Contact us

Contact Nuveen

Thank you for your message. We will contact you shortly.

Alternative credit

Private equity secondaries: Structural advantages for portfolio construction

The private equity secondaries market has evolved over the past two decades from a niche solution into a bona fide asset class offering benefits for limited partners (LPs), general partners (GPs) and secondary buyers. With transaction volumes growing from $26 billion in 2013 to over $160 billion in 2024, secondaries are a compelling option for consideration within diversified portfolios.1

For financial advisors and their clients seeking private equity exposure with potentially enhanced risk-return characteristics, the secondaries market offers compelling structural advantages that merit consideration.

[Interested in learning more about PE secondaries evolution? Watch the webinar replay now.]

Two distinct pathways to value

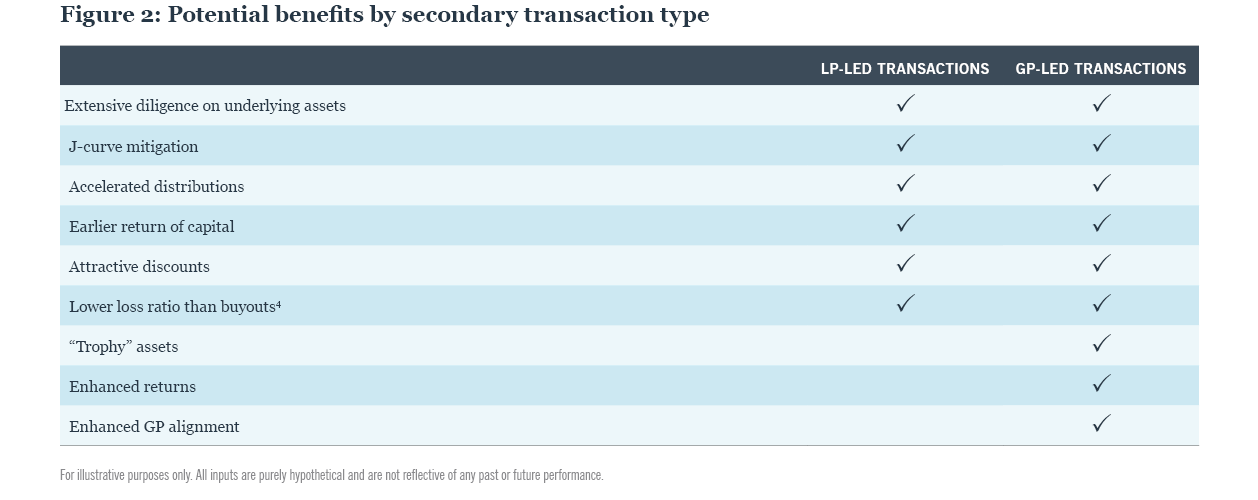

Private equity secondaries refer to the buying and selling of existing private equity fund interests and direct company investments, rather than making new primary investments into companies or funds. The secondaries market operates through two primary transaction types, each offering unique benefits:

LP-led transactions involve investors selling their stakes in private equity funds to generate liquidity or rebalance portfolios. These transactions provide buyers with immediate diversification across multiple portfolio companies within established funds, along with visibility into actual performance rather than historical manager track records.

GP-led transactions, primarily structured as continuation vehicles, allow private equity firms to retain control of their highest-performing assets while providing liquidity options to existing investors. These transactions typically focus on trophy assets where sponsors see significant additional growth potential.

