What began as enthusiasm for generative models has evolved into a full-scale, multi-year investment cycle to build the computational, energy and physical infrastructure of a new industrial era. For investors, this could offer capital allocation opportunities spanning all layers of the capital stack.

Key takeaways

- AI is a multi-year capital cycle, not a short-term trade. Scale, funding quality and physical constraints point to a structural investment cycle rather than a speculative technology boom.

- Returns extend beyond U.S. megacap technology stocks. The opportunity set increasingly spans credit, private markets, infrastructure and real assets financing AI deployment at scale.

- Digital and physical investments deliver distinct risk-return profiles. Near-term earnings momentum sits in semiconductors and other memory hardware and cloud computing, while power, grids and cooling systems are likely to shape returns over the next decade.

- Diversification is possible across asset classes. Investors can align growth, income and inflation protection objectives with opportunities across the AI value chain.

- A key risk is concentration, not adoption. Returns will cluster by capital structure, geography and physical capacity.

AI as a structural capital cycle

Artificial intelligence (AI) is not simply a technological breakthrough. It is a capital cycle unfolding at unprecedented scale and speed, reshaping how companies invest, how governments design industrial policy and how energy and infrastructure systems are built.

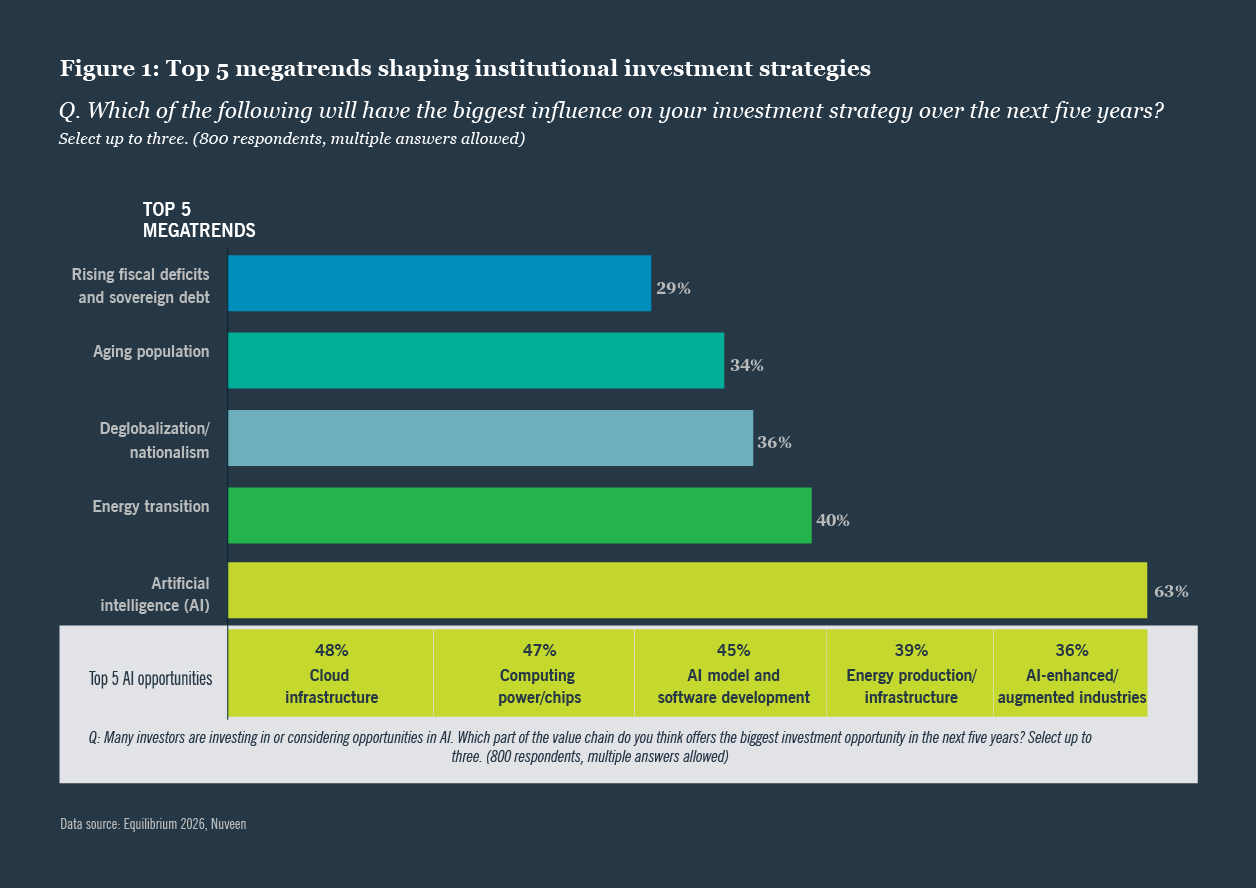

With AI poised to influence so many aspects of economic life, it is unsurprising that it was identified as the top megatrend shaping investment strategy in Nuveen’s 2026 EQuilibrium survey of global institutional investors (fig. 1). As providers of long-term capital, these investors need to explore the implications of this investment cycle — one which we expect to unfold across many years, if not decades or even generations.

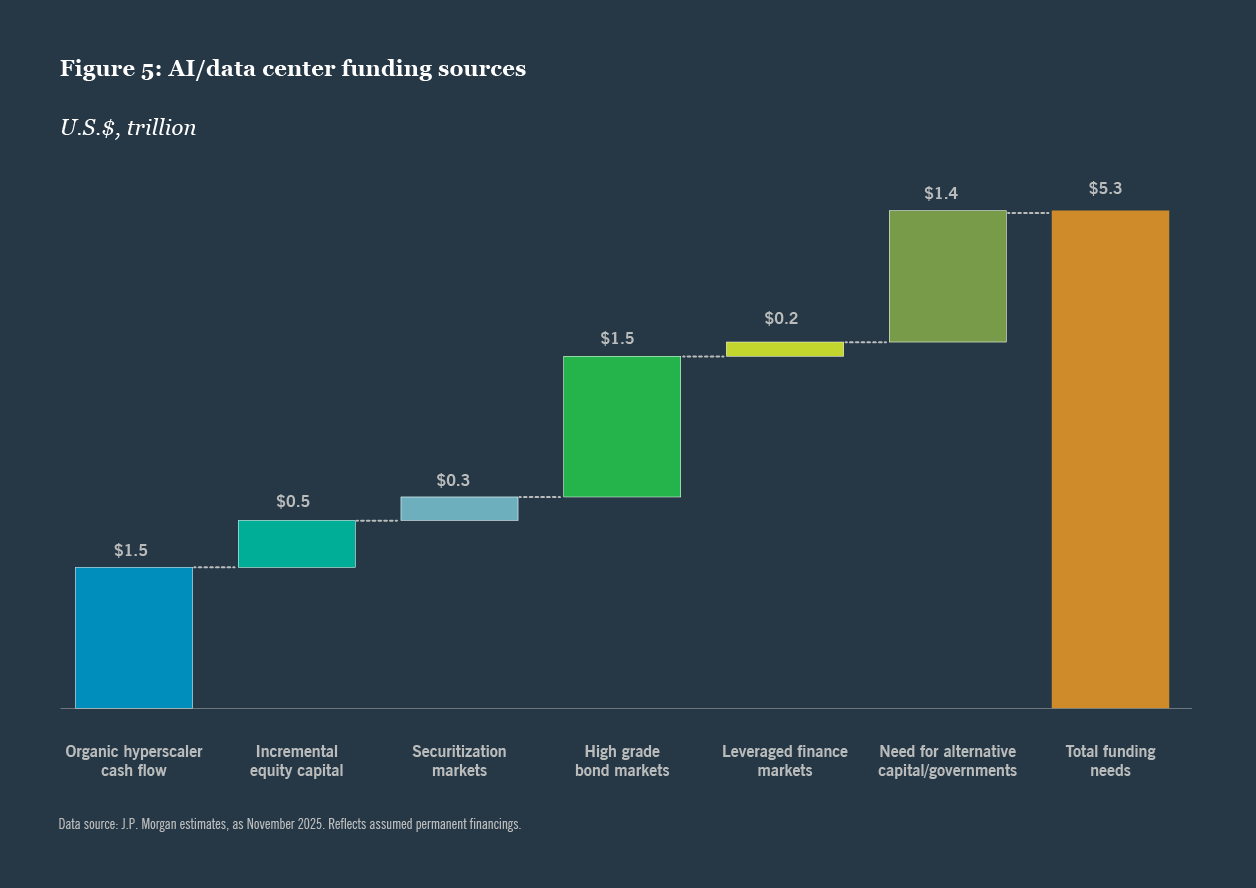

A defining characteristic of this cycle is the quality of investment driving it. The world’s most profitable corporations are funding large portions of AI infrastructure with internally generated cash flows, while governments are incentivizing innovation and adoption through subsidies and tax breaks across multiple sectors. And recently, debt markets have become a vital source for funding.

