The structural case for transitional CRE debt: A perspective for U.S. life insurers

Key takeaways

- The current opportunity in transitional CRE debt is structural and supply-driven, with the dislocation rooted in capital availability rather than any deterioration in borrower or asset quality.

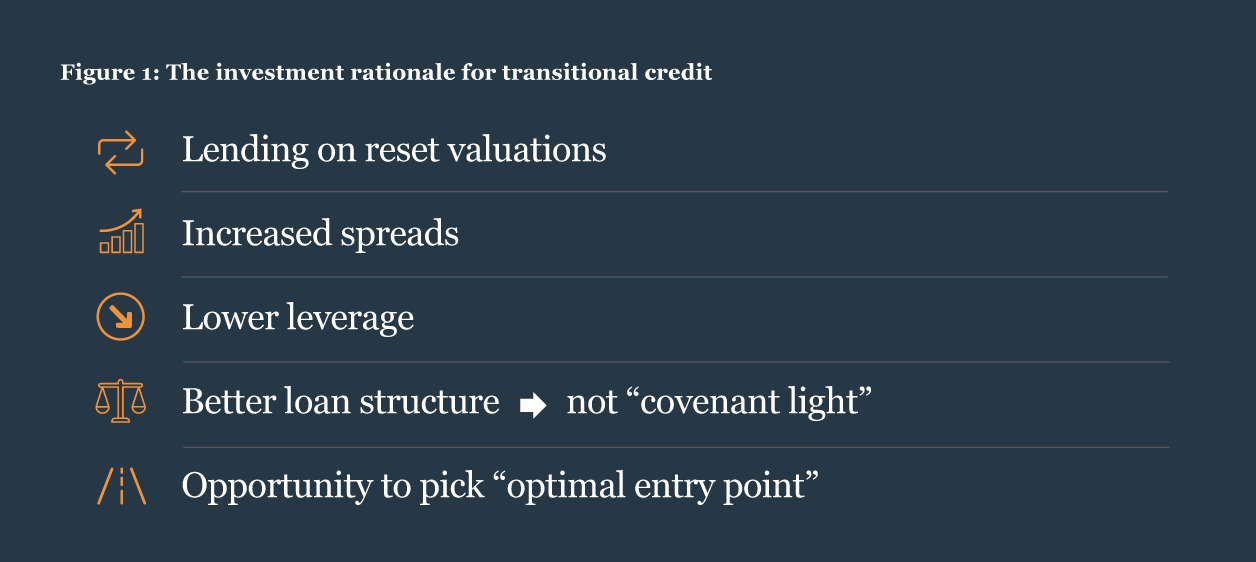

- CRE valuations have reset 20% to 30% from peak levels, and transitional lenders are now originating against those lower values, at spreads above prior-cycle averages and with stronger structural protections than the prior liquidity cycle allowed.

- For life insurers, a well-sized allocation to transitional CRE debt offers an attractive floating-rate complement to a core commercial mortgage loan book.

Over the past several years, rate normalization and a reset in commercial real estate (CRE) valuations have fundamentally altered the landscape for transitional lending, the floating-rate, shorter-duration segment of the market that sits above the core commercial mortgage loan but below the purely opportunistic end of the risk spectrum. The conditions that now define this space are different in kind, not just degree, from what existed when base rates were near zero.

For life insurers, core commercial mortgage loans (CML) have long been a natural fit: long-duration, fixed-rate, investment-grade and well-suited to liability-matching balance sheets. While this allocation remains firmly in place, the role of transitional CRE warrants closer examination. Historically a peripheral consideration for insurers, this segment is becoming increasingly relevant within portfolio construction.

Transitional lending is a financing gap story, not a distress story

Transitional lending encompasses floating-rate loans, typically three to five years in duration, made against properties undergoing some form of change, such as a lease-up, a renovation, a recapitalization or a repositioning. The loan types span senior mortgages, construction facilities, mezzanine debt and preferred equity. The common thread is that the underlying asset has a business plan, and the lender is underwriting both the real estate and the sponsor’s ability to execute.

Today’s transitional lending environment is often mischaracterized. It is not a distressed trade, in which lenders acquire impaired assets at deep discounts or rely on credit improvements to generate returns. Rather, the current opportunity is structural and supply-driven: a gap has emerged between the volume of transitional CRE activity requiring financing and the capital available to meet that demand. In most cases, borrower quality remains sound, and the dislocation lies in capital availability, not in the underlying real estate.

Three structural shifts behind the current opportunity

The attractiveness of transitional CRE reflects three interconnected forces, none of which is likely to reverse quickly.

Banks have become facilitators, not competitors. For most of the post-Global Financial Crisis (GFC) era, regional and money-center banks were the primary providers of transitional CRE capital. Successive rounds of regulatory capital requirements have made direct whole-loan CRE exposure increasingly costly to hold on a bank balance sheet, and as a result, banks have pulled back from primary direct lending in this segment. Today, banks have migrated into a different role, acting as active providers of back-leverage and warehouse financing to non-bank credit funds, a form of exposure that carries more favorable regulatory capital treatment than direct mortgage lending. As banks have returned to the market, they have functioned more as a source of cost-effective leverage for credit funds than as competitors in the origination market.

Values and financing costs have reset to more defensible levels. The normalization of base rates from near-zero to the current 4%+ range was indeed disruptive for the CRE market broadly, but it has created a more defensible entry point for transitional lenders. CRE valuations have declined 20% to 30% from peak levels, and those reset values are now supported by several years of transaction volume, with real price discovery behind them rather than theoretical marks. The result is a set of conditions that did not exist before 2022: lending on lower appraised values, at spreads estimated at 25–40 basis points above prior-cycle averages, with better structural protections and tighter covenants than a liquidity-saturated market would have allowed. More of the return now comes from the fundamental economics of the loan (base rate plus spread) than from financial leverage, resulting in a more durable return profile.

