In 2026, fiscal policy, rather than monetary policy, will shape global fixed income markets. While central banks across developed economies near the end of their rate cutting cycles (Figure 1), fiscal trajectories remain far more variable. Elevated deficits, ageing demographics, sustained commitments to defense, industrial policy and energy transition mean fiscal settings will exert an important influence on growth, inflation and term premiums over coming quarters and years.

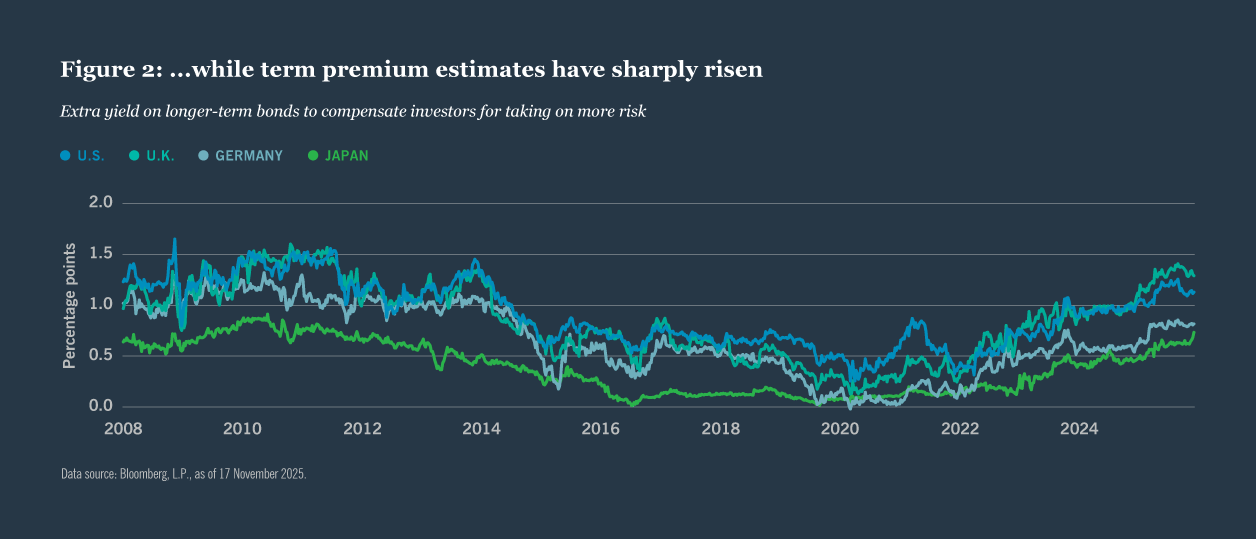

Across the U.S., Euro area and Japan, governments are set to maintain relatively expansionary fiscal positions. With debt levels already elevated, wide deficits threaten to push term premiums higher across most government bond markets (Figure 2). Though central bank policy may be entering a new, more-predictable environment, investors must assess not only the path of policy rates but also the credibility and medium-term sustainability of fiscal plans. One bright spot is the U.K., which we expect to proceed cautiously with both monetary and fiscal adjustments, adding further differentiation within developed markets.

For fixed income investors, fiscal dynamics warrant a prudent approach to positioning across curves and sovereign markets. Rather than extending duration aggressively, we see value in positioning for moderately steeper curves, an environment supportive of sectors with structural demand or lower sensitivity to sovereign supply dynamics. Securitized credit, municipal bonds and high-quality credit remain well supported, while careful attention to sovereign issuance patterns and fiscal frameworks will be increasingly important.

Actions to consider

- Target sectors with structural demand insulated from sovereign supply pressures.

- Favor positioning for a steeper curve over aggressive duration extension.

Continue reading

Contact us

- +44 20 3727 8000

- 201 Bishopsgate, London, United Kingdom