For investors, this reframes AI from a thematic exposure into an expansive allocation opportunity — one defined by duration, capital intensity and cash-flow durability across the AI value chain.

Capturing the full return potential of this supercycle requires understanding how the transformation is financed and having exposure across the capital stack: from innovation-driven equities to contracted, asset-backed cash flows at the infrastructure layer.

AI as a supercycle, not a bubble

Not all growth cycles are created equal. Supercycles are rare periods where new technologies reshape economic activity across multiple industries rather than simply driving short-term company earnings. Artificial intelligence fits that definition.

In contrast to classic financial bubbles that tend to be driven by cheap leverage and speculative capital, today’s AI leaders exhibit the opposite: robust earnings, net cash positions and investment plans that are largely self-funded.

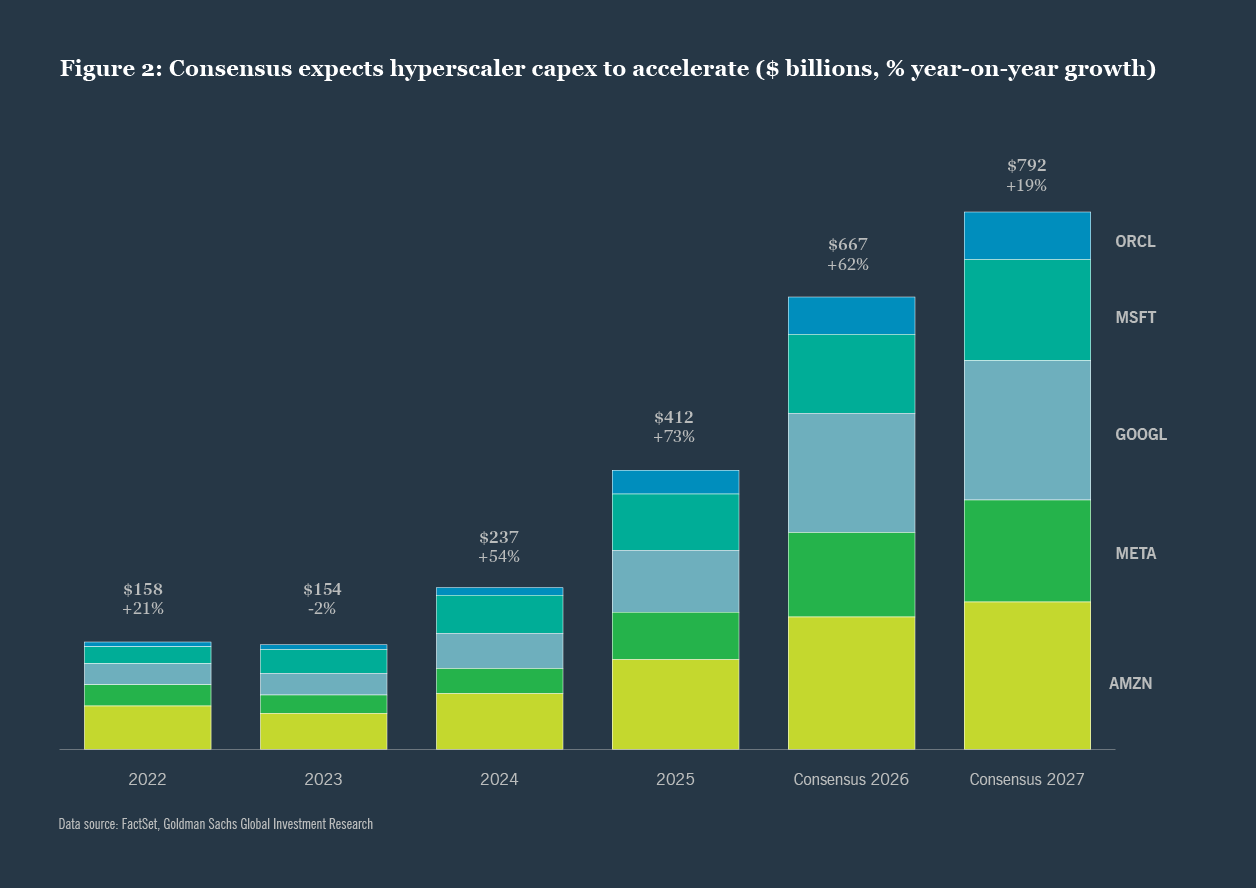

Hyperscaler capital expenditure (capex) is accelerating (fig. 2), with supply chains for semiconductors, advanced packaging, cooling and power-distribution expected to remain constrained at least until the end of the decade.1

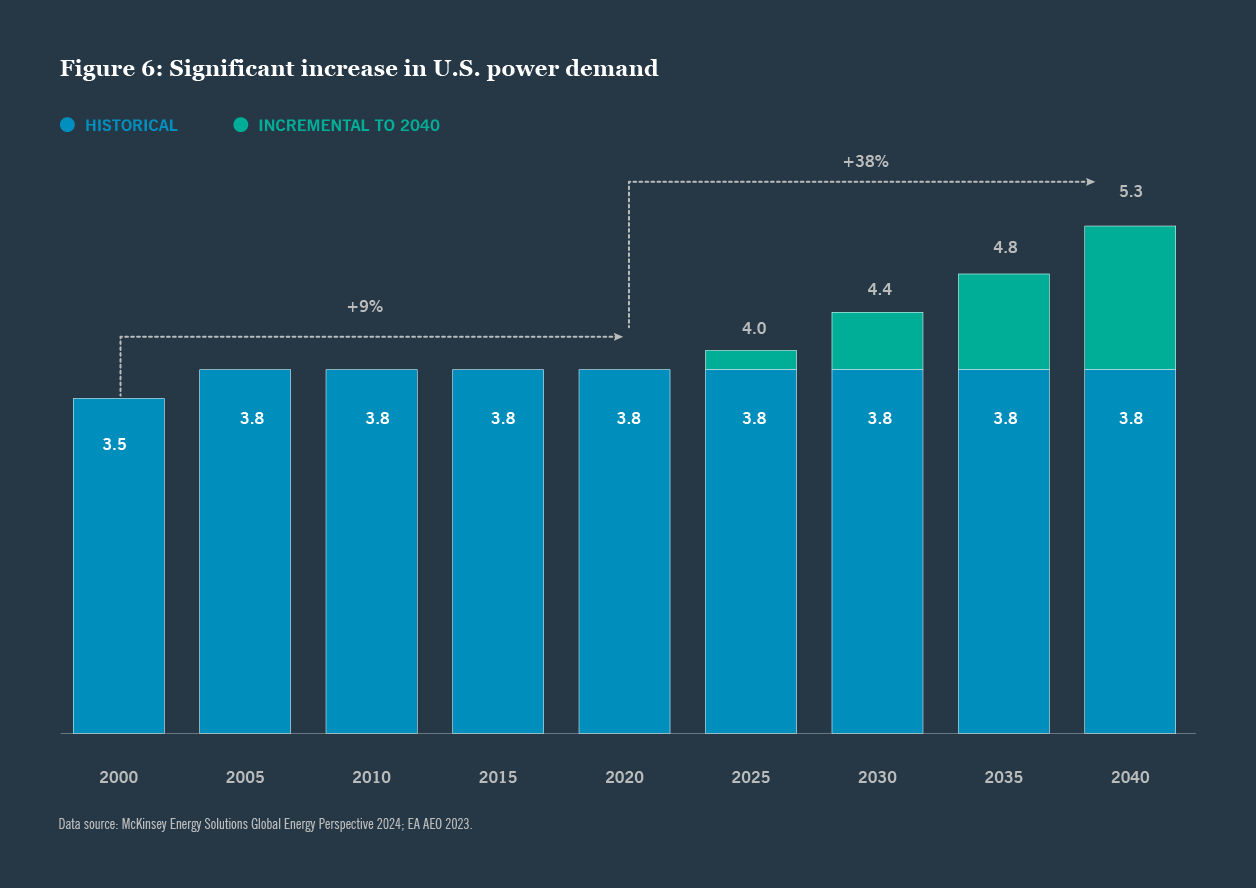

Industrial policy is further reinforcing this cycle. The U.S. CHIPS Act, the European Union’s AI Act, Japan’s digital industrial strategy and China’s localization push are embedding structural demand across geographies. Furthermore, physical capacity (namely, power, land, transmission and cooling) is a binding constraint, which will take years rather than quarters to change.

