Did you know your holiday shopping helps state and local governments build infrastructure? Many governments issue bonds secured by sales taxes — which are bolstered by seasonal gift purchases — to finance infrastructure investments. While tariff-driven price increases create uncertainty about consumer behavior this year, sales tax bonds feature strong security provisions and reserves that have proven resilient through economic cycles.

By the numbers

- 45: number of states with a sales tax1

- 30%: sales taxes as a percentage of total state tax collections1

- 3.4%: sales tax revenue growth projected in fiscal 20262

- 7.5%: national weighted average sales tax rate1

State and local budgets depend on robust sales tax collections

Sales taxes are a crucial revenue source for state and local governments, funding education, health care, public safety and infrastructure. Forty-five states collect statewide sales taxes, with local sales taxes in 38 states. These taxes generate 30% of state tax revenues and 13% of local collections, making them the second-largest state revenue source after personal income taxes (Figure 1).

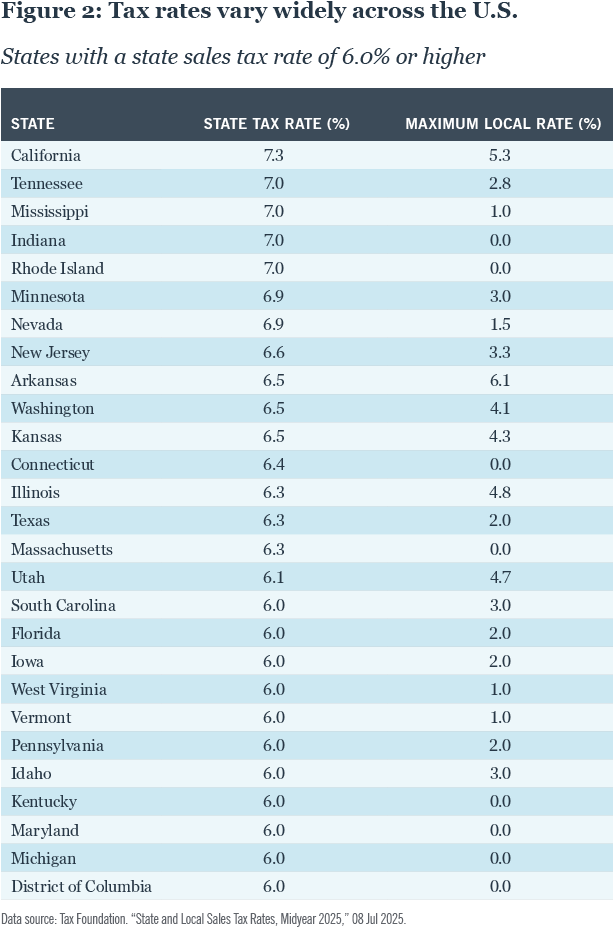

Tax rates across the U.S. vary widely and are frequently adjusted (Figure 2). In addition to statewide sales taxes, many states allow local governments to set their own sales tax rates within certain limits. For example, Illinois has a state sales tax of 6.25%, but most municipalities can levy an additional local sales tax up to 1%, while home-rule municipalities can impose unlimited local sales taxes.

The nationwide weighted average sales tax rate is 7.5%, including both state and local rates. Rate affordability must be evaluated within the context of a government’s overall tax structure and taxes levied by overlapping jurisdictions. The total rate paid often includes multiple local and special district rates layered on top of the state rate

Some states, like Florida and Tennessee, have higher sales tax rates but do not levy statewide income taxes. Other states rely on income taxes and do not levy sales taxes at all. Five states — New Hampshire, Oregon, Montana, Alaska and Delaware — have no state sales tax. California has the highest state tax rate at 7.25%, while Colorado has the lowest at 2.9%.

What’s taxed — and what’s not

While most people understand the basic mechanism of sales tax — a percentage-based tax on goods imposed at the time of sale — many may not realize how widely the taxability of items varies from state to state. Most states have exemptions or lower rates for essential items such as groceries, clothing under a certain dollar threshold, or prescription medications.