The maturity wall is compressing, and deal flow is expanding with it. A significant volume of CRE loans originated when base rates were effectively zero — approximately 37% of maturities between 2025 and 2027 were originated when the Fed funds rate was below 25 basis points — are now coming due in a markedly different financing environment. This dynamic is driving volume and deal flow for transitional lenders. Borrowers need to refinance into current market conditions, and the duration of new transitional loans is shorter than the paper it is replacing. This means the maturity cycle will turn over more frequently, sustaining the origination opportunity across multiple vintages.

A genuine complement to a core CML allocation

For a life insurer with an established core CML allocation, transitional CRE debt offers portfolio characteristics that are genuinely complementary rather than duplicative.

The floating-rate structure of transitional loans provides an offset to the fixed-rate duration in the core book, diversifying interest-rate exposure. The current yield premium over investment-grade fixed income alternatives, available at comparable or lower leverage and backed by real asset collateral with senior claims, represents an attractive risk-adjusted trade-off for the value-add portion of a real estate debt allocation. Conservative loan-to-value (LTV) ratios, reset lower than prior-cycle averages, provide downside insulation at the position level.

From a sector positioning standpoint, housing and logistics currently offer attractive relative value, with structural demand tailwinds and sufficient transaction volume to support reliable price discovery. In the current environment, it is possible to achieve value-add returns in these sectors for core-plus risk. Office, by contrast, combines well-understood macro headwinds with a lack of price transparency that makes underwriting difficult to defend at value-add return thresholds.

Vehicle structure is also an important consideration. In our view, the appropriate format for accessing transitional CRE debt is a closed-end, vintage-focused fund sized for the opportunity it intends to capture. A well-disciplined manager sizes the vehicle to what the market can absorb at the targeted return profile, maintains that discipline and moves to the next vintage when conditions warrant.

In the current environment, it is possible to achieve value-add returns in these sectors for core-plus risk.

Platform attributes that translate structural opportunity into portfolio outcomes

The structural opportunity in transitional CRE debt is meaningful, but execution quality can vary significantly. When evaluating a manager, four attributes matter most:

• Origination scale and deal flow quality. The best transactions in this market are rarely widely marketed. A manager with regional teams on the ground, deep sponsor relationships and a high rate of repeat borrower activity has a sourcing advantage that compounds over time.

• Integrated equity and debt platform. A lender with visibility into both the ownership and credit sides of a property type — exit cap rate assumptions, sponsor execution track record, where equity buyers are underwriting values — makes better credit decisions than one operating with a narrower lens.

• Capital markets capability. Transitional CRE debt strategies typically employ moderate back-leverage, and cost-of-leverage differentials between large and small platforms are meaningful. That differential accrues directly to investor returns.

• Vintage discipline in vehicle sizing. Oversized vehicles either fail to deploy or drift from their stated strategy. Both outcomes undermine the investment thesis. How a manager sizes its funds relative to the available opportunity is one of the most reliable signals of alignment with its investors.

Structural change in the financing landscape makes the case for a fresh look

The case for adding transitional CRE debt exposure rests on attractive structural conditions that have accumulated over several years and are unlikely to normalize quickly.

For life insurers, transitional lending now offers something genuinely additive: a differentiated return stream, a complementary risk profile and an entry point that the market has not offered in some time.

Nuveen Real Estate is one of the largest real estate managers in the world, with $43.8 billion in CRE debt AUM globally. The U.S. debt platform has averaged $4.7 billion in annual originations over the past five years, supported by a team of dedicated debt professionals operating a decentralized, locally embedded origination model. As part of a broader $136 billion real estate platform, the debt business benefits from the integrated equity and property expertise that we believe is essential to sound credit underwriting in transitional lending. For life insurers looking to establish or expand a transitional CRE debt allocation, please reach out to your Nuveen representative.1,2

Additional insights for insurers

About the author

Contact us

- +1 312 917 7700

- 333 W Wacker Drive, Chicago, United States of America

Endnotes

1. One of the largest RE manager source Pensions & Investment Real Estate Managers Special Report, Nov 2025. Ranking included 63 real estate managers and ranked them by total worldwide real estate assets as of 30 Jun 2025. Real estate assets are reported net of leverage, including contributions committed or received but not yet invested; REOCs are included with equity; REIT securities are excluded.

2. As of 31 Mar 2026.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on factors such as market conditions or legal and regulatory developments. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions made in preparing this material could have a material impact on the information presented herein. Past performance is no guarantee of future results. Investing involves risk; principal loss is possible. This information does not constitute investment research as defined under MiFID. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

A word on risk

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance is no guarantee of future results. Investing involves risk; principal loss is possible. Important information on risk Investing involves risk; loss of principal is possible. Real estate investments are subject to various risks associated with ownership of real estate-related assets, including fluctuations in property values, higher expenses or lower income than expected, potential environmental problems and liability, and risks related to leasing of properties. The real estate industry is greatly affected by economic downturns or by changes in real estate values, rents, property taxes, interest rates, tax treatment, regulations, or legal. Prices of equity securities may decline significantly over short or extended periods of time. Nuveen Real Estate is a real estate investment management holding company owned by Teachers Insurance and Annuity Association of America (TIAA). All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. This information does not constitute investment research as defined under MiFID. Nuveen, LLC provides investment solutions through its investment specialists.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen, LLC.