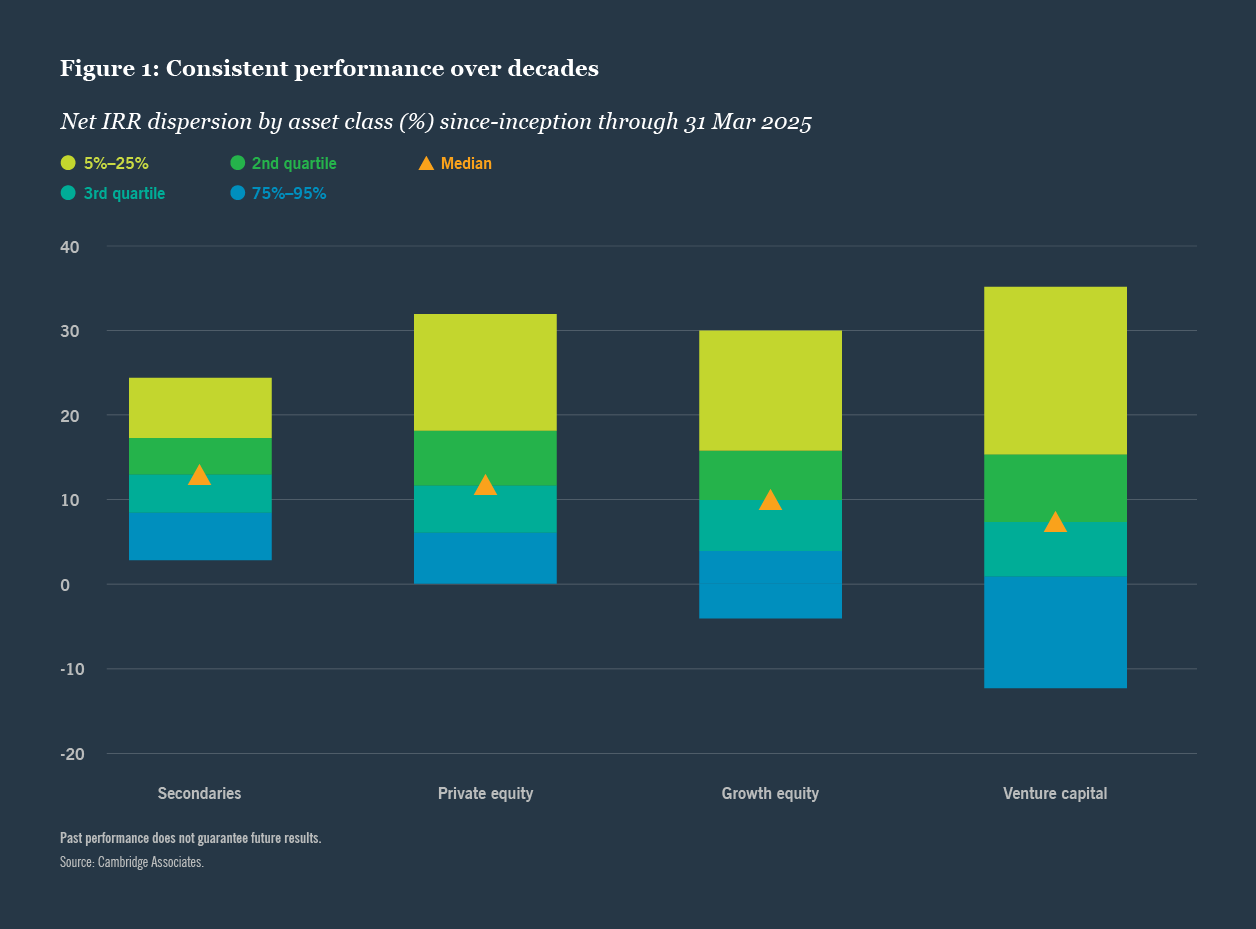

Both transaction types have demonstrated attractive performance characteristics, with secondaries showing the narrowest return dispersion of any major private markets asset class over the past 25 years (see Figure 1). 2

Structural advantages of secondaries

Several factors contribute to the compelling risk-return profile of secondaries investments:

Reduced blind pool risk: Unlike traditional private equity investments where performance is reliant on managers' historical track records remains theoretical, secondaries buyers can evaluate actual company performance, management effectiveness and value creation progress during due diligence.

Attractive entry points: Secondaries transactions are typically structured at discounts to book value (i.e., the cost of generating liquidity for an illiquid asset). They also often benefit from conservative sponsor valuations and timing advantages between pricing dates (generally the most recently available quarterly mark) and deal closure. This "record date lag" can create even more material effective discounts as portfolio companies continue growing during the transaction process.

