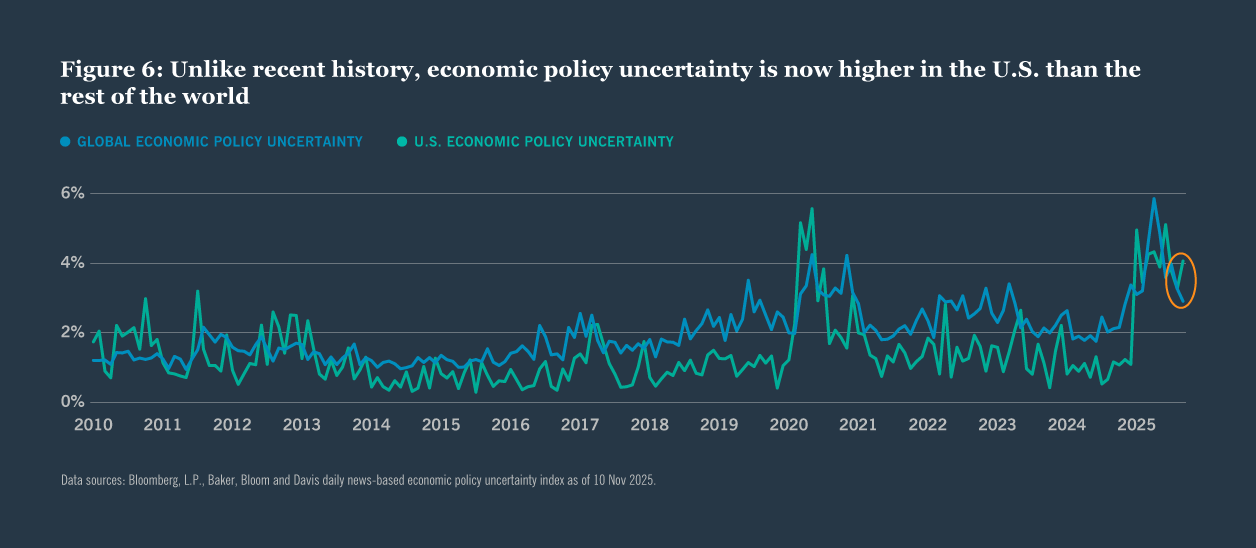

A notable shift in the 2026 landscape will be the narrowing gap between developed markets (DM) and emerging markets (EM) in terms of macro stability, institutional credibility and policy predictability (Figure 6). Questions investors once reserved for emerging markets around political continuity, central bank independence and the durability of fiscal and institutional anchors are becoming increasingly relevant across major developed economies.

Political transitions in France and Japan, alongside the change in U.S. Federal Reserve leadership when Chair Powell’s term ends in early 2026, introduce uncertainty as global term premiums have already risen. Meanwhile, continued supply chain adjustments, elevated geopolitical tensions and an increasingly fragmented trade environment mean that DM economies face structural forces traditionally associated with EM.

At the same time, many EM economies have strengthened their fundamentals. Proactive and more decisive monetary tightening, healthier balance sheets and more credible policy frameworks mean EM assets are entering 2026 from a position of relative stability.

For investors, these factors make the case for taking a more EM-style analytical framework to DM issuers: assessing political and institutional risks as part of the overall credit, rates and currency outlooks. It also supports selective allocations to areas insulated from sovereign-level volatility such as securitized credit and municipals, while recognizing that high-quality EM debt may offer diversification benefits traditionally associated with DM.

Actions to consider

- Analyze political and institutional risks in both DM and EM allocations.

- Favor sovereign-insulated assets like securitized credit and municipals.

Continue reading

Contact us

- +44 20 3727 8000

- 201 Bishopsgate, London, United Kingdom