Key takeaways

- Asset-based finance (ABF) encompasses a large and diverse set of credit investments that differ fundamentally across collateral types, duration and, most importantly, in the nature of the downside protection they provide.

- A key distinction in ABF is between diversified pool strategies and single-asset deals, which differ substantially in the nature and source of downside protection they provide.

- Manager selection in ABF turns on three questions: how assets are sourced and whether the incentive structure aligns with investor interests; whether specialist underwriting expertise is present across each sub-strategy; and whether the manager has the expertise and experience to translate deal access into portfolios that target specific investor objectives.

- The application of ABF structures to renewable energy, digital infrastructure and grid modernization is expanding the opportunity set for long-duration investors.

Discover how the TIAA General Account takes a hybrid approach to ABF investing

A closer look at risk and structure

Institutional investors are increasingly allocating to asset-based finance, drawn by the secular retreat of banks from complex lending and the corresponding expansion of private markets as the primary source of credit intermediation. The structural case for the asset class is well established: collateral-backed credit with contracted cash flows offers diversification from corporate risk, spread premiums over public fixed income and structural protections that public markets rarely provide.

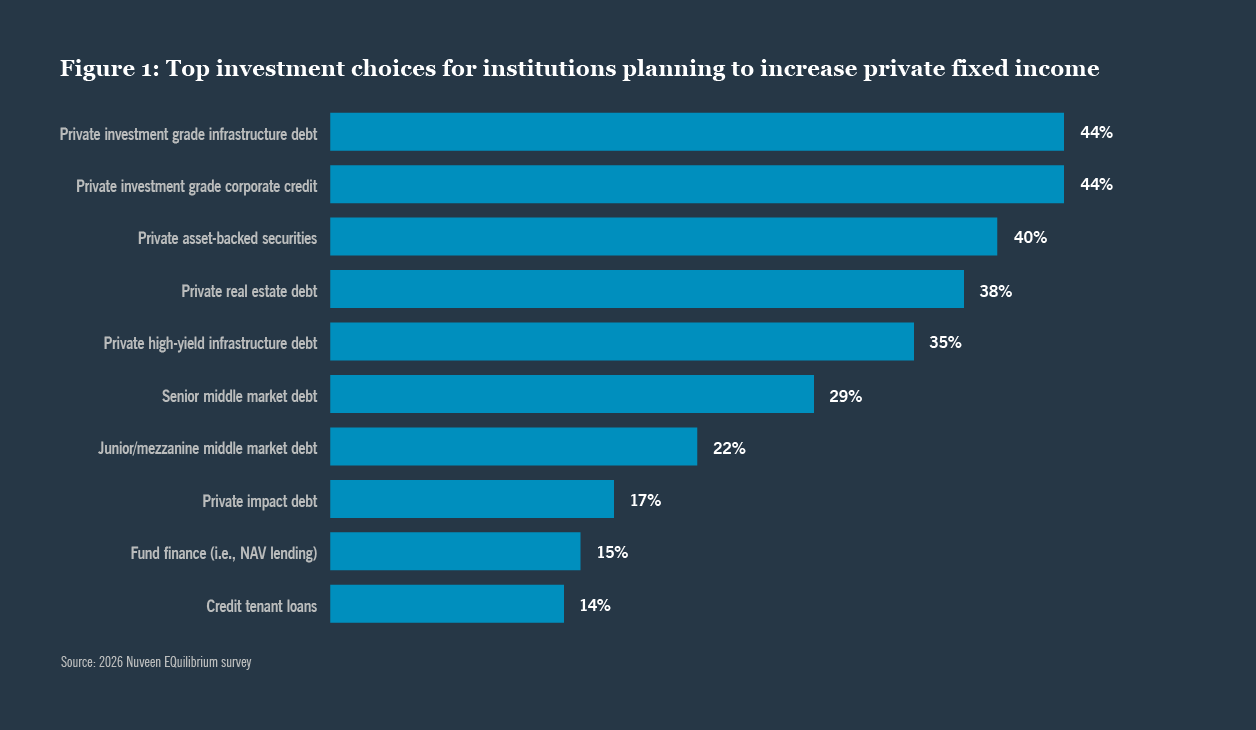

According to Nuveen's 2026 EQuilibrium Survey, 46% of institutional investors cite diversifying their alternative credit portfolio as a top priority over the next five years. For those planning to increase their allocation to private fixed income, 40% or more intend to direct capital specifically to private investment grade infrastructure debt and asset-backed securities. That intentionality suggests investors are moving past the question of whether to allocate to ABF and wrestling with a more demanding one: how to allocate within it.