Additionally, in most states, sales taxes apply to goods but not services. As the U.S. economy has transitioned from goods-producing to service-based, the sales tax base captures a smaller share of overall economic activity, limiting revenue growth. States are considered to have a broad sales tax base when they allow fewer exemptions and apply the tax to most goods and services. For example, Hawaii, which has one of the broadest sales tax bases, taxes barber services — only one of four states to do so. Conversely, states with numerous exemptions are said to have a narrow tax base.

Generally, having a broader sales tax base is more effective at raising revenue, easier to administer and results in greater revenue stability. For these reasons, numerous think tanks, economists and government officials support broadening the sales tax base to include more services. However, opponents argue that sales taxes are regressive, placing a larger burden on lower income households, and prefer raising revenues through other means.

Online shopping is not exempt from sales taxes. In a landmark 2018 decision (South Dakota v. Wayfair, Inc.), the U.S. Supreme Court ruled that states may require out-of-state sellers to collect sales taxes on internet purchases, even without a physical presence in the state. Since that ruling, all 45 states with statewide sales taxes have adopted remote sales tax laws. Most state laws also address marketplace facilitators such as Amazon, eBay and Etsy, requiring these companies to serve as the primary tax collectors.

Prior to the Wayfair ruling, states and local governments were concerned that missing out on increasing online sales was eroding sales tax revenue. Following the Wayfair decision — and especially during the pandemic when social distancing measures increased online shopping — e-commerce grew at a very high rate, supporting strong growth in total sales tax collections.

Forecasts point to slower sales tax growth

Over the last few years, strong governmental revenue collections have been driven by robust individual income tax growth. Sales taxes increased sharply during the early years of the pandemic due to inflation and increased consumer spending but have grown at a slower pace recently (Figure 3). Total state and local sales tax collections increased 4.6% in 2024 compared to 13.1% growth in 2021.

Slower economic and consumer spending growth will impact sales tax revenue collections. On average, state revenue forecasts project sales taxes to increase 3.4%, compared to personal income taxes forecasted to increase 4.9%. Overall consumption is expected to remain resilient, supported by spending from upper income households.

Spending from middle- and lower-income groups is likely to be more affected by recent federal tax policy changes and benefit cuts, and these groups tend to be more sensitive to tariff-related price increases for consumer staples. Reductions in Medicaid and SNAP benefits could curtail discretionary spending among affected households. Additionally, the impact of tariffs on consumer behavior introduces new uncertainty and makes revenue forecasting challenging.

Evaluating sales tax bonds requires focus on security provisions

Because sales taxes are highly sensitive to economic conditions, bondholders typically require strong security pledges or guardrails to be in place. In periods of sustained economic growth or inflationary environments, sales tax revenues can experience robust growth. However, steep declines are also possible. Unlike consistently stable property taxes, which primarily support local government operations, sales taxes can fluctuate from year to year. For local economies highly dependent on tourism, the volatility inherent in sales taxes may be amplified; however, these risks may be mitigated through stronger security features.

A sales tax revenue bond pledge is in some ways inherently simpler for investors to assess than a general obligation promise to pay. The strength of a narrowly defined revenue stream pledged to bondholders can be quantitatively measured by comparing it to annual debt service. Sales tax bonds typically have strict legal covenants such as minimum debt service coverage ratios and additional bonds tests that protect investors from pledged revenues being over-leveraged.

Strong security features often include a trustee intercept, or a flow of funds that diverts and segregates tax revenues to pay debt service before other operating expenses and dedicated reserve funds. These features can make sales tax bonds attractive investments.

Securitized structures may reduce financing costs

Some municipal issuers, especially when facing fiscal stress, have used securitization structures for sales taxes or other dedicated taxes to access the bond market and generate interest-cost savings. This type of financing vehicle allows a municipality to assign or “sell” certain revenues to an independent entity that issues debt backed by the revenue stream for the benefit of the municipality. The structure allows pledged revenues to be segregated for debt service before excess revenues are made available to the municipality for other purposes.

For example, a state may collect sales taxes on behalf of a city and transfer the receipts directly to a third party, where collections are trapped and accumulate until they are sufficient to pay debt service before any residual funds are remitted to the city.

By securitizing revenues, municipalities aim to shift the focus to debt service coverage and legal protections and away from underlying general creditworthiness. Often the goal is to obtain more affordable market access than could be achieved by issuing bonds secured by the municipality’s general obligation pledge.