Enhanced alignment: In GP-led transactions, sponsors typically invest significant capital alongside secondaries buyers, often representing 5-25% ownership compared to the typical 2-5% in traditional funds.2

Accelerated distributions: Secondaries funds generally deploy capital faster and distribute proceeds sooner than traditional private equity funds, reducing cash drag and improving overall returns.3

Diversification:The asset class offers significant diversification benefits through LP-led transactions that provide immediate exposure to mature fund positions and can fill gaps in vintage year exposure, while GP-led transactions offer access to curated portfolios across diversified fund managers and industries. This contrasts with traditional fund commitments that invest in new portfolio companies over approximately 5-year investment periods to achieve similar diversification.

Why private equity secondaries now

Undercapitalization, combined with the structural evolution of the market, creates what we view as a compelling entry point.

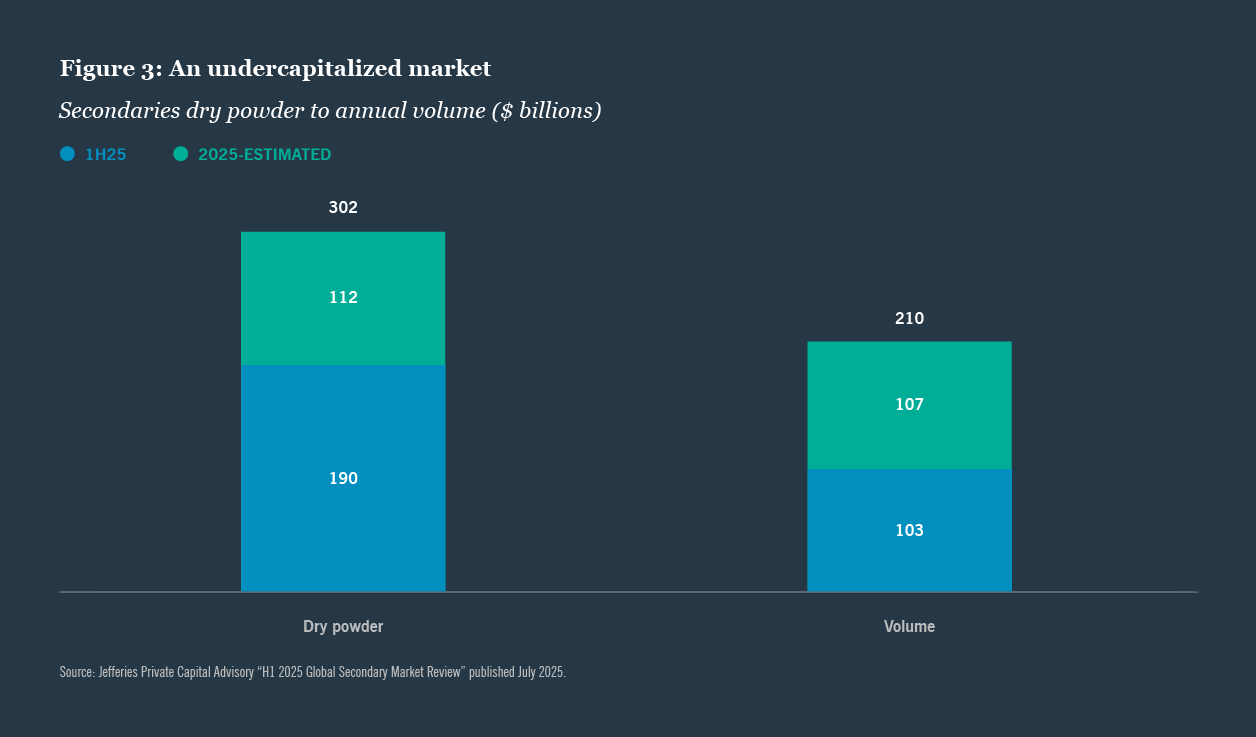

While the market has grown substantially, it remains undercapitalized relative to private markets broadly. Current dry powder sits at approximately 1.5 times annual volume, compared to over 2.0 times for traditional private equity, creating favorable supply-demand dynamics for buyers (see Figure 3). 5

Reduced exit activity is driving strong volume. Deal flow is not expected to slow when M&A markets rebound

