Asset allocation

A new investment landscape: implications of the Dutch pension transition

Summary

The Netherlands is executing one of the most significant pension reforms in developed market history. By January 2028, approximately €1.8-1.9 trillion in pension assets (equivalent to 150% of Dutch GDP) will transition from a collective defined benefit framework to defined contribution structures based on lifecycle investing principles.

This transition fundamentally reshapes asset allocation through three regulatory changes:

- Elimination of punitive capital charges on risky assets

- Introduction of age-based lifecycle risk profiles that replace one-size-fits-all defensive positioning

- Adoption of market-based risk assessment replacing prescribed regulatory shocks

This analysis is based on proprietary Nuveen research conducted through October 2025 and January 2026, which included interviews with Dutch pension fund advisors, fiduciary managers and OCIO providers.

Our research outlines the implications for the supply and demand of different asset classes. Furthermore, it supports our views that success requires understanding:

- how lifecycle mechanics drive allocation changes

- how contract structure determines implementation

Key findings

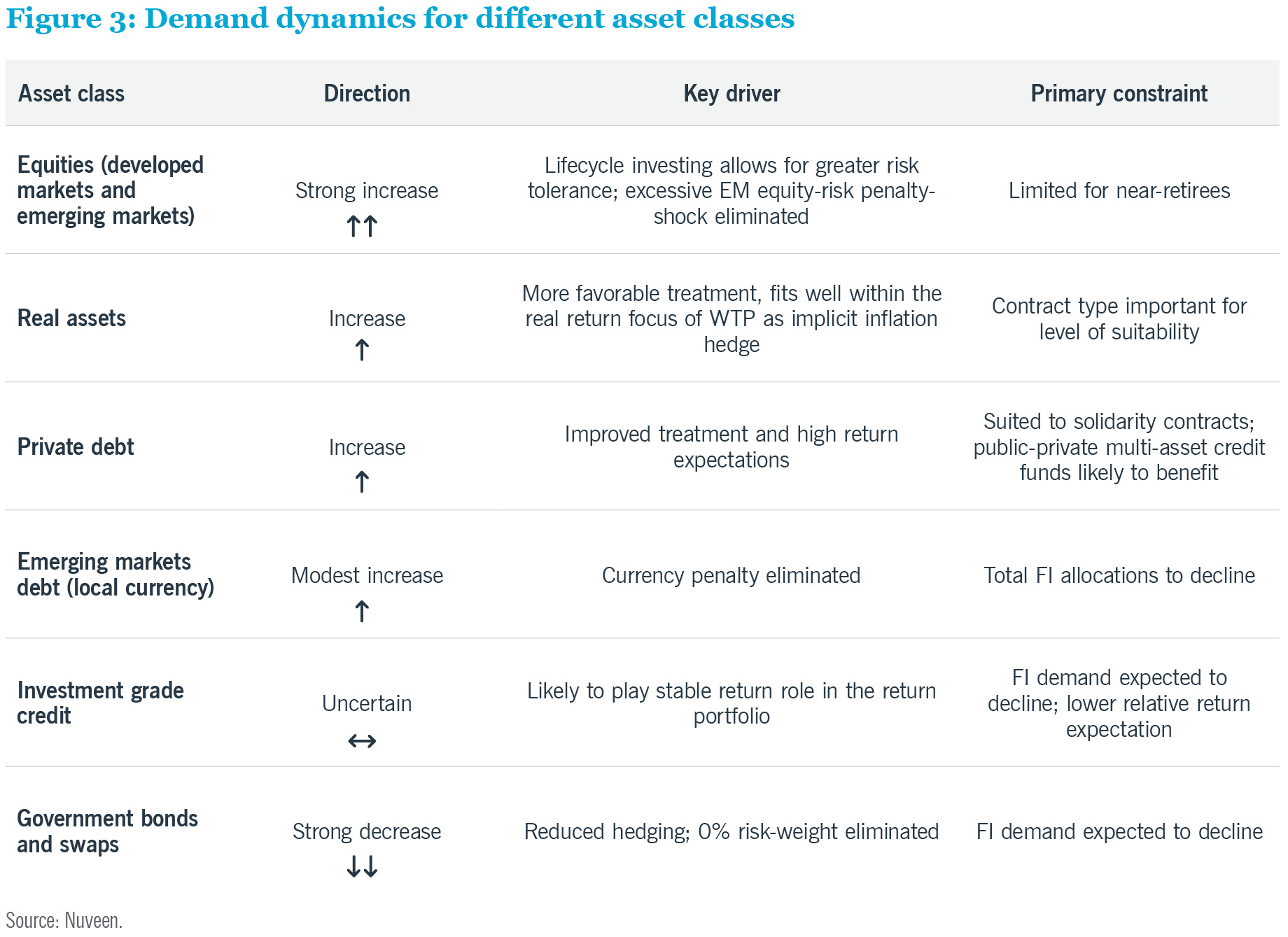

- Substantial increase in equity allocations expected: Funds are targeting considerably higher equity allocations for younger cohorts, driven by lifecycle implementation and elimination of VEV capital charges. Emerging markets (EM) equities to further benefit from the elimination of the 40% regulatory shock (versus 30% for developed markets), which removes a 33% penalty

- Fixed income demand faces structural decline: Government bonds and swaps are expected to decline as hedging requirements diminish; pensions funds anticipated to offload approximately €100-150 billion in government bonds

- Composition of fixed income exposure to change: Remaining bond allocations are moving away from developed markets (DM) government bonds toward spread products, such as corporate credit and emerging markets debt (EMD)

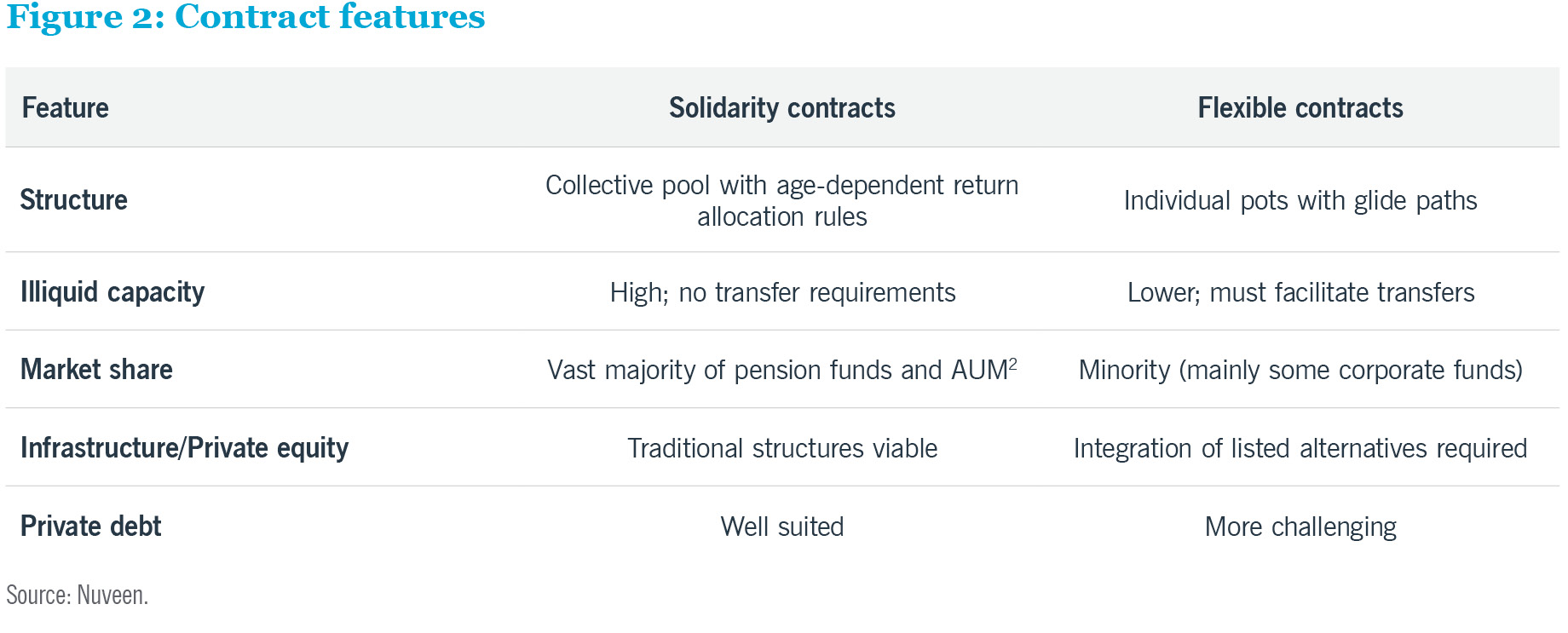

- Contract structure determines capacity for illiquid assets: Solidarity contracts (expected to be the vast majority) maintain substantial capacity for illiquid investments; flexible contracts (limited take-up expected) face more liquidity constraints that preclude traditional illiquid structures