Investing across the capital stack

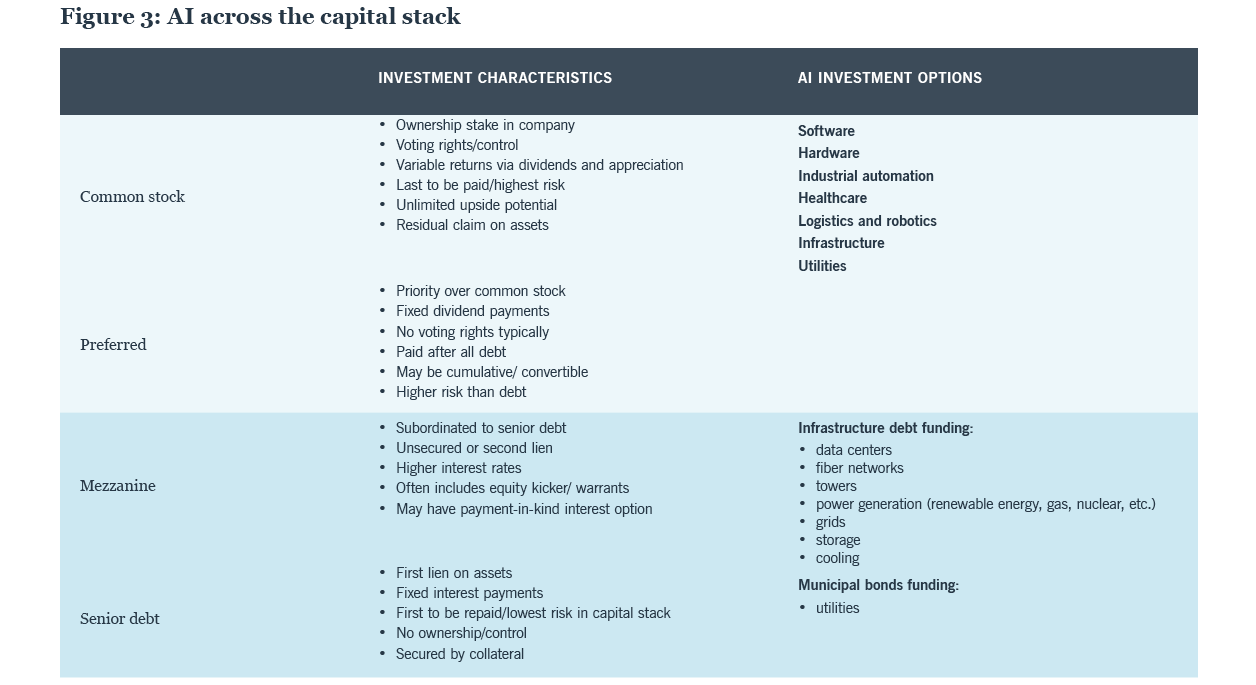

The AI supercycle is unfolding across the capital stack. At the top sit equity holders capturing earnings growth and innovation upside. In the middle and the remainder of the stack are credit investors financing AI‑related capital expenditure with priority claims on cash flows.

Returns across the stack differ not only in magnitude, but also in timing, volatility and sensitivity to execution, valuation and regulation. Understanding where to position within this structure (fig. 3) is central to long-term portfolio construction.

