-inflation

Bloomberg ICE Data Services

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor's objectives and circumstances and in consultation with his or her financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain "forward-looking" information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Performance data shown represents past performance and does not predict or guarantee future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. For term definitions and index descriptions, please access the glossary on nuveen.com. Please note, it is not possible to invest directly in an index.

Important information on risk

Investing involves risk; principal loss is possible. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Investing in municipal bonds involves risks such as interest rate risk, credit risk and market risk. The value of the portfolio will fluctuate based on the value of the underlying securities. There are special risks associated with investments in high yield bonds, hedging activities and the potential use of leverage. Portfolios that include lower rated municipal bonds, commonly referred to as "high yield" or "junk" bonds, which are considered to be speculative, the credit and investment risk is heightened for the portfolio. Bond insurance guarantees only the payment of principal and interest on the bond when due, and not the value of the bonds themselves, which will fluctuate with the bond market and the financial success of the issuer and the insurer. No representation is made as to an insurer's ability to meet their commitments. This information should not replace an investor's consultation with a financial professional regarding their tax situation. Nuveen is not a tax advisor. Investors should contact a tax professional regarding the appropriateness of tax-exempt investments in their portfolio. If sold prior to maturity, municipal securities are subject to gain/losses based on the level of interest rates, market conditions and the credit quality of the issuer. Income may be subject to the alternative minimum tax (AMT) and/or state and local taxes, based on the state of residence. Income from municipal bonds held by a portfolio could be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service or state tax authorities, or noncompliant conduct of a bond issuer. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

Nuveen, LLC provides investment solutions through its investment specialists.

This information does not constitute investment research as defined under MiFID.

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen DMAT Cart

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)