The category now encompasses strategies that differ fundamentally in collateral type, duration, origination model and, most importantly, in the nature of the structural protections and security they actually provide.

This paper deconstructs the structural dimensions that distinguish ABF strategies from one another, and what those differences mean for manager selection and portfolio construction.

The breadth behind the ABF label

Beneath the ABF label lies a growing set of strategies that share a name but differ fundamentally in collateral type, structure and risk profile.

At its most basic, ABF covers any credit investment whose return is secured by discrete assets or cash flows, as distinct from corporate direct lending, which is ultimately backed by the enterprise value and operating cash flow of a business. The rapid expansion of private ABF as an institutional allocation has been predominantly a U.S. story, driven by the depth of U.S. consumer and commercial loan markets and the breadth of statutory and contractual frameworks that support asset-level collateralization. However, that is beginning to change, as similar structures gain traction in other jurisdictions.

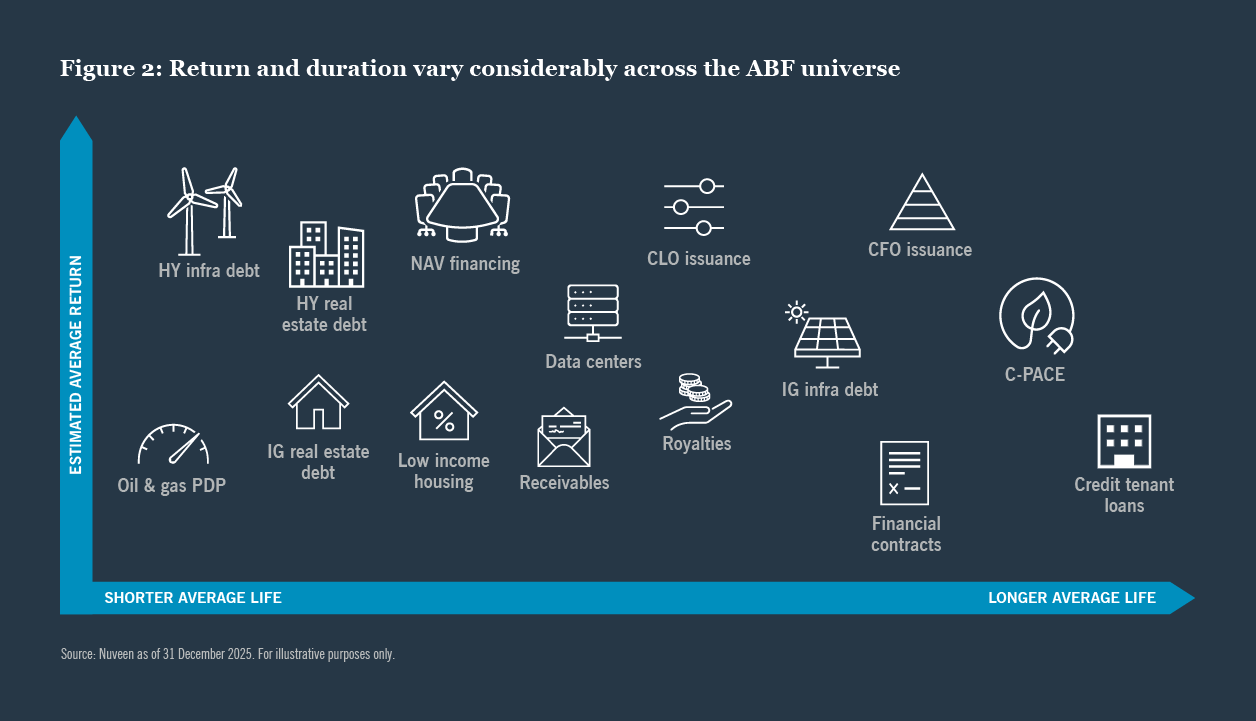

The universe of investment opportunities ABF has produced is vast. Consumer loan pools, trade receivables, equipment leases, credit tenant loans, project finance, infrastructure debt, Commercial Property Assessed Clean Energy (C-PACE), music royalties and data center receivables can all qualify, but they do not share a common risk profile.

A useful starting point is to divide the asset class into two broad segments: macro-sensitive ABF, where consumer credit and leasing strategies are meaningfully tied to the economic cycle, and real asset-based and infrastructure-oriented ABF, anchored in contracted cash flows, statutory liens or long-term obligations, a distinction we explore in the next section.