The AI cycle is unfolding across the capital stack

Cross-asset positioning: allocating across the AI capital cycle

Public equities: growth and earnings momentum

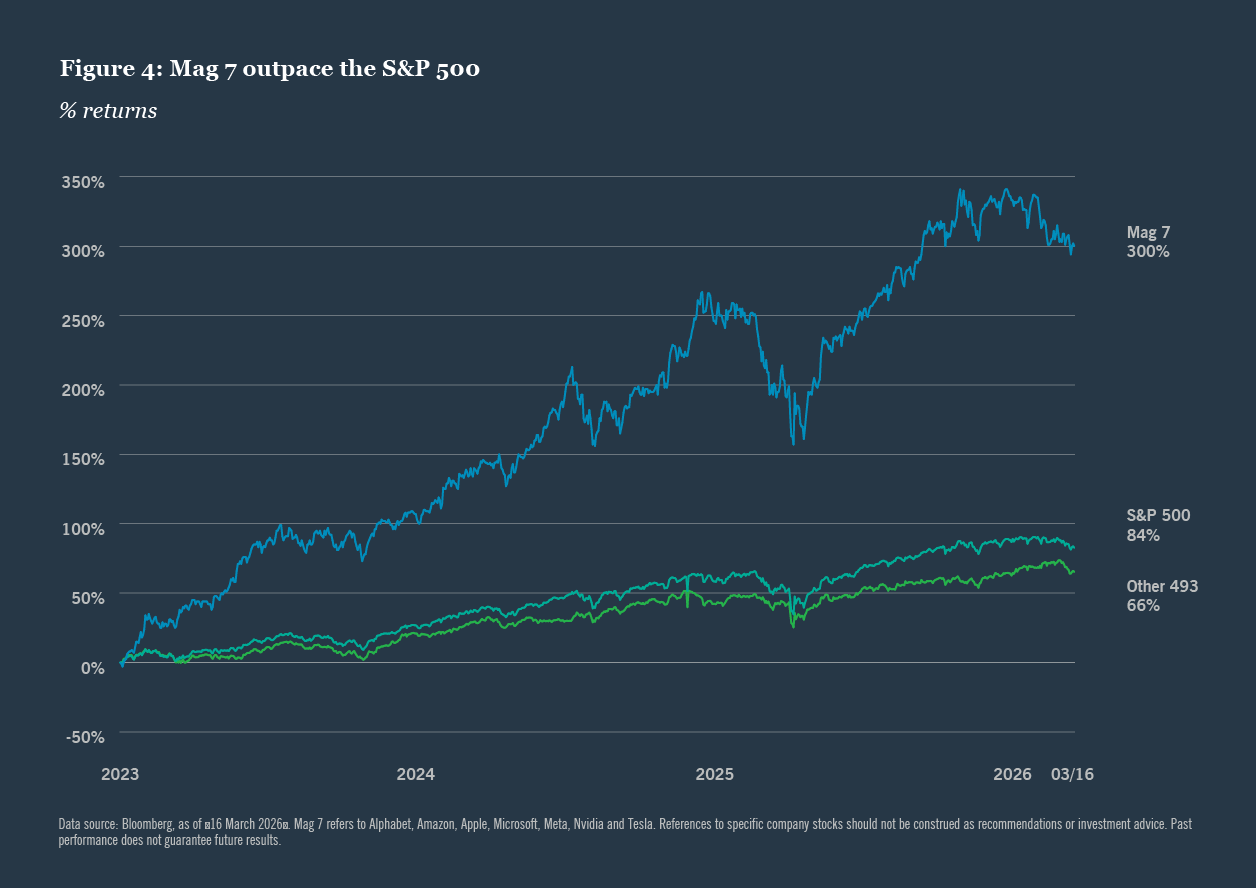

Equities continue to offer a compelling combination of growth potential and exposure to structural change, with AI adoption serving as both a catalyst for earnings expansion and a driver of evolving stock market leadership. Dominant U.S. technology companies have powered recent gains with AI-related spending and productivity investments underpinning stronger profit trajectories, even in the face of rich valuations (fig. 4). While elevated multiples have raised questions around concentration risk, particularly among a narrow cohort of megacap names, we believe those are, in many cases, supported by fundamental earnings growth potential.

At the same time, the equity opportunity set is broadening. As markets digest the implications of AI and capex shifts, we see productivity gains becoming embedded across sectors: from U.S. industrial automation to logistics platforms, healthcare technology and beyond. This diffusion of AI-enabled productivity is beginning to unlock second-order effects in areas that have previously been underappreciated by traditional valuation frameworks.

At the sector level, hardware is underpinned by strong demand driven by data movement, storage and analytics. And as AI expands the types of threat and their complexity, incremental spending in cybersecurity is likely to remain resilient in this relatively unique part of the market. Elsewhere, AI-adjacent sectors are positioned to benefit from the power shortfall, from industrials to energy.