- Real assets gain from regulatory changes: Infrastructure and real estate benefit from a less penalizing classification of risk under the new WTP framework. Real assets also provide diversification from equity allocations and inflation protection, which aligns with the WTP’s real return goal

- Private asset investing to ramp up: While decisions to add new or make sizeable allocation changes to private asset classes will take time, funds that transitioned in January 2026 are expected to do so from around Q2 to Q3 2026 with more funds following in 2027 after transitioning. Private debt investing is expected to gain ground from 2027 onward within solidarity contracts

- Interest in impact investing to increase: Greater exposure to corporate entities through increasing equity and credit allocations will create opportunities for ESG and sustainability-focused strategies

Regulatory Architecture

Figure 1 highlights the different asset class treatment under the old and new systems and their likely impact. The old FTK framework required pension funds to maintain buffers ensuring 97.5% certainty of the ability to pay all benefits in one year’s time (equivalent to a funding ratio at 100%+). This imposed uniform defensive positioning across all participant age groups.

With the new WTP system, three regulatory changes will have significant impact. The elimination of VEV capital charge removes the penalties on holding equities and other more illiquid risk assets. The implementation of lifecycle mandates enables younger participants to have a higher allocation to a riskier portfolio in search of higher returns (which typically means equities are the largest exposure) compared with older participants’ more defensive portfolios (which typically means fixed income is the largest exposure). The new system provides transparency as participants receive monthly valuation reports.

Portfolio structure: protection vs. return

The new framework mandates clearer separation between protection and return portfolios. Return portfolios serve all cohorts, especially the needs of younger participants, as they prioritize allocations to risk-bearing assets for long-term growth. Fixed income allocations in return portfolios will likely shift toward higher return spread products (e.g. EM debt, developed markets corporate credit), while private equity and private credit are estimated to increase in allocations by about 5%.1 Furthermore, interest is likely to increase in asset classes that can provide absolute returns with low correlation to equities (such as public-private multi-asset credit, catastrophe bonds and commodity trading advisors (CTAs)).

While government bond allocations will likely be lower in aggregate for pension funds, they will remain an important part of protection portfolios. These protection portfolios serve older participants through lower risk fixed income exposure that better match their liabilities.

Contract structure: the critical binary

Pension funds must choose between solidarity and flexible contracts, a decision that fundamentally determines investment implementation possibilities. Solidarity contracts will be more popular in terms of the number of pension funds adopting them as well as assets managed under this regime. However, a limited number of corporates will continue to favor flexible contracts.

Solidarity contracts maintain collective investment pools with age-dependent return allocation rules, preserving maximum flexibility for illiquid investments. In contrast, flexible contracts create individual pension pots (unitization of investments) and provide investment options, meaning higher liquidity needs that can constrain some illiquid investment capacity.

Investment implications

Equity implications

Four regulatory changes should lead to substantial equity allocation increases:

- VEV elimination removes artificial capital penalties. Risk expectations will now reflect observed market volatility

- Elimination of the 97.5% one-year certainty requirement of 100%+ funding ratio removes inappropriate defensive requirements

- Lifecycle implementation enables aggressive (higher risk) positioning for younger cohorts. Funds with significant young participant populations are targeting higher equity allocations for these cohorts, creating sustained demand through 2026-2028 and beyond

- Individual account visibility and monthly valuations increase transparency and potential engagement for participants

Developed markets (DM): We expect DM equities to be the single largest beneficiaries of the pension reform as pension plans move toward more risk taking under the WTP. Active equity managers should find favor in this environment given the WTP’s focus on returns and pension plan intentions. As revealed during our research interviews, pension funds are looking to reposition regional exposures amid ongoing geopolitical uncertainty and cater to plan participants’ sustainable investing requirements.

Emerging markets (EM): Under the old FTK, EM equity faced a 40% regulatory shock versus 30% for DM equity; a 33% higher regulatory capital requirement. The new framework assesses actual volatility, which often shows EM equity comparable with DM equity. This change positions EM equity as both a possible structural beneficiary (from shock elimination) and strategic opportunity (diversifying from U.S.-concentrated developed markets with lower correlation plus higher return potential).