The duration characteristics of these two worlds are also distinct. Pooled consumer and commercial loan strategies typically carry a weighted average life of two to 12 years; credit tenant loans extends that range to 15 to 25 years; and infrastructure debt can span seven to 30 years. For investors managing long-dated liabilities, this spectrum matters as much as collateral type. Within each duration band, the nature of the structural protections and security differs substantially, and that difference has significant implications for how portfolios behave under stress.

Structural protections are important and varied

Understanding the structural protections and contracts in place is the most important consideration in any ABF investment. These can look very different between ABF investments consisting of diversified pools of collateral and single-asset deals.

When evaluating an ABF investment, understanding the credit risk embedded in the assets and corresponding cash flows is a necessary first step, but not sufficient to make a decision. Knowing how the investment is protected if things go wrong is paramount. Structural protections are common and critical in ABF investments to protect investors in the event of a downside scenario. These may include features such as cash sweeps and rapid amortization triggers in ABS deals backed by a pool of collateral. Additionally, financial maintenance covenants, distribution restrictions and even statutory protections can be common for infrastructure investments and other types of assets backed by single assets. Different types of structural protections and security features are not in competition: they can serve different portfolio objectives.

For example, some structured pools of ABF strategies rely on diversification across a large number of underlying obligors as a primary form of protection and the underwriting approach is unique to the collateral. Because the pool is generally too large to evaluate loan by loan — doing so would be prohibitively inefficient — the investor underwrites at the portfolio level based on criteria such as historical loss rates, loan-to-value distributions, geographic and credit score stratification and prepayment assumptions.

In most market environments, this approach to underwriting tends to be sound. The limitation is that this protection is backward-looking and probabilistic in nature. In a stress scenario, correlations across obligors that appeared modest in historical data can increase. This puts pressure on servicers, the third-party administrators responsible for collecting payments, managing delinquencies and enforcing loan terms on behalf of investors. At this point, the portfolio-level statistics that supported the original underwriting may evolve as the pool seasons or economic conditions shift.

The structural and contractual features embedded in the transactions — trustee arrangements, borrowing base tests, performance triggers and backup servicer provisions — are the actual factors designed to address these dynamics, and when properly constructed, they can be robust. Different tranches within a pooled structure may also carry meaningfully different protections and rights, adding another layer of differentiation.

For single-asset or small group transactions, there is greater transparency around the specific underlying investments, and the structural considerations, underwriting analysis and security features may be specific to those individual assets. C-PACE financing provides a clear example where the loan itself contains embedded security features through both law and contract. The senior tax lien that secures a C-PACE loan attaches to the property itself and is non-extinguishable. It survives foreclosure and takes priority over virtually all other claims on the asset. These features are a matter of property law and hold regardless of market conditions.

Similarly, many infrastructure debt investments are backed by contracts such as power purchase agreements, long-term leases, utility tariffs or contracted venue revenues. In these transactions there are typically also other forms of protection in place including financial covenants, restricted payment tests and reserves. However, in-depth analysis of the contracts is absolutely critical.

Knowing what you own

Each ABF sub-strategy demands a distinct set of underwriting skills, and the work does not end at the point of investment.

Understanding structural protections serves as a starting point. What converts structural positioning into durable performance is the quality of underwriting: the depth of asset-level expertise that allows a manager to better evaluate the risks and opportunities embedded in both the fundamental credit and structural components of a potential investment and identify problems before they become losses.

Underwriting expertise in ABF is a collection of highly specialized disciplines, and each sub-strategy demands a different skillset. Evaluating a consumer loan pool, for example, requires interrogating stratification data, modeling loss curves under stress and assessing the equity sponsor behind the collateral. Evaluating a C-PACE loan requires knowledge of property law, lien priority mechanics and local real estate dynamics. Evaluating infrastructure debt requires understanding contracted revenue streams, counterparty creditworthiness and the technical risks specific to a given asset. These disciplines share a commitment to asset-level rigor, but they draw on entirely different bodies of expertise.

Active monitoring is as important as the original underwriting decision. Ongoing engagement through covenant compliance reviews, servicer performance assessments and direct counterparty dialogue is what allows managers to protect value and respond decisively when conditions change.

Sourcing, incentives and the prerequisites for selectivity

The sourcing model behind an ABF portfolio, and the incentive structures surrounding that origination, are consequential dimensions of ABF investing.