One example of this securitization structure involves the City of Chicago’s sales tax. The city created a securitization corporation in 2017, to which it legally transferred ownership of its pledged sales tax revenues.

This structure segregates the pledged sales taxes from other city revenues and funds, effectively insulating bondholders from the operating risks associated with the City of Chicago. Chicago Sales Tax Securitization Corporation bonds are rated A+/AAA/AAA by S&P, Fitch and Kroll, while the City of Chicago’s general obligation bonds are currently rated BBB/A-/A- by the same rating agencies, reflecting the strong security structure of the sales tax bonds.

Las Vegas leverages tourism revenue for Muni bond financing

Las Vegas is a top tourist destination in the U.S., and discretionary spending is the main driver of its tourism industry. Consequently, the City of Las Vegas relies heavily on sales taxes, which account for more than half of the city’s operating revenue. Las Vegas’s “consolidated tax” revenue includes sales tax revenue along with excise taxes on cigarettes and liquor and other sources.

Although sales tax collections can be affected by economic cycles, they have generally performed well over time, growing at a compound annual rate of 3.3% since 2005. There have been two notable declines in recent history: during the Great Recession (2007–2010) when consolidated taxes fell a cumulative 24% and during the pandemic (2020) when they declined 4% year-over year. Revenues have rebounded by over 40% since 2020, and sales tax revenue bonds could withstand a 63% decline before approaching 1.0x coverage.

Las Vegas issues general obligation bonds that are additionally secured by a pledge of a portion of the city’s consolidated tax revenue. The bonds are considered secure investments and are rated Aa2 by Moody’s and AA+ by S&P. In recent years, the city has issued such bonds for various purposes, including improvements to the city’s civic center, municipal courthouse building and performing arts center.

Diverse projects tap into sales tax bond financing

Sales tax bonds have been issued to fund a wide variety of infrastructure needs. Projects supported by these revenues have ranged from small community based recreational parks, schools and public libraries to larger regional public transit systems, bridges and highways and professional sports stadiums. Sometimes, state laws dedicate sales taxes to specific purposes, while other states may allow a wide variety of uses.

For instance, Iowa state law allows all school districts to use a statewide 1% sales and use tax to support infrastructure projects and provide property tax relief to residents. The state collects the tax revenue and distributes it to districts on a per-pupil basis. Importantly, a district experiencing enrollment declines could still see an increase in their per pupil sales tax revenue if sales tax collections grow statewide. In Arizona, many municipalities issue dedicated tax bonds secured by sales or excise taxes to fund essential capital projects, water and sewer infrastructure, or to prefund pension liabilities.

Mall of America powers infrastructure financing

The Mall of America, the largest mall in the U.S., is located in Bloomington, Minnesota, just south of the Twin Cities. The Mall of America is a significant driver of sales tax revenues, attracting over 40 million visitors annually who dine and shop throughout Bloomington. In 2023, city residents approved a 0.5% sales tax to support infrastructure needs.

The city currently has $100 million in outstanding sales tax bonds issued to fund construction of a community health and wellness center and restoration work on the city’s 100-acre nature park. The new sales tax generated $15 million in revenues in its first year, providing 1.9x coverage of maximum annual debt service (MADS) on the bonds.

Dependency on tourism can make sales tax collections extremely sensitive to economic slowdowns. For example, during the height of the pandemic, taxable sales in Bloomington fell a sharp 36% year-over-year. Current sales tax revenues could withstand a similar decline and still maintain over 1.0x MADS coverage on the bonds.

Strong security covenants are in place, including a debt service reserve fund, which prevents payment disruptions should sales tax collections decline precipitously below annual debt service requirements. Reflecting the city’s robust credit quality, S&P rates Bloomington’s general obligation bonds AAA/Stable and its sales tax bonds AA/Stable. The rating differential reflects the volatility of sales tax revenues compared to property tax revenues, which support debt service on the general obligation bonds.

Transit authorities harness sales tax revenue streams

Sales taxes often support public transit systems, which has largely insulated bondholders from declines in ridership that have plagued mass transit systems across the country since 2020. Several states, including Kansas, California, Utah and Virginia, have statewide sales taxes specifically dedicated to mass transit or state highway funds.