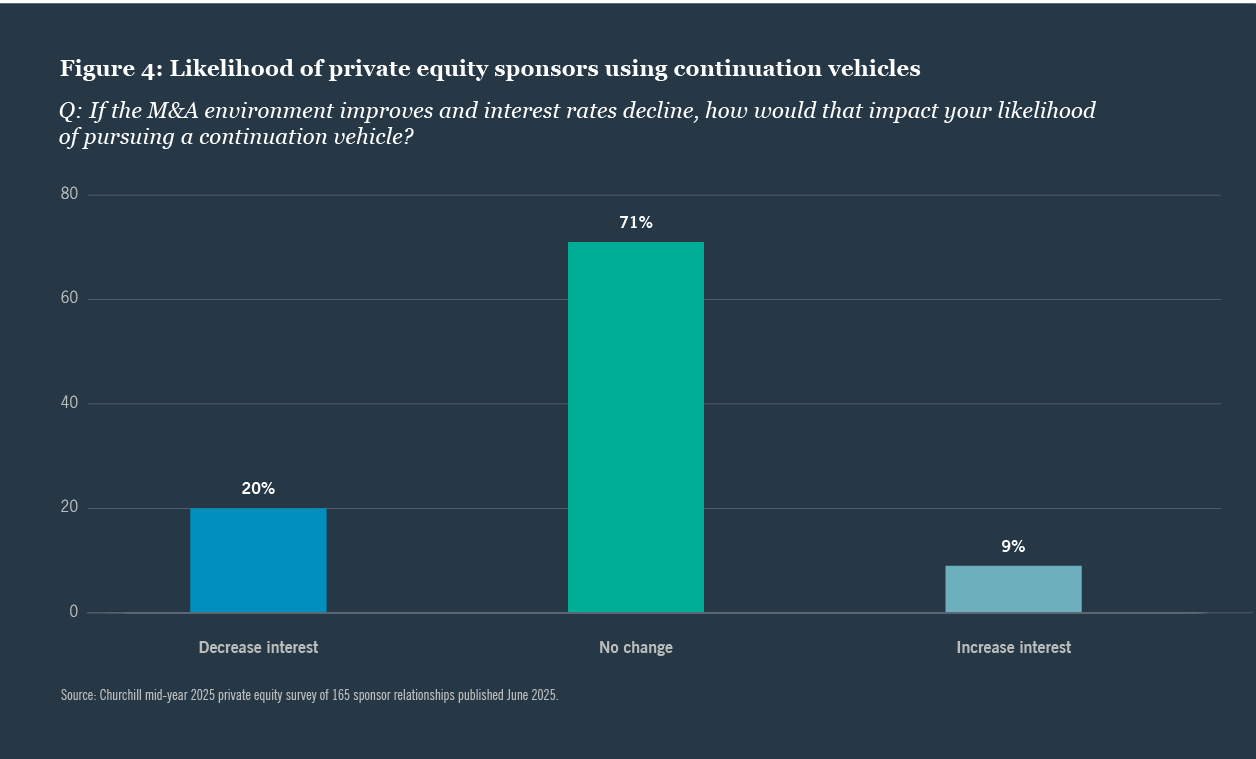

The modern secondaries market has evolved beyond distressed selling. Today, sophisticated portfolio management and strategic asset optimization drive most activity. On the GP-led side of the market, a recent Churchill survey shows that 80% of private equity sponsors plan to maintain or increase their use of continuation vehicles even as market conditions improve (see Figure 4).

Access to high-quality assets during peak growth

While secondaries can accelerate portfolio establishment, the market now offers access to trophy assets that may no longer trade through traditional buyout processes. As sponsors hold their best-performing companies longer, secondaries may be the only way to access these high-quality assets during their peak growth phase.

A strategic allocation consideration

We believe the growth in private markets assets under management (forecasted to exceed $60 trillion by 2032)6 naturally provides an expanding supply of private equity secondaries opportunities, regardless of broader economic conditions. The combination of reduced blind pool risk, attractive entry points, enhanced alignment and accelerated distributions creates what we believe is a compelling case for including secondaries as a strategic component of private markets allocations.

To further help you evaluate if incorporating secondaries is appropriate for clients’ portfolios, explore our research paper Beyond the Basics: How Secondaries Can Enhance Client Investment Outcomes.