Fixed income implications

Government bonds and interest rate swaps face severe structural reduction in demand. AAA government bonds move from regulatory favorites to a neutral assessment with unattractive returns within fixed income for the return portfolio. At the same time, interest rate hedging requirements decline dramatically, with approximately €100-150 billion in long-end government bond sales expected. Swap notional amounts are expected to reduce too, with the reduction concentrated in long maturities (30+ years).

Within declining aggregate fixed income allocations, composition shifts decisively toward return-generating spread products: emerging markets debt, high yield and potentially some investment grade credit. Protection portfolios will mainly focus on pure matching with swaps and government bonds (under the preferred indirect method).

Emerging markets debt: The old FTK system separately penalized both credit and currency risk. The new framework focuses on observed market volatility, eliminating the separate currency penalty. EMD offers lower equity correlations than high yield, potentially making it a more effective diversifier.

Investment grade (IG) credit: Given many funds are choosing the indirect De Nederlandsche Bank methodology for rate hedging, a role for IG credit in the protection portfolio appears limited. However, IG credit could feature in return portfolios given its lower but stable return potential and participants’ preferences for stability and avoiding large drawdowns.

High yield: This asset class should see some uptake due to attractive income and return potential combined with daily liquidity. However, high yield bonds have a higher correlation with equities compared to alternative spread products, limiting their strategic appeal during periods of equity market stress.

Real asset and alternative opportunities

Infrastructure, real estate and broader real assets should benefit from improved regulatory treatment and their ability to provide diversification from increasing equity allocations. Real assets receive a 100% “risk-bearing” assets classification, like equities despite exhibiting meaningfully lower volatilitys. Real assets also fit well with the WTP focus on real return target profiles. Real estate and infrastructure currently represent approximately 20% of portfolios as “cornerstone investments” valued for diversification, inflation protection, and potential for ESG alignment. Broader real asset opportunities including farmland and timber could also receive an increasing allocation. Monthly valuation requirements for all private investments is a challenge, however.

According to our research, private debt is under active investigation by multiple funds, with implementation expected primarily from 2027 onward. The asset class benefits from improved regulatory treatment and offers attractive illiquidity premiums. Solidarity contracts are better suited than flexible contracts due to the liquidity needs by the latter. The optimal approach includes both private markets and publicly traded comparables for liquidity purposes. Public-private multi-asset credit funds could provide a solution, especially for flexible contracts.

The inflation protection gap

Explicit inflation protection remains frequently absent from implementation plans despite purchasing power preservation being central to the new framework’s mandate. During our research, many investors highlighted how inflation in the Netherlands consistently exceeds broader European levels in the long run. Given this, strategies offering inflation protection will likely be in demand, such as infrastructure and real assets with cash flows linked to inflation.

The case for impact investing

The pension reform caters to the increasing interest in impact investing in the Netherlands. The expected growth in equity allocations, illiquid opportunities within private credit, real assets and private equity, plus scope for more credit within fixed income allocations essentially increases exposure to corporates. By providing capital either through equity or debt, investors have different avenues to influence corporate policies. This will be partly facilitated by any increase in active investing and the use of benchmarks with ESG, impact or sustainability criteria. Furthermore, with the WTP system, participants are likely to be asked about investing along sustainability and impact lines, which creates opportunities for thematic investing such as affordable housing, health, climate, food security, energy transition and the circular economy.

Conclusion

The Dutch pension transition will trigger a reallocation of €1.8-1.9 trillion with unambiguous implications.

- Equity allocations increase substantially.

- Fixed income exposure decreases, particularly to long duration assets, while spread products are likely to be a higher proportion of the reduced fixed income allocations.

- Private debt emerges as an opportunity due to the changes in regulatory treatment and attractive illiquidity premiums.

- Real assets gain from more favorable regulatory treatment under WTP and a real return focus.

Contact us

- +44 20 3727 8000

- 201 Bishopsgate, London, United Kingdom

Endnotes

1 Source: APG Asset Management, FT.com, Dutch pensions to invest €100bn in risky assets boosting Europe’s defence efforts, 30 March 2025

2 Source: ASR, Zijn flexibele premieregelingen de échte koplopers?, 16 September 2025