TOOLS

Login to access your documents and resources.

Listen to this insight

~ 11 minutes long

Our complex framework of roads, waterways, utilities and airports must be maintained and expanded to meet evolving global needs. In the past, government has been largely responsible for creating and maintaining infrastructure. However, private funding has become an increasingly important resource as governments find themselves unable to cope with the challenges of modern infrastructure. Thus infrastructure has transformed from something that consumes tax dollars to a potential investment opportunity.

What is infrastructure?

Infrastructure typically refers to the technical structures that support a society, such as roads, bridges, water supply, sewers, electrical grids and telecommunications. Viewed functionally, infrastructure facilitates the production and distribution of goods and services and basic social services.

The urgent need for private capital

The pressing global need for infrastructure development and/or maintenance will require massive investment in the coming decades. When it comes to financing infrastructure projects worldwide, the fundamental imbalance between supply and demand will continue to widen, presenting potential investors with an array of new opportunities.

According to the Global Infrastructure Hub, global spending on basic infrastructure – transport, power, water and communications – is forecast to total $79 trillion from 2016 through 2040, while the actual investment need is $94 trillion.1 That means approximately $3.7 trillion is needed each year. That total is more than the annual economic output of the United Kingdom, the world’s sixth largest economy.2 Moreover, demand is increasing as population growth and global urbanization strain existing infrastructure and create a need for new development. The continuing urbanization and overall growth of the world’s population is projected to add almost one billion people to the urban population by 2050, with most of the increase concentrated in Asia and Africa.3 At the same time, the proportion of the world’s population living in urban areas is expected to increase, reaching two-thirds by 2050.3 This unprecedented migration into cities will require an equally vast investment in roads, water, communications and power.

Expanding and modernizing infrastructure is also a non-negotiable condition of economic growth, especially for developing countries. To compete successfully in the global market, such economies must invest heavily in new infrastructure to support growth initiatives and attract global capital. For example, India’s enormous growth potential is hampered by poor infrastructure.

Meanwhile, developed countries face the urgent task of replacing and upgrading aging or inadequate infrastructure. As demonstrated by California’s Camp Fire, the destruction caused by Hurricane Katrina or the bridge collapse in Minneapolis, even economic giants like the United States cannot overlook the impact of aging infrastructure.

Expanding privatization

The world spends some $2.5 trillion a year on the transportation, power, water and telecom systems that underpin economic activity and provide essential services. But this has not been sufficient to avoid significant gaps, and investment needs are only growing steeper. From 2016 through 2030, the world must invest about 3.8% of gross domestic product, or an average of $3.3 trillion a year, in infrastructure just to support expected rates of growth. This adds up to a cumulative need of $49 trillion over the entire period.4

To generate the capital to cope with this scale, governments have increasingly been reaching out to the private sector. Strained for financial resources and often loath to raise taxes, governments have found willing partners in private-market investors.

The expanding role of private funding in public infrastructure is still relatively new to the United States, but is well-established in other developed nations. It can take several forms, including full or partial privatization, public-private partnerships (known as PPPs or P3s) and private-to-private investments through asset sales and mergers. Private investors offer not only badly needed cash, but also administrative expertise, operational efficiency and accountability.

A significant investment opportunity

Today, essential infrastructure projects require more funds than governments can supply. As private markets are invited to assist, an investment universe has emerged with compelling characteristics:

Monopolistic. Components of infrastructure typically demand large-scale investments with very high fixed costs, creating high barriers to entry and monopolistic or quasi monopolistic characteristics. Geography also tends to limit proliferation of competing infrastructure projects.

Inelastic demand. Since the physical assets and services that make up infrastructure are necessities, demand does not fluctuate with price changes. For example, in 2008 the City of Chicago privatized its parking meters. Even though rates increased rather dramatically, there was little impact on overall demand for parking.5 Relatively inelastic demand makes infrastructure less sensitive to business cycles.

Stable cash flows. Long-term contracts between governments and private managers promote steady cash flows generated by fees or tolls on underlying assets. Concessions granted by governments to private entities to manage infrastructure assets can last up to 99 years.

Inflation hedge. As replacement costs of physical assets increase in an inflationary environment, they protect the value of infrastructure investments. Moreover, fees for the use of infrastructure are frequently linked to inflation measures through a regulated return framework or a contractually specified rate of return.

Durability. Infrastructure assets often last more than 50 years, with little or no risk of redundancy or technological obsolescence.

