Our 2026 outlook rests on a fundamentally constructive view of global growth. Our long-held “no recession” call remains intact. Although headwinds persist, fresh areas of strength more than offset areas of concern. Credit spreads are tight by historical standards but fair for the current environment. We suggest maintaining modestly risk-on exposure, specifically in preferred securities, high yield corporates, broadly syndicated loans and middle market loans.

Across developed markets, including in the U.S., Euro area and Japan, we expect faster growth in 2026 than 2025. Global inflation has moderated to around 2.5% year-over-year from over 5% in 2023, and is now within striking distance of the conventional 2% target.

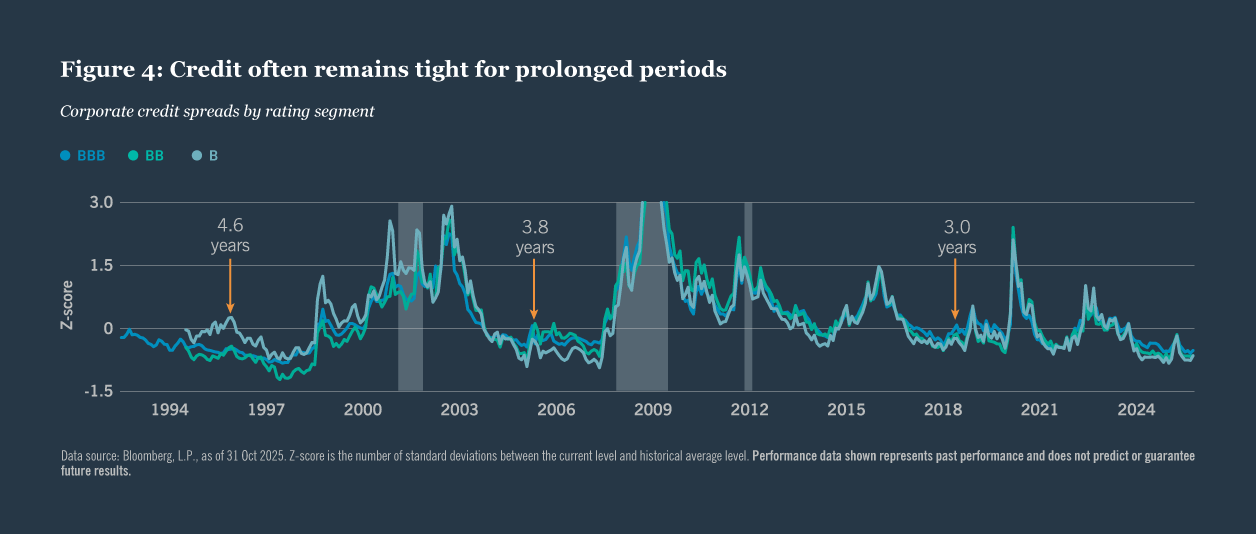

At the same time, tech infrastructure investment has driven roughly 20% of headline U.S. GDP growth in 2025 and should remain elevated, with scope for better productivity growth as AI tools are deployed more widely across the workforce (Figure 3). Strong corporate fundamentals are poised to continue to be supported by healthy balance sheets. Valuations are rich by historical standards, but credit spreads often remain tight for years at a time (Figure 4). We favor taking risk in segments that combine strong fundamentals with reasonable credit spreads. Higher-rated, investment grade segments do not offer compelling income, while lower-rated, below investment grade segments carry too much shock risk. The up-in-quality segment of below-investment grade markets — in preferred securities, high yield corporates, broadly syndicated loans and middle market lending — is the sweet spot.

Actions to consider

- Maintain modest risk-on exposure in preferreds, high yield and loans.

- Focus on higher-quality segments within below investment grade credit.

Continue reading

Contact us

- +44 20 3727 8000

- 201 Bishopsgate, London, United Kingdom