The upside potential, however, also comes with heightened sensitivity to multiple compression, earnings disappointment and concentration risk. And recent scrutiny on the software sector captures how the themes that have propelled markets higher — strong earnings forecasts, robust corporate margins and AI enthusiasm — can also change quickly as AI-led disruptions emerge as the cycle evolves. This reinforces the importance of selectivity and disciplined diversification.

Opportunities have also expanded internationally. European and Japanese industrials, which stand to capture broader AI adoption in manufacturing and services across the real economy, currently appear more attractively valued relative to their U.S. counterparts, in our view.

Rates and duration: the often underappreciated enabler

Power generation, transmission, grid upgrades and data center infrastructure require long-term financing, creating a structural bid for high-quality duration assets. Investment grade utilities, infrastructure debt and long dated project finance provide exposure to AI-driven investment with defensive characteristics: lower volatility, strong asset backing and greater cash-flow visibility.

Credit: defensive carry with structural tailwinds

While equities capture earnings growth and valuation upside, credit investors can also access these structural tailwinds.

In public markets, U.S investment grade utilities are entering one of the most significant grid-upgrade cycles in decades. Electrification, data center power demand and network resilience are driving elevated capex plans, supported by regulated, inflation-linked cash flows and improving accelerating rate-base growth as utilities invest to expand and modernize the grid.

Long-dated project finance and infrastructure debt offer exposure to AI-driven investment with the defensive characteristics of lower volatility, strong asset backing and predictable cash-flow visibility. Select high yield industrial and technology issuers tied to automation, networking and data infrastructure could further broaden the opportunity, benefitting from stronger free cash flow and more disciplined balance sheets than in prior cycles.2

While municipal government bonds are not a direct AI play, the asset class fundamentals can gain support over time through productivity gains, infrastructure investment and stronger local tax bases in tech-heavy regions. AI exposure can be expressed selectively through infrastructure-linked revenue bonds or geography.

In private markets, direct lending is increasingly becoming a core financing channel for the AI ecosystem. Senior loans to mid-market data center operators, cooling and power management specialists and network-interface providers currently offer yields in the 8.5% – 12% range.3 Collateralized loan obligations further broaden floating rate exposure across technology, telecom infrastructure and AI-linked software, offering income resilience in a higher-for-longer rate environment.

Crucially, private credit allows investors to tailor exposure to the AI supply chain, translating thematic conviction into contracted, cash flow-driven returns through underwriting discipline, covenant protections and asset backed structures.

Real assets and infrastructure: debt and equity opportunities

Digital infrastructure, including data centers, fiber networks and towers, alongside energy infrastructure such as power generation, grids and storage, represent essential inputs to scaling AI adoption. Their long-dated contractual revenues and high barriers to entry support stable cash flows, making these assets well suited to absorb the significant capital investment required to meet rising demand.

Infrastructure debt and private credit strategies provide senior exposure with attractive income profiles, offering the potential for 10% – 12% returns for senior structures and 13% – 18% for more opportunistic capital.4 By contrast, equity and hybrid structures allow investors to participate in the long-term growth of infrastructure assets as revenues rise and operators expand capacity to meet increasing demand.

Risks: concentration, execution, policy and power

New technology brings new risks. These risks do not undermine the AI investment case, but they shape where along the value chain returns may accrue and how volatile they may be.

Concentration risk remains elevated in public equities. While likely to broaden, equity market leadership remains narrow, and earnings expectations are increasingly concentrated in a small group of hyperscalers and semiconductors suppliers. That concentration heightens sensitivity to sentiment shifts and short-term valuations compression, particularly where expectations run ahead of reality.

Aggressive capex plans present execution risk. AI is capital intensive and supply-chain dependent, spanning advanced semiconductors, memory hardware, networking, power and physical infrastructure. Delays in fabrication, packaging, grid connections or data center commissioning can slow revenue realization even when end demand is strong.

Policy and regulatory risk vary across countries and regions. Export controls, national AI strategies, energy regulation and grid permitting, for example, will influence capex decisions and potentially redirect capital flows. Geopolitical tensions in the AI race add complexity for firms operating across jurisdictions, impacting supply chain flexibility in areas such as semiconductors and critical minerals.

Physical capacity, especially electricity, has emerged as the defining constraint of AI implementation. Rapid AI data center deployment often has direct implications for power price inflation and grid stability for local communities, among other sustainability considerations.5 This can threaten the viability of project developments and give rise to tensions between the developers and the local municipalities.