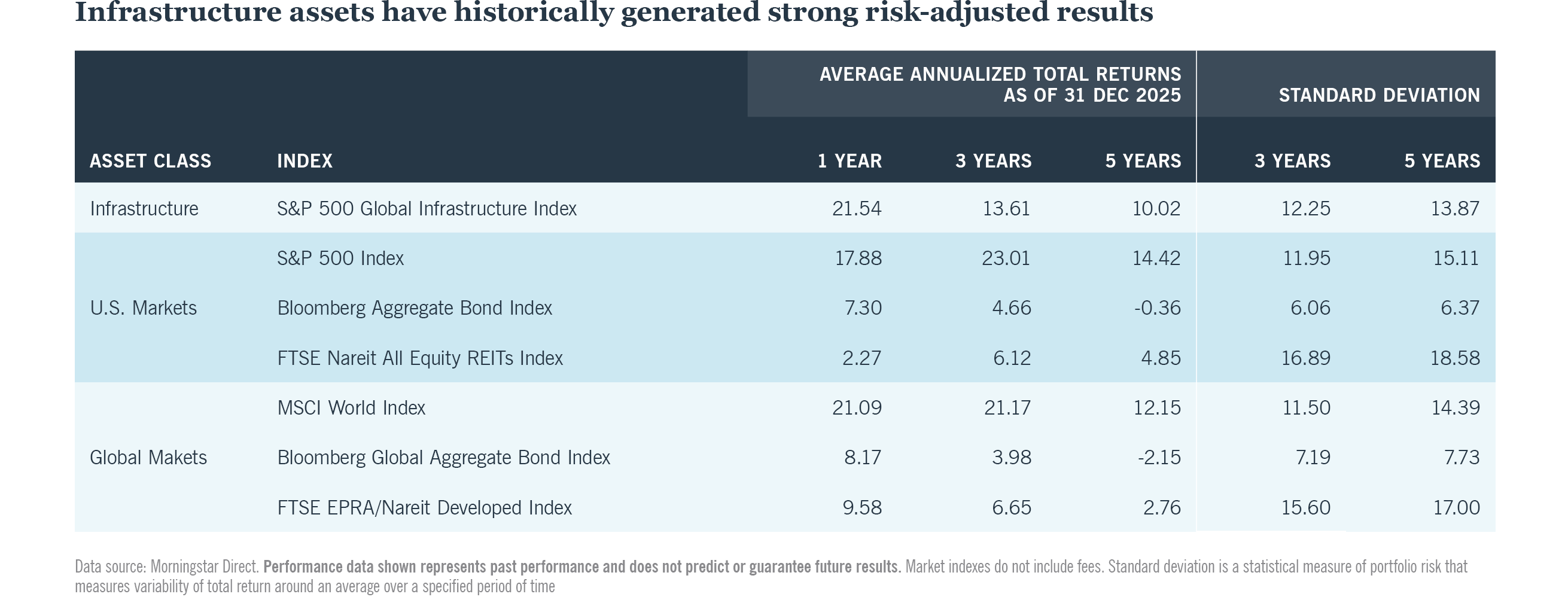

Due in large part to these qualities, infrastructure can be considered a distinct asset class, with potentially more stable, income-oriented returns that are not highly correlated with those of other major asset classes.

Investing in infrastructure

The most common ways to invest in infrastructure are direct investment, private equity investment or investment in listed (public) equity:

Direct investment allows an investor to become a financial backer and potential beneficiary in a specific infrastructure project through an equity stake or joint venture. This approach gives investors fairly stable cash flow and control over the underlying assets, but it involves a large capital outlay with uncertain prospects for residual values, offers limited diversification and generally requires specialists to manage.

As private markets are invited to assist, an investment universe has emerged with compelling characteristics.

Private equity partnerships invest directly in a variety of infrastructure assets or operating companies. Such investment vehicles may offer performance stability with consistent cash flows and higher levels of diversification than direct investment. However, they are still relatively illiquid, requiring significant up-front capital and often a long wait for asset placement. Due in part to the newness of these strategies, exit strategy options tend to be poorly defined. Private equity investment partnerships typically collect a percentage of the profits in addition to charging management fees.

Listed (public) infrastructure securities are issued by companies that own, construct or manage infrastructure assets. In contrast to direct and private equity investments, these investments offer greater liquidity, diversification and transparency. In addition, public partnerships and real estate investment trusts (REITs) have lower management fees than private partnerships. However, the return potential of listed infrastructure securities tends to be lower and they may exhibit slightly higher correlation with other public equities and more equity-linked volatility.

Complexities and barriers to entry can make investing directly in global infrastructure projects difficult for individual investors. We believe it may be beneficial to hire an investment manager that is experienced in the global infrastructure market to assemble a diversified portfolio that emphasizes stock selection and rigorous risk management.

Private investment will play a vital role

Given the surging demand for financial resources to sustain infrastructure initiatives, private investment will play an increasingly vital role as a funding source. Private equity investment, already very much in evidence in the global markets, has the potential to generate bond-like cash flows but is characterized by limited liquidity and high fee structures.

Related articles

Oil prices, Fed signals and rising Treasury yields shaped a challenging week for fixed income markets.

Senior loans may offer attractive returns due to spread widening, but active management may be necessary to manage risk.

The Fed extended its rate pause amid rising oil prices and geopolitical turmoil. See our updated outlook and top investment ideas for 2026.

Endnotes

Sources

1 Data source: Licensed from the Global Infrastructure Hub Ltd under a Creative Commons Attribution 3.0 Australia License. To the extent permitted by law, the GI Hub disclaims liability to any person or organization in respect of anything done, or omitted to be done, in reliance upon information contained in this publication.