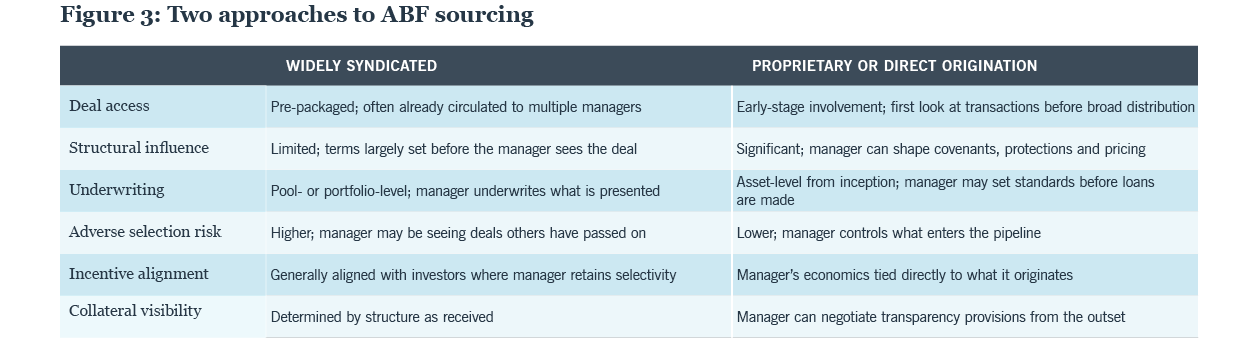

The quality of assets in an ABF portfolio begins with the process by which those assets are sourced. Sourcing models in ABF exist on a spectrum, from widely syndicated origination at one end (where investment opportunities typically arrive largely pre-packaged from agent banks and issuers) to direct platform ownership at the other, where the asset manager controls the origination process entirely.

Widely syndicated origination typically offers a large and robust deal funnel, but with this approach it may be more difficult to achieve desired allocations since investors have less influence on the terms and structure. Direct platform ownership, on the other hand, allows managers to set underwriting standards from inception and negotiate bespoke terms, but it also means sourcing investment opportunities from their own captive platforms. This carries an inherent tension when originators need volume to maintain profitability.

There is also a sizable middle ground in ABF that allows for large and sophisticated managers to invest in proprietary club-style transactions alongside a small group of investors or work directly with agent banks, third-party sponsors and third-party originators on proprietary transactions. With this approach, the manager will typically have more significant influence over the terms and structure of the transaction as well as be able to size the deal or allocation according to investor needs.

Regardless of the sourcing model or combination thereof, it is important for investors to understand the manager's approach and the ability of the manager to remain selective and choose only the investment opportunities that are the best fit for their client portfolios.

Building portfolios across a growing opportunity set

Innovative ABF structures are increasingly being applied to markets where the need for institutional capital is greatest.

The capital needs of energy transition and digital infrastructure buildout are massive, long-dated and no longer adequately served by traditional lending markets. ABF structures are playing an increasingly vital role in bridging that gap, expanding the opportunity set for institutional investors.

Capturing these opportunities requires both origination expertise and structural capability. For insurers managing long-duration liabilities, for example, regulatory capital requirements make the form of an investment as important as its economics. Rated note feeder structures have emerged as an important mechanism for meeting those requirements while preserving access to the full breadth of the opportunity set. Developing that wrapper requires sophisticated legal and structuring capability alongside specialist investment management. Thus, the ability to combine both is an important consideration in manager selection.

What the label doesn't tell you

The investors best positioned to capture ABF's potential are those who look past the label to the quality of protection, sourcing and underwriting underneath it.

Asset-based finance is a large and diverse opportunity set, and the ABF label itself conveys very little about what any given strategy actually offers or how it will behave under stress. Investors who approach it with the rigor the category demands can source durable income, stable cash flows and meaningful diversification from corporate credit.

The investors better positioned to capture ABF's potential have a long investment horizon and a liability structure that does not require daily liquidity. This allows them to systematically capture the spread premium that private ABF offers over public equivalents. Investors with this positioning can also approach the category with enough analytical granularity to distinguish between sub-strategies rather than treating ABF as a single, undifferentiated allocation.

The most important questions in ABF remain structural. What is the source of the protection? Who controls the origination, and what incentives surround it? Does the underwriting reflect asset-level expertise across each sub-strategy? And can the portfolio be constructed to match the investor's specific objectives? Investors who build their ABF allocations around those questions will be well positioned to capture what remains one of the most compelling opportunities across private markets.

Related insights

Investment capabilities

Contact us

- +1 312 917 7700

- 333 W Wacker Drive, Chicago, United States of America