Differentiated access to the U.S. middle market

- With over $56 billion in committed capital and as one of the most active U.S. middle market lenders, Churchill provides customized financing solutions to private equity firms and their portfolio companies across the capital structure.5,6 The firm has established relationships with more than 300 private equity firms and has over $20 billion committed to U.S. middle market private equity funds, equity co-investments and secondaries since 2011, with $2 billion or more in new commitments annually.9,10

Related articles

About the author

Contact us

You are on the site for: Financial Professionals and Individual Investors. You can switch to the site for: Institutional Investors or Global Investors

For more information, please visit nuveen.com.

Endnotes

Sources

1Evercore H1 2025 Secondary Market Review published February 2025

2PJT Partners “FY 2024 Secondary Market Update Investor Roadmap” published January 2025

3Morgan Stanley Private Capital Advisory “The Case for Continuations Funds: An Updated Review of Initial Performance” published March 2025. Continuation fund dataset represents 147 continuation funds with vintages between 2018-2024 and does not represent an exhaustive list of every continuation fund completed. Buyout fund DPI benchmarks are calculated using performance data from Preqin’s database comprised of 815 buyout funds with vintages between 2018-2024.

4Morgan Stanley. As of March 2025. Principal loss as referenced herein is defined as funds with <1.0x reported net MOIC

5Jefferies Private Capital Advisory “H1 2025 Global Secondary Market Review” published July 2025.; Schroders “Redefining private equity: How continuation investments are

disrupting the buyout market” published August 2025

6Bain Global Private Equity Report Published June 2025

7As of 30 Jun 2025. The term “committed capital” refers to the capital committed to client accounts in the form of equity capital commitments from investors, as well as

committed, actual or expected financing from leverage providers (including asset-based leveraged facilities, notes sold in the capital markets or any capital otherwise

committed and available to fund investments that comprise assets under management). For purposes of this calculation, both drawn and undrawn equity and financing

commitments are included. In determining committed capital in respect of funds and accounts that utilize internal asset-based leverage (e.g., levered funds and CLO

warehouses), committed capital calculations utilize a leverage factor that assumes full utilization of such asset-based leverage in accordance with the account’s target

leverage ratio as disclosed to investors. In determining committed capital in respect of Churchill’s management of an institutional separate account for its parent company,

TIAA (as defined below), (i) committed capital in respect of private equity fund interests includes commitments made by TIAA to such strategy over the most recent 10 years,

and the net asset value of all such investments aged more than 10 years, and (ii) committed capital in respect of equity co-investments, junior capital investments, structured

capital investments, and senior loans includes the commitment made by TIAA for the most recent year, and the outstanding principal balance of investments made in all

preceding years, and (iii) committed capital in respect of secondaries includes commitments made by TIAA, which includes the aggregate commitment made by TIAA since the

inception of the strategy in 2022 and inclusive of the current year’s allocation. In determining committed capital in respect of Churchill’s management of institutional separate

accounts for third party institutional clients, committed capital includes the aggregate commitments made by such third party clients, so long as such commitments remain

subject to recycling. Thereafter, outstanding principal balance is used in respect of any applicable commitment (or portion thereof) that has expired. Due to the foregoing,

committed capital figures may be adjusted over the course of a financial period, based on accounts transitioning the calculation methodology from capital commitment to

invested capital

8Pitchbook Data’s FY 2024 US PE Middle Market Lending League Tables with select titles

9Includes private equity fund commitments made under the Private Equity fund strategy since 2011. Excludes venture capital and secondaries commitments. TIAA and client

capital commitments to Churchill that are not yet committed to specific underlying funds are excluded

10Average deployment from 2021 - 2024

Important information on risk

Investing involves risk; principal loss is possible. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, derivatives risk, dollar roll transaction risk and income risk. As interest rates rise, bond prices fall. Below investment grade or high yield debt securities are subject to liquidity risk and heightened credit risk. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. Please note investments in private debt, including leveraged loans, middle market loans, and mezzanine debt, are subject to various risk factors, including credit risk, liquidity risk and interest rate risk.

This information represents the opinion of Nuveen, LLC and its investment specialists and is not intended to be a forecast of future events and or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time.

Nuveen, LLC provides investment advisory services through its investment specialists. Churchill Asset Management is a registered investment advisor and an affiliate of Nuveen, LLC. This information does not constitute investment research as defined under MiFID.

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen DMAT Cart

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)