Global regions: different strategies, distinct opportunities

As AI scales globally, it is fragmenting into regional ecosystems shaped by industrial strategy, capital availability and regulation. That fragmentation creates distinct opportunity sets for investors with cross-border reach.

U.S.: As the innovation and deployment leader, opportunity spans the full capital stack: semiconductors, cloud platforms, AI-native software, power generation and grid infrastructure. In fixed income, investment grade utilities and infrastructure debt offer AI-driven exposure with long-duration, asset backed cash flows

Europe: Considered more an adopter and regulatory architect than a technology originator, companies in manufacturing, logistics and industrial automation are well positioned to capture AI diffusion. Regulated infrastructure assets benefit from long-term investment programs and inflation linkage. Europe’s emergence as the global reference point on AI governance may prove a durable competitive advantage over time.

Japan: AI deployment is tied to solving structural economic problems, such as labor constraints, productivity gaps and manufacturing competitiveness. Corporate governance reforms are improving capital discipline, further supporting a constructive view on Japanese equities.

China and Asia-Pacific: China leads in scaled, applied AI, such as robotics, logistics, smart cities and consumer-facing platforms. However, geopolitical and policy risk narrows the investable universe to domestic supply chains. Across Asia- Pacific more broadly, the region is central to the AI supply chain through semiconductor manufacturing, networking equipment and data center development, and energy, grid and transport infrastructure.

Regional differences reinforce the core thesis: AI exposure can be expressed through different combinations of growth, income, duration and inflation protection, without relying on a single market, technology or regulatory regime.

Regional differences reinforce the core thesis: AI exposure can be expressed through different combinations of growth, income, duration and inflation protection

Investing in progress

AI is reshaping the global economy from the inside out. It is redirecting capital allocation and building a new industrial base around computing, electricity and digital infrastructure. It is not a moment to time, but a supercycle. With such an expansive investment universe, investors can capture opportunities by positioning portfolios across capital structures, geographies and time horizons.

Featured insights

About the author

Contact us

- +44 20 3727 8000

- 201 Bishopsgate, London, United Kingdom

Endnotes

1 McKinsey Global Institute, “The economic potential of generative AI”, June 2023

2 Nuveen, “High yield bonds: No longer junk but still high yield”, February 2026

3 Preqin, Cliffwater Direct Lending Index, 2025

4 Nuveen, 2026

5 For more information, read “A sustainable investor’s guide to AI” on nuveen.com

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her financial professionals.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Performance data shown represents past performance and does not predict or guarantee future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. For term definitions and index descriptions, please access the glossary on nuveen.com. Please note, it is not possible to invest directly in an index.

Important information on risk

Investing involves risk; principal loss is possible. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Investing in municipal bonds involves risks such as interest rate risk, credit risk and market risk. The value of the portfolio will fluctuate based on the value of the underlying securities. There are special risks associated with investments in high yield bonds, hedging activities and the potential use of leverage. Portfolios that include lower rated municipal bonds, commonly referred to as “high yield” or “junk” bonds, which are considered to be speculative, the credit and investment risk is heightened for the portfolio. Bond insurance guarantees only the payment of principal and interest on the bond when due, and not the value of the bonds themselves, which will fluctuate with the bond market and the financial success of the issuer and the insurer. No representation is made as to an insurer’s ability to meet their commitments. This information should not replace an investor’s consultation with a financial professional regarding their tax situation.

Nuveen is not a tax advisor. Investors should contact a tax professional regarding the appropriateness of tax-exempt investments in their portfolio. If sold prior to maturity, municipal securities are subject to gain/losses based on the level of interest rates, market conditions and the credit quality of the issuer. Income may be subject to the alternative minimum tax (AMT) and/or state and local taxes, based on the state of residence. Income from municipal bonds held by a portfolio could be declared taxable because of unfavorable changes in tax laws, adverse interpretations by the Internal Revenue Service or state tax authorities, or noncompliant conduct of a bond issuer. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

Taxable-equivalent yields are based on the highest individual marginal federal tax rate of 37%, plus the 3.8% Medicare tax on investment income. Individual tax rates may vary. Inflation rate used is the PCE Deflator, which is removed from the after tax income of the 3 month T-bill yield, resulting in an after tax and after inflation rate for cash.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Nuveen, LLC provides investment solutions through its investment specialists.

This information does not constitute investment research as defined under MiFID.