2 Data source: Jessop, S. (2017, July 25). World needs $94 trillion spent on infrastructure by 2040: report. Retrieved from https://www.reuters.com/article/us-global-infrastructurereport/world-needs-94-trillion-spent-on-infrastructure-by-2040-report-idUSKBN1AA1A3

3 Data source: “World Urbanization Prospects, 2018 Revision of World Urbanization Prospects,” The United Nations, Department of Economic and Social Affairs. Most recent data available.

4 Data source: “Bridging Global Infrastructure Gaps,” McKinsey & Company, June 2016. Most recent data available.

5 Data source: “What Happened When Chicago Privatized its Parking System,” MinnPost.com, December 19, 2011; ChicagoMeters.com. Most recent data available.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Performance data shown represents past performance and does not predict or guarantee future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. For term definitions and index descriptions, please access the glossary on nuveen.com. Please note, it is not possible to invest directly in an index.

Important information on risk

All investments carry a certain degree of risk, including possible loss principal and there is no assurance that an investment will provide positive performance over any period of time. Because infrastructure portfolios concentrate their investments in infrastructure-related securities, portfolios have greater exposure to adverse economic, regulatory, political, legal, and other changes affecting the issuers of such securities. Infrastructure-related businesses are subject to a variety of factors that may adversely affect their business or operations, including high interest costs in connection with capital construction programs, costs associated with environmental and other regulations, the effects of economic slowdown and surplus capacity, increased competition from other providers of services, uncertainties concerning the availability of fuel at reasonable prices, the effects of energy conservation policies and other factors. Additionally, infrastructure-related entities may be subject to regulation by various governmental authorities and may also be affected by governmental regulation of rates charged to customers, service interruption and/or legal challenges due to environmental, operational or other mishaps and the imposition of special tariffs and changes in tax laws, regulatory policies and accounting standards. There is also the risk that corruption may negatively affect publicly-funded infrastructure projects, especially in emerging markets, resulting in delays and cost overruns. In addition, investing internationally presents certain risks not associated with investing solely in the U.S., such as currency fluctuation, political and economic change, social unrest, changes in government relations, differences in accounting and the lesser degree of accurate public information available, foreign company risk, market risk and correlation risk. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

Nuveen, LLC provides investment solutions through its investment specialists.

This information does not constitute investment research as defined under MiFID.

Sources

1 Data source: Licensed from the Global Infrastructure Hub Ltd under a Creative Commons Attribution 3.0 Australia License. To the extent permitted by law, the GI Hub disclaims liability to any person or organization in respect of anything done, or omitted to be done, in reliance upon information contained in this publication.

2 Data source: Jessop, S. (2017, July 25). World needs $94 trillion spent on infrastructure by 2040: report. Retrieved from https://www.reuters.com/article/us-global-infrastructurereport/world-needs-94-trillion-spent-on-infrastructure-by-2040-report-idUSKBN1AA1A3

3 Data source: “World Urbanization Prospects, 2018 Revision of World Urbanization Prospects,” The United Nations, Department of Economic and Social Affairs. Most recent data available.

4 Data source: “Bridging Global Infrastructure Gaps,” McKinsey & Company, June 2016. Most recent data available.

5 Data source: “What Happened When Chicago Privatized its Parking System,” MinnPost.com, December 19, 2011; ChicagoMeters.com. Most recent data available.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Performance data shown represents past performance and does not predict or guarantee future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. For term definitions and index descriptions, please access the glossary on nuveen.com. Please note, it is not possible to invest directly in an index.

Important information on risk

All investments carry a certain degree of risk, including possible loss principal and there is no assurance that an investment will provide positive performance over any period of time. Because infrastructure portfolios concentrate their investments in infrastructure-related securities, portfolios have greater exposure to adverse economic, regulatory, political, legal, and other changes affecting the issuers of such securities. Infrastructure-related businesses are subject to a variety of factors that may adversely affect their business or operations, including high interest costs in connection with capital construction programs, costs associated with environmental and other regulations, the effects of economic slowdown and surplus capacity, increased competition from other providers of services, uncertainties concerning the availability of fuel at reasonable prices, the effects of energy conservation policies and other factors. Additionally, infrastructure-related entities may be subject to regulation by various governmental authorities and may also be affected by governmental regulation of rates charged to customers, service interruption and/or legal challenges due to environmental, operational or other mishaps and the imposition of special tariffs and changes in tax laws, regulatory policies and accounting standards. There is also the risk that corruption may negatively affect publicly-funded infrastructure projects, especially in emerging markets, resulting in delays and cost overruns. In addition, investing internationally presents certain risks not associated with investing solely in the U.S., such as currency fluctuation, political and economic change, social unrest, changes in government relations, differences in accounting and the lesser degree of accurate public information available, foreign company risk, market risk and correlation risk. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

Nuveen, LLC provides investment solutions through its investment specialists.

This information does not constitute investment research as defined under MiFID.