European insurers have avoided securitisations for over a decade, deterred by punitive capital treatment under Solvency II. While forthcoming reforms could be a gamechanger for Europe, the breadth and depth of the U.S. securitised market offer more opportunities for immediate implementation.

Key takeaways

- Solvency II reforms will align capital charges for securitisation with empirical risk, reflecting decades of exceptional resilience in senior tranches.

- European insurers can access meaningfully higher spreads than comparable corporate bonds without taking higher credit risk.

- As Europe takes time to rebuild its securitisation market, the U.S. offers near-term opportunities in areas.

The paper at a glance

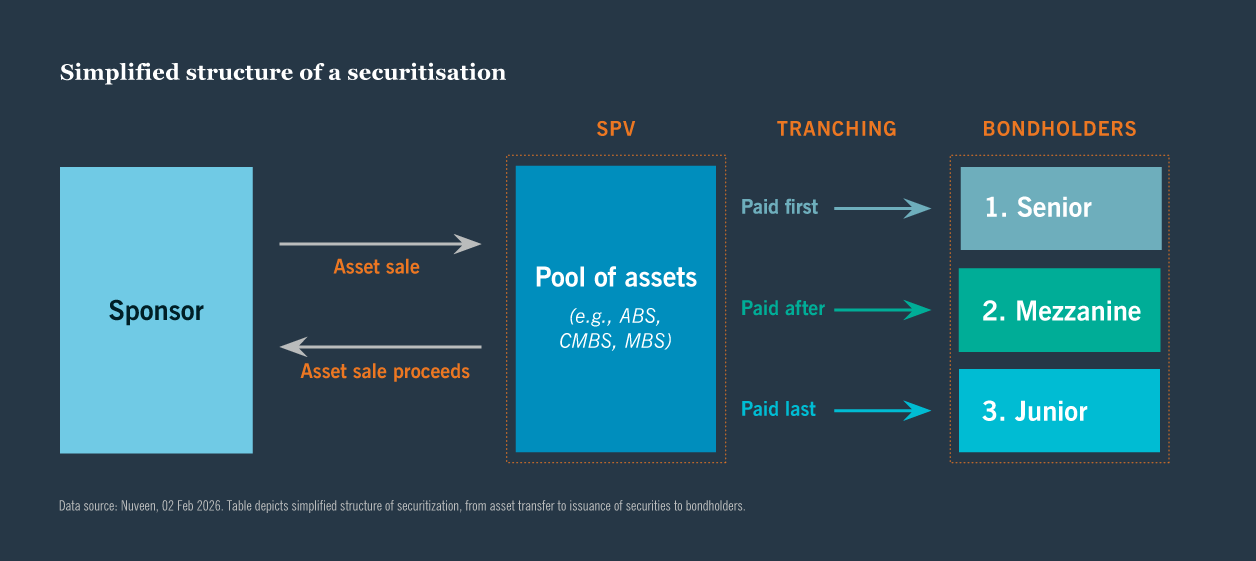

Securitisation: The Basics

Securitisation pools assets into tradable securities, enabling lenders to achieve balance sheet and capital relief, while offering institutional investors — including European insurers — higher spreads than corporate bonds, diversification, and access to a large, scalable market.

Learn more about how this structure creates opportunity for European insurers.

Why the opportunity lies in the U.S.

The U.S. securitised market stands at approximately $13 trillion,1 compared to €1.2 trillion in Europe.2 Annual issuance volumes reinforce this divergence.

This is critical because Solvency II implementation does not require non-STS investments to be made domestically or regionally. Capital charges vary by rating and structure, not geography, allowing insurers to tap the U.S. market as soon as the reforms come into effect.

To discover which U.S. asset classes offer the most compelling near-term opportunities, download the full article.

European insurers considering securitised credit allocations should consider the following key factors:

- Currency management

- Operational infrastructure

- Portfolio construction

- Manager selection

- Internal model and risk governance

For more in-depth guidance on implementing securitised credit into insurance portfolios, get the full article here.

Conclusion

The July 2025 Solvency II reforms represent a watershed moment for European insurers. Decades of data demonstrating the resilience of securitised credit will finally align with supervisory capital treatment. The U.S. market provides immediate scale and a broad range of opportunities while Europe rebuilds.

The investment thesis rests on three pillars. Read more to explore what they are and why the reforms matter for European insurers.

Contact us

- +44 20 3727 8000

- 201 Bishopsgate, London, United Kingdom

2 SIFMA, U.S. Structured Finance Statistics, Q3 2025