The Massachusetts Bay Transportation Authority (MBTA), which provides subway, ferry, bus and commuter rail service to the greater Boston area, benefits from a dedicated statewide 1% sales tax. The MBTA issues municipal bonds backed by the sales tax to fund its capital program (senior bonds rated Aa2 by Moody’s, AA+ by S&P and AAA by Fitch). Revenues from this sales tax provide ample support for debt service, providing over three times coverage, which allows the bonds to carry strong credit ratings and borrow at lower cost.

Other states, such as Colorado, Illinois, Georgia, Missouri and Oregon, authorize local or regional taxes for transportation projects. One example is the Dallas Area Rapid Transit System (DART), which provides bus, light rail and commuter rail services in the Dallas area. It is primarily funded by a 1% local sales tax levied throughout five counties and 13 municipalities surrounding the city of Dallas. DART issues bonds secured by a lien on sales taxes, but the bonds are also paid by other DART revenues such as passenger fares. Sales tax revenues have historically provided over three times coverage, and the bonds are rated Aa2 by Moody’s, AA+ by S&P and AA by Fitch.

Sales tax bonds remain attractive despite economic uncertainty

Sales tax laws vary greatly from state to state, but for most states, sales taxes represent an important revenue source that supports operations and infrastructure. U.S. consumer spending growth is projected to be constrained in 2025, and shifting tariff policy creates additional uncertainty for sales tax revenue collections — both to the upside and downside.

However, governments that rely on sales tax revenues have budgeted conservatively, and sales tax bonds benefit from strong legal protections and considerable downside tolerance, making them sound investments in the municipal bond market.

Related articles

Contact us

- +1 312 917 7700

- 333 W Wacker Drive, Chicago, United States of America

1 Data source: Tax Foundation. “State and Local Sales Tax Rates, Midyear 2025,” 08 Jul 2025.

2 Data source: NASBO Fiscal Survey of States: Governors’ Proposed Budgets for Fiscal 2026

The Tax Foundation, State and Local Sales Tax Rates, Midyear 2025, 7/8/2025; National Association of State Budget Officers, Fiscal Survey of States, Spring 2025; United States Government Accountability Office. “Remote Sales Tax: Initial Observations on Effects of States’ Expanded Authority. Statement of James R. McTigue, Jr., Director, Tax Policy and Administration.” 14 Jun 2022; The Tax Foundation. “Sales Tax Base Broadening: Right-Sizing a State Sales Tax.” 24 Oct 2017; City of Las Vegas Annual Comprehensive Financial Reports FY 2020 – FY 2024; Moody’s Research, “Subdued spending growth through 2026 will drive bifurcated credit outcomes.” September 2025.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her financial professionals.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Performance data shown represents past performance and does not predict or guarantee future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. For term definitions and index descriptions, please access the glossary on nuveen.com. Please note, it is not possible to invest directly in an index.

Important information on risk

Investing involves risk; principal loss is possible. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Investing in municipal bonds involves risks such as interest rate risk, credit risk and market risk. The value of the portfolio will fluctuate based on the value of the underlying securities. There are special risks associated with investments in high yield bonds, hedging activities and the potential use of leverage. Portfolios that include lower rated municipal bonds, commonly referred to as “high yield” or “junk” bonds, which are considered to be speculative, the credit and investment risk is heightened for the portfolio. Bond insurance guarantees only the payment of principal and interest on the bond when due, and not the value of the bonds themselves, which will fluctuate with the bond market and the financial success of the issuer and the insurer. No representation is made as to an insurer’s ability to meet their commitments. This information should not replace an investor’s consultation with a financial professional regarding their tax situation. Nuveen is not a tax advisor. Investors should contact a tax professional regarding the appropriateness of tax exempt investments in their portfolio. If sold prior to maturity, municipal securities are subject to gain/losses based on the level of interest rates, market conditions and the credit quality of the issuer. Income may be subject to the alternative minimum tax (AMT) and/or state and local taxes, based on the state of residence. Income from municipal bonds held by a portfolio could be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service or state tax authorities, or noncompliant conduct of a bond issuer. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

Nuveen, LLC provides investment solutions through its investment specialists.

This information does not constitute investment research as